In early June 2026, Samsung Electronics finds itself positioned at a dramatic crossroads between unprecedented industrial demand and shifting corporate dynamics. Following a spectacular year-to-date gain exceeding 190%, the South Korean semiconductor pioneer briefly surpassed Meta and Tesla in market capitalization during intraday trading on June 2, breaking into the world's top ten companies with a market cap peaking near $1.54 trillion before stabilizing around ₩310,500 per share.

While the stock spent previous cycles navigating severe supply gluts, back-to-back operational breakthroughs in high-bandwidth memory (HBM) have supercharged its revenue outlook. Investors are aggressively weighing exceptionally strong first-quarter reports and highly bullish forward guidance against an escalating labor landscape that is placing massive pressure on long-term corporate expense models.

As the global technology ecosystem transitions toward specialized agentic AI frameworks and multimodal systems integrating vision, language, and behavior, the absolute necessity for high-density, energy-efficient memory integration has transformed Samsung into a primary infrastructure bottleneck. However, a major labor dispute involving a near-miss general strike has forced management into a unique profit-sharing agreement, creating a persistent valuation debate regarding structural margin compression.

This guide breaks down the Samsung Electronics stock forecast and price prediction for the remainder of 2026, utilizing data from Goldman Sachs, JPMorgan, KB Securities, UBS, and official regulatory financial disclosures.

You will also discover how to trade Samsung Electronics stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Samsung (005930.KS) Traders to Know in 2026

As Samsung navigates a high-stakes environment of explosive revenue scaling and intensive domestic labor negotiations, traders must closely monitor these five market-moving factors:

- The 2027 Total Capacity Sellout: According to KB Securities analyst Jeff Kim, soaring demand from artificial intelligence hyperscalers and structurally limited industry supply growth are set to keep DRAM and NAND markets tight for years. Samsung’s entire memory chip output through 2027 is expected to completely sell out, forcing major tech companies to increasingly negotiate 5-year vendor deals extending through 2030 to secure supply.

- Nvidia HBM4 Validation and the Vera Rubin Pipeline: At the GTC Taipei conference, Nvidia confirmed that its next-generation AI chip architecture, Vera Rubin, will utilize Samsung’s advanced HBM4 memory. Samsung’s high-end AI memory has officially passed quality certifications for both Nvidia and AMD, with its entire 2026 HBM production capacity already fully sold out.

- The Averted 48,000-Member General Strike: On May 20, 2026, an 11th-hour government-mediated negotiation narrowly averted an 18-day general strike by Samsung's largest labor union. While the crisis was temporarily resolved, management conceded to a 6.2% average salary increase for 2026 alongside a landmark 10.5% profit-linked stock bonus pool for the semiconductor division.

- Historic Q1 Financial Outperformance: In its April earnings release, Samsung reported a consolidated Q1 revenue of ₩133.9 trillion, a 69% YoY increase, and an operating profit of ₩57.2 trillion. This marks an eightfold increase in quarterly profit, driven by a robust 42.7% operating margin as contract prices for conventional DRAM surged nearly 98% in Q1 2026 alone.

- The Launch of 12-Layer HBM4E Samples: Pushing to widen its competitive moat, Samsung announced in late May that it has begun global customer shipping of its industry-first 12-layer HBM4E chip. Operating at speeds up to 16 Gbps with a 48GB capacity, this next-generation configuration represents a 30% density increase over baseline HBM4 architectures.

What Is Samsung Electronics?

Samsung Electronics Co., Ltd. is a global leader in application-optimized memory, system LSI, and advanced semiconductor foundry architectures. Operating out of Suwon, South Korea, the company commands a dominant structural position across the global tech stack, maintaining absolute vertical integration across Dynamic Random-Access Memory (DRAM), NAND flash storage, and High-Bandwidth Memory (HBM).

As of mid-2026, Samsung represents a vital pick-and-shovel pillar of the artificial intelligence revolution. Alongside SK Hynix and TSMC, it forms the elite core of the hardware ecosystem feeding colossal data centers. Its proprietary engineering innovations, stacking DRAM vertically to optimize bandwidth and thermal performance, supply the baseline memory layer required by advanced graphics processing units (GPUs) and AI accelerators like Google's Ironwood Tensor Processing Unit.

Samsung’s Performance in Early 2026: The Post-Earnings Repricing

The company kicked off Q2 2026 by reporting standout financial results that completely re-anchored institutional valuations. Consolidated revenue reached ₩133.9 trillion, fueled by a full-scale pricing recovery where global DRAM industry revenues climbed 81% quarter-on-quarter to $97 billion.

Crucially, the memory division alone is projected to generate ₩38 trillion in operating profit for Q1, nearly matching or exceeding its total structural corporate earnings for the entirety of 2025 in just a single quarter. This structural shift prompted analysts at KB Securities to elevate near-term 2026 operating profit estimates by 30% to ₩220 trillion, followed by an aggressive upward revision of 2027 forecasts to ₩301 trillion.

With contract memory prices maintaining an upward trajectory due to tight capacity expansion and high HBM conversion ratios, the underlying financial profile has entered a supercycle decoupling from traditional boom-and-bust behavior.

Samsung’s 2026 Trading Strategy: Navigating Volatility Multiples

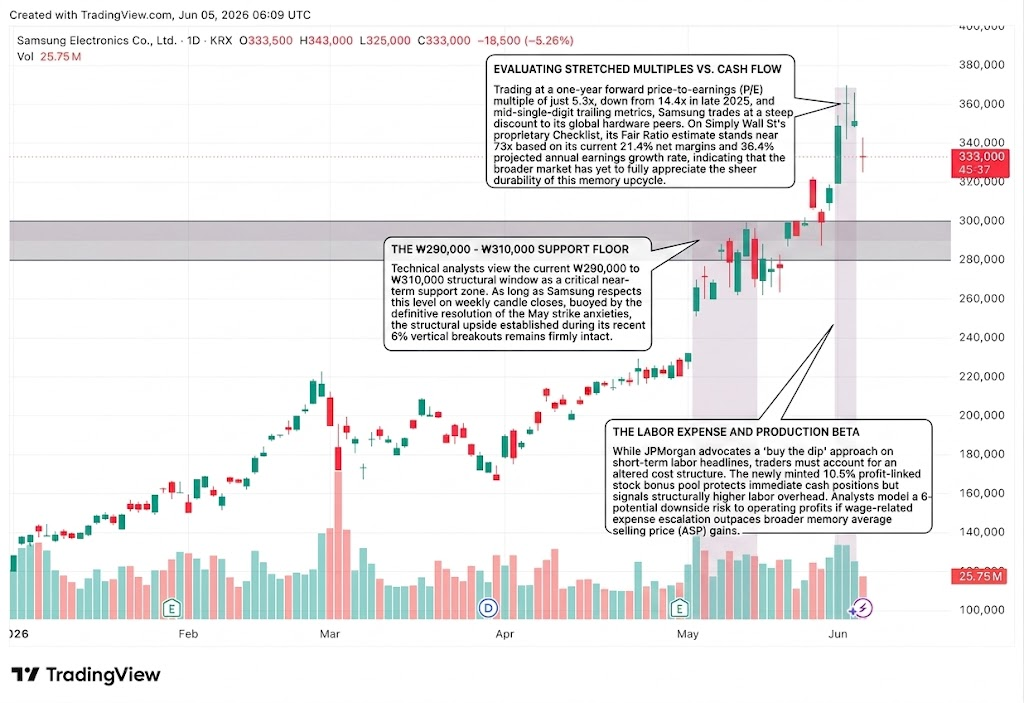

The ₩290,000 - ₩310,000 Support Floor

Technical analysts view the current ₩290,000 to ₩310,000 structural window as a critical near-term support zone. As long as Samsung respects this level on weekly candle closes, buoyed by the definitive resolution of the May strike anxieties, the structural upside established during its recent 6% vertical breakouts remains firmly intact.

Evaluating Stretched Multiples vs. Cash Flow

Trading at a one-year forward price-to-earnings (P/E) multiple of just 5.3x, down from 14.4x in late 2025, and mid-single-digit trailing metrics, Samsung trades at a steep discount to its global hardware peers. On Simply Wall St’s proprietary Checklist, its Fair Ratio estimate stands near 73x based on its current 21.4% net margins and 36.4% projected annual earnings growth rate, indicating that the broader market has yet to fully appreciate the sheer durability of this memory upcycle.

The Labor Expense and Production Beta

While JPMorgan advocates a 'buy the dip" approach on short-term labor headlines, traders must account for an altered cost structure. The newly minted 10.5% profit-linked stock bonus pool protects immediate cash positions but signals structurally higher labor overhead. Analysts model a 6-10% potential downside risk to operating profits if wage-related expense escalation outpaces broader memory average selling price (ASP) gains.

Samsung 2026 Outlook: ₩480,000 Street-High Peak vs. ₩209,000 Structural Cyclical Trap

Evaluating Samsung's forward trajectory requires balancing an unyielding, multi-year semiconductor undersupply against the operational friction of an escalating domestic labor landscape.

The Bull Case: The ₩480,000 HBM4 Monopoly and Apple Foundry Catalyst

The bullish thesis hinges entirely on Samsung's rapid execution in high-end AI nodes. Championed by Goldman Sachs’ target upgrades toward ₩480,000, this path assumes that memory is entering a permanent structural paradigm shift rather than a cyclical spike. Under this framework, Samsung’s conventional DRAM ASP will increase 326% year-over-year in 2026, while the global HBM total addressable market expands exponentially to $116 billion by 2027.

In this scenario, Samsung successfully captures 40% of the global HBM market share by 2027, matching SK Hynix. This dominance is augmented by a massive secondary secular catalyst: exploratory discussions with Apple to manufacture main device processors directly within U.S. foundry facilities. If verified, these multi-billion-dollar foundry commitments would break TSMC's absolute monopoly, justifying a massive re-rating of the stock toward ₩480,000.

The Base Case for Samsung Stock: ₩320,000 – ₩360,000 Consolidation Plateau

The base case envisions a steady upward ascent where the market reconciles Samsung's massive cash generation with its structural operating constraints. Backed by KB Securities and JPMorgan, this path factors in a projected 148% jump in 2026 DRAM contract pricing alongside 111% NAND increases.

Valuations comfortably stabilize between ₩320,000 and ₩360,000 as tech hyperscalers deploy over $700 billion in infrastructure spending. In this landscape, the stock is insulated from steep downside due to robust binding long-term agreements (LTAs), but upside remains capped as minor production frictions and rising components costs within Samsung’s mobile and display divisions partially offset the astronomical gains of the semiconductor division.

The Bear Case: The ₩209,000 Cyclical Turn and Union Rejection Trap

The bearish outlook focuses on historical cyclical mean reversion and domestic execution risk. If the tentative wage agreement face-plants during upcoming union ratification votes, or if workers renew calls for a permanent 15% absolute corporate operating profit allocation, institutional capital may flee due to margin erosion fears.

This thesis, modeled by Simply Wall St's community bear case fair value of ₩209,079, assumes that the memory boom remains inherently cyclical. If macro head-winds stunt global edge-AI rollouts in autonomous vehicles and robotics, an abrupt accumulation of secondary supply could trigger an aggressive turn in DRAM/NAND contract pricing, forcing a rapid, high-beta correction back toward the ₩200,000 level.

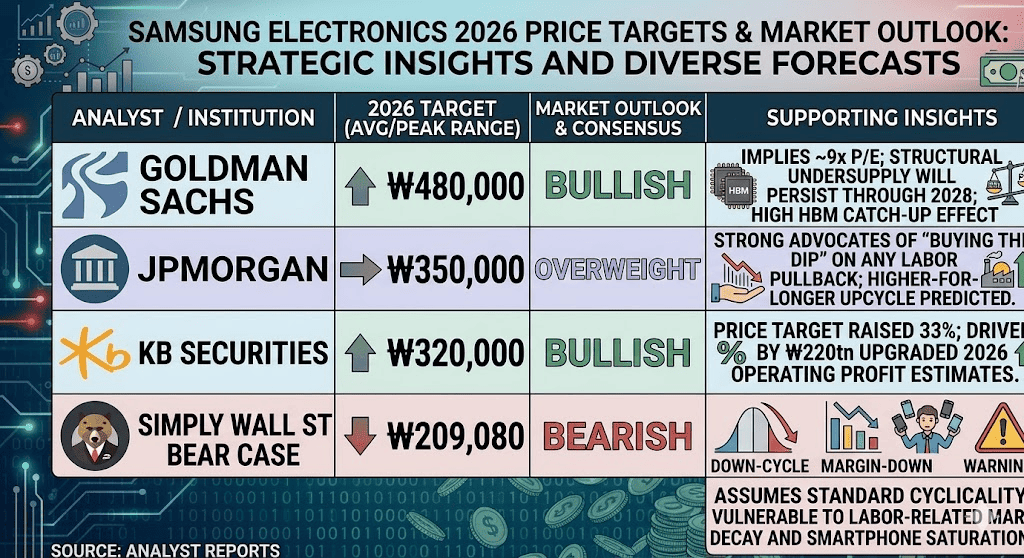

Samsung Electronics (005930.KS) Price Forecasts for 2026 by Wall Street Analysts

|

Institution |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

Goldman Sachs |

₩480,000 |

Bullish: Implies ~9x P/E; structural undersupply will persist through 2028; high HBM catch-up effect. |

|

JPMorgan |

₩350,000 |

Overweight: Strong advocates of "buying the dip" on any labor pullback; higher-for-longer upcycle. |

|

KB Securities |

₩320,000 |

Bullish: Price target raised 33%; driven by ₩220tn upgraded 2026 operating profit estimates. |

|

Simply Wall St Bear Case |

₩209,080 |

Bearish: Assumes standard cyclicality; vulnerable to labor-related margin decay and smartphone saturation. |

How to Trade Samsung Electronics Stock Futures on BingX TradFi

As Samsung navigates this period of historic market capitalization expansion and high-volume price discovery, tactical traders can seamlessly capitalize on its price action through the BingX platform:

- Access BingX TradFi: Navigate to the specialized TradFi section on the main BingX exchange dashboard.

- Select Samsung Electronics (005930): Search for and select the SAMSUNG-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the Nvidia HBM4 validation and ₩530 trillion 2027 profit forecasts will drive the asset to the ₩480,000 street-high target. Select Open Short to trade the potential downside of labor friction and cyclical price turns.

- Select Leverage and Margin Mode: Apply your preferred Isolated or Cross-Margin parameters alongside conservative leverage to optimize capital efficiency.

- Execute Strict Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in gains and insulate your capital from abrupt gaps in Asian market trading hours.

Top 5 Risks to Consider Before Investing in Samsung Stock

While Samsung’s explosive top-line semiconductor growth presents a compelling narrative, navigating this asset demands a rigorous assessment of its unique operational landmines:

- Union Ratification and Labor Vulnerabilities: If the tentative 10.5% stock bonus framework is rejected by the general membership vote, the suspension of the 18-day strike will dissolve, threatening global supply chains.

- HBM Market Share Competition: Rival SK Hynix maintains an exceptionally high bar, posting record 72% operating margins in Q1 and forcing Samsung into aggressive, capital-intensive R&D conversion cycles to catch up.

- Macroeconomic Mobile/Display Softness: While the chip unit experiences an absolute frenzy, Samsung's consumer-facing mobile and display segments face margin deterioration due to rising materials costs.

- Capital Expenditure Dilution: Massive long-term investment targets, including a projected annual operating goal of ₩200 trillion through 2028, require immense, sustained capital deployments that restrict near-term free cash conversion.

- Geopolitical Trade Vulnerabilities: As a core linchpin of global AI hardware, Samsung remains deeply exposed to international trade control friction, export compliance adjustments, and technological fracturing between Eastern and Western consumer corridors.

Final Thoughts: Is Samsung Electronics Stock a Buy in 2026?

As of June 2026, Samsung Electronics represents one of the most fundamentally mispriced mega-cap opportunities within the artificial intelligence infrastructure landscape. The company's unique dual validation across Nvidia and AMD ecosystems, combined with a total supply sellout stretching through 2027, completely validates the thesis that memory is an indispensable, non-cyclical structural bottleneck.

While domestic labor negotiations introduce a layer of headline volatility and a higher cost baseline, trading at a steep forward P/E discount offers an incredibly compelling margin of safety compared to stretched Western technology multiples. For tactical short-term participants, the equity provides an elite ecosystem for volatility capture via BingX futures, while long-term investors are presented with an attractive entry point into the structural backbone of the global AI boom.

Risk Reminder: Trading high-growth semiconductor equities involves significant capital risk due to elevated beta metrics, capital-intensive manufacturing adjustments, and complex domestic labor frameworks. Always enforce disciplined risk management, proper position sizing, and mandatory stop-losses.

Related Reading

- SMCI Stock Price Prediction 2026: $65 Street-High Rack-Scale Boom or Corporate Governance Trap?

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide