In early July 2026, Redwire Corporation (NYSE: RDW) has become one of the most-watched names at the intersection of space infrastructure and defense technology. After spiking as high as $24 during the space-sector rally around the SpaceX IPO hype, RDW pulled back to the $11 to $12 range following a large equity offering, revenue miss, and widening GAAP losses, while still holding gains of well over 40% on a trailing 12-month basis.

The bull case is built on 58% Q1 revenue growth, a record $498.1 million contracted backlog, a 1.92 book-to-bill ratio, exposure to the U.S. Missile Defense Agency's SHIELD and Golden Dome architecture, a NATO ally's multiyear high eight-figure Penguin Mk3 contract, and the transformative Edge Autonomy acquisition.

The risk is that RDW remains adjusted EBITDA-negative, missed both revenue and EPS in Q1, launched a $500 million at-the-market equity program that raised dilution concerns, and still trades at 7x sales in a sentiment-driven space and defense rotation. This guide breaks down the Redwire stock forecast, 2026 price scenarios, key risks, and how to trade RDW stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Redwire Traders to Know in 2026

Redwire's 2026 story is shaped by a sharp divide between operational milestones, a record backlog and NATO contract wins, and financial friction, GAAP losses, dilution, and adjusted EBITDA that remains negative. As RDW navigates a fast-changing space and defense cycle, market participants must closely track these core structural drivers:

- The $498 Million Record Backlog: Redwire ended Q1 2026 with $498.1 million in contracted backlog, up from $411.2 million a quarter earlier, driven by a 1.92 book-to-bill ratio and more than $350 million in bookings over the trailing two quarters. Roughly 72% of the backlog sits in the space segment, with the remainder in defense tech.

- The Edge Autonomy Acquisition Transformed the Business: Redwire's $925 million acquisition of Edge Autonomy, completed June 13, 2025, added the field-proven Stalker and Penguin uncrewed aerial system product lines and turned Defense Tech into a segment nearly the size of Space. By Q1 2026, more than 100 Stalker and Penguin UAS had been delivered to seven countries, including the U.S. Army, U.S. Marine Corps, and multiple NATO allies.

- SHIELD and Golden Dome Exposure: Redwire's January 2026 SHIELD contract from the U.S. Missile Defense Agency placed it inside the market conversation around the Trump administration's Golden Dome missile defense architecture, which some analysts frame as a $542 billion total addressable market with an initial $25 billion funding opportunity.

- A $500 Million ATM Equity Offering Raised Dilution Concerns: Redwire announced in June 2026 a $500 million at-the-market equity program, following a completed follow-on offering of about 25.5 million shares at $7.23 earlier in the year, prompting a sharp post-announcement selloff and an ongoing debate over how much the story is priced in.

- Analyst Coverage Is Split After a Massive Rally: With RDW up more than 220% year to date at its peak, analyst views diverged sharply, from Cantor Fitzgerald's $9.00 target and BofA Securities' $6.00 target on the cautious side to HC Wainwright's $22.00 target on the bullish side, with the consensus around a $14 to $16 price target.

Read More: Top Space Stocks to Buy Ahead of SpaceX IPO

What Is Redwire Corporation (NYSE: RDW)?

Redwire Corporation (NYSE: RDW) is a Jacksonville, Florida-based aerospace and defense technology company founded in 2020 and taken public through a SPAC merger in 2021. The company develops and delivers mission-critical solutions for government, commercial, and civil customers, spanning spacecraft platforms, space infrastructure, avionics, sensors and payloads, power generation systems, radio frequency systems, digital engineering software, and, following the Edge Autonomy acquisition, tactical uncrewed aerial systems.

Redwire operates through two main segments. The Space segment covers spacecraft platforms, sensors and avionics such as star trackers and sun sensors, digital engineering software, in-space manufacturing and biotech facilities aboard the International Space Station, and NASA-linked programs including lunar infrastructure hardware. The Defense Tech segment, built around the Edge Autonomy acquisition, covers combat-proven Stalker and Penguin UAS aircraft, autonomous systems, optical sensors, resilient energy solutions, and intelligence, surveillance, and reconnaissance capabilities for U.S. and allied customers.

In 2026, Redwire's biggest strategic shift is the integration of Edge Autonomy and the positioning of the combined business as a dual-play on space infrastructure and defense modernization. Management has framed the company as a beneficiary of both the multiyear NASA and lunar exploration cycle and the Pentagon's expanding drone and missile-defense budgets, alongside allied NATO demand for tactical UAS platforms.

Read More: What Is SpaceX Tokenized Stock (SPCXB) and How to Buy SPCX Tokenized Stock?

Redwire's Performance in Early 2026: From Record Backlog to Dilution Overhang

Redwire entered 2026 in the middle of its most consequential business transformation to date, with the Edge Autonomy acquisition fully integrated and a growing pipeline of space and defense contracts.

Q1 2026 revenue grew 57.9% year over year to $97.0 million, driven by the Edge Autonomy contribution, a favorable contract mix, and major wins in next-generation spacecraft, quantum-secure satellites, and defense tech. The Space segment contributed $52.7 million and Defense Tech contributed $44.3 million. Gross margin expanded sharply to 26.6% from 14.7% in the prior-year quarter, and total liquidity reached a record $175.2 million, including roughly $145 million in cash and a $30 million undrawn revolver. However, revenue missed consensus by 7.3% and the GAAP net loss widened to $76.5 million, weighed down by more than $42.5 million in accelerated equity-based compensation tied to the Edge Autonomy deal.

Redwire Corporation Q1 2026 Financial and Consensus Profile

Redwire’s Q1 2026 results showed strong top-line growth but weaker profitability, with revenue missing consensus and GAAP losses widening due partly to non-recurring Edge Autonomy charges. The market reaction was mixed: analysts remained constructive on long-term space infrastructure demand, but the later $500 million ATM equity program increased dilution concerns.

|

Financial Metric |

Consensus Estimate |

Reported / Actual |

Surprise / Trend |

|

Q1 FY2026 Revenue |

~$104.6 million |

$97.0 million |

Missed estimates, but grew 57.9% YoY |

|

Q1 FY2026 GAAP EPS |

-$0.15 |

-$0.40 |

Wider loss than expected |

|

Q1 FY2026 Net Loss |

— |

$76.5 million |

Included ~$42.5 million in non-recurring Edge Autonomy charges |

|

Q1 FY2026 Gross Margin |

— |

26.60% |

Improved from 14.7% in Q1 2025 |

|

Q1 FY2026 Adjusted EBITDA |

— |

-$9.2 million |

Improved sequentially; would have been positive excluding discretionary IRAD |

|

Q1 FY2026 Contracted Backlog |

— |

$498.1 million |

Record high; book-to-bill of 1.92 |

|

FY2026 Revenue Guidance |

— |

$450 million to $500 million |

Reaffirmed; midpoint implies ~41.6% YoY growth |

|

FY2026 Consensus EPS |

-$0.515 |

-$0.875 revised |

Street estimates moved lower after Q1 |

After the Q1 earnings print, Canaccord raised its price target to $14 and Jefferies raised its target to $13, with both firms maintaining Buy ratings at the time. The setup became more cautious after Redwire announced a $500 million at-the-market equity program in June 2026, which triggered dilution concerns and contributed to a sharp pullback. Management reaffirmed full-year 2026 revenue guidance of $450 million to $500 million, with Q2 2026 results scheduled for August 4, 2026.

Redwire's 2026 Trading Strategy: Backlog Conversion and Dilution Discipline Drive the Setup

Redwire's 2026 setup depends on three key signals: whether the record backlog converts into revenue on schedule, whether adjusted EBITDA can turn positive without further one-time drags, and whether the pace of equity issuance under the $500 million ATM stays measured enough to keep dilution from overwhelming the growth story.

- Watch the $8.50 to $12 Support Zone: After breaking out from an $8.50 to $9.00 base earlier in the year and running to a $24 high during the SpaceX IPO-driven space-sector rally, RDW has pulled back to the $11 to $12 area following the ATM announcement and Jefferies' downgrade. A sustained move above $15 would support a retest of the mid-$20s highs, while a break back below $9 could revive concerns about dilution and execution.

- Backlog Conversion vs. Dilution Risk: The bull case values Redwire as a fast-growing space and defense infrastructure provider with a record backlog, sector-leading book-to-bill, and exposure to Golden Dome. The risk is that the company remains adjusted EBITDA-negative, and that ongoing ATM issuance could add material share count over the year even if revenue meets guidance.

- Monitor Contract Wins and Insider Activity: RDW is highly sensitive to headline contract news, from the NATO Penguin Mk3 win to smaller USMC and international orders. Insider activity has also been mixed, with the CEO and other executives making small purchases while the RED Holdings vehicle recorded large sales over recent quarters, adding another data point to sentiment.

Read More: SpaceX (SPCX) Price Prediction 2026: $227 Street-High AI Fusion or Trillion-Dollar Valuation Bubble?

The Redwire 2026 Forecast: $22+ Golden Dome Upside vs. $6 Execution Risk Floor

Redwire’s 2026 outlook depends on whether space and defense demand stays strong, whether its record backlog converts into revenue and margin expansion, and whether the June at-the-market equity program can be managed without overwhelming the operating improvement story.

The Bull Case: Backlog Conversion and Golden Dome Push RDW Above $22

The bull case requires Redwire to convert its record $498 million backlog into revenue near or above the top end of its $450 million to $500 million full-year guidance, deliver positive adjusted EBITDA in the second half, and secure additional Golden Dome-related contracts as missile defense funding accelerates. If the NATO Penguin Mk3 contract leads to follow-on orders and Q2 shows disciplined ATM usage, RDW could retest the $22 to $24 range implied by the most bullish analyst targets.

The Base Case: Steady Execution Keeps RDW Between $12 and $16

The base case assumes disciplined execution without a major new catalyst. Redwire reaches the midpoint of its 2026 revenue guidance, gross margin holds in the mid-20% range, and the ATM program is used gradually rather than aggressively. In this scenario, RDW could consolidate between $12 and $16 as investors wait for clearer evidence of adjusted EBITDA improvement and additional contract wins.

The Bear Case: Dilution and Execution Setbacks Pull RDW Toward $6 to $8

The bear case is driven by revenue misses, wider losses, aggressive ATM issuance, slower backlog conversion, or a broader unwind in space and defense sentiment after the sector rally. If the market shifts back to valuing Redwire on current cash flow rather than future backlog and defense optionality, RDW could retest the $6 to $8 range, closer to the more cautious BofA and Cantor Fitzgerald views.

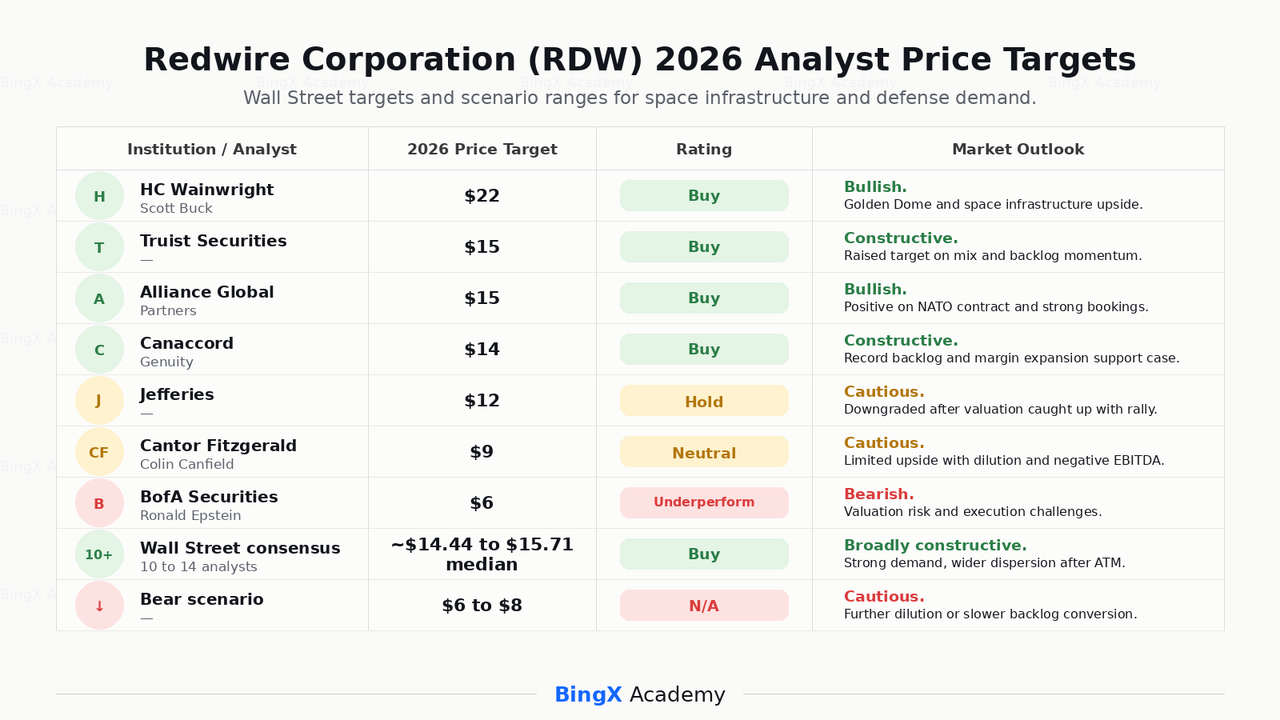

Redwire Corporation Price Forecasts for 2026 by Wall Street Analysts

Wall Street remains broadly constructive on Redwire, but views have become more divided after the June 2026 ATM equity program. Bulls focus on space infrastructure demand, Golden Dome defense exposure, and record backlog conversion, while cautious analysts focus on dilution, negative EBITDA, and execution risk.

|

Institution / Analyst |

2026 Price Target |

Rating |

Market Outlook |

|

HC Wainwright / Scott Buck |

$22.00 |

Buy |

Bullish. Sees Redwire as a leveraged play on space infrastructure and Golden Dome missile defense demand. |

|

Truist Securities |

$15.00 |

Buy |

Constructive. Raised target from $13 on improving revenue mix and backlog momentum. |

|

Alliance Global Partners |

$15.00 |

Buy |

Bullish. Raised target after the NATO Penguin Mk3 contract and strong bookings. |

|

Canaccord Genuity |

$14.00 |

Buy |

Constructive. Positive on record backlog and gross margin expansion after Q1 results. |

|

Jefferies |

$12.00 |

Hold |

Cautious. Downgraded after the space-sector rally pushed valuation above its prior target. |

|

Cantor Fitzgerald / Colin Canfield |

$9.00 |

Neutral |

Cautious. Sees limited upside due to dilution risk and negative EBITDA. |

|

BofA Securities / Ronald Epstein |

$6.00 |

Underperform |

Bearish. Cites valuation risk and execution challenges. |

|

Wall Street consensus |

~$14.44 to $15.71 median |

Buy |

Broadly constructive. Reflects strong space demand, but also a wide target range after the ATM announcement. |

|

Bear scenario |

$6.00 to $8.00 |

N/A |

Cautious. Assumes further dilution, slower backlog conversion, or a broader space and defense sentiment reset. |

How to Trade Redwire (RDW) Stock Futures on BingX TradFi

As Redwire navigates the integration of Edge Autonomy, a record backlog, Golden Dome-related contract flow, and a large ATM equity program, tactical traders can capitalize on its sharp bidirectional moves through the BingX TradFi platform.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select Redwire (RDW). Search for and select the RDW-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect Redwire to convert backlog into revenue, secure additional Golden Dome and NATO contracts, and turn adjusted EBITDA positive. Select Open Short if you expect further dilution, weak Q2 execution, or a broader space and defense sentiment reset.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. Because RDW has already shown 60% single-week moves in 2026, conservative leverage and clear position sizing are important.

Step 5: Execute strict risk protocols. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. RDW can react quickly to earnings, contract announcements, missile defense budget headlines, ATM issuance updates, and SpaceX-linked space-sector sentiment.

Top 5 Risks to Consider Before Investing in Redwire Stock

Redwire has one of the more compelling backlog and contract profiles among small-cap space and defense stocks, but RDW also carries major risks tied to dilution, execution, valuation, insider activity, and sector sentiment.

- Dilution from the $500 million ATM equity program: Redwire's June 2026 announcement of a $500 million at-the-market equity program, on top of an earlier follow-on offering of about 25.5 million shares at $7.23, creates ongoing dilution risk that could weigh on per-share metrics if issuance is aggressive.

- Adjusted EBITDA is still negative: Despite Q1 2026 revenue growth of nearly 58%, Redwire's adjusted EBITDA was negative $9.2 million and GAAP net loss was $76.5 million. Even excluding non-recurring Edge Autonomy charges, the business has not yet demonstrated sustained operating profitability.

- Valuation is stretched after the 2026 rally: RDW rallied more than 220% at its peak earlier in 2026, pushing the stock to roughly 7 times sales, in line with high-growth defense peers. Multiple compression could be sharp if execution disappoints or the SpaceX IPO-driven sector enthusiasm fades.

- Insider selling has been concentrated at large holders: The RED Holdings vehicle recorded 35 sales over the trailing six months, disposing of roughly 85 million shares for an estimated $916 million. While CEO Peter Cannito and other executives have been small net buyers, large insider distribution can still weigh on sentiment.

- Program and budget risk affects the defense pipeline: Redwire's exposure to SHIELD, Golden Dome, and other U.S. Missile Defense Agency programs is a bull-case catalyst, but it also means the company is exposed to federal budget timing, procurement delays, and policy shifts that can affect the pace of revenue conversion.

Final Thoughts: Is Redwire Stock a Buy in 2026?

As of July 2026, Redwire Corporation (RDW) is one of the more polarizing names in the small-cap space and defense complex. Its record $498 million backlog, 1.92 book-to-bill ratio, expanding gross margin, Edge Autonomy integration, NATO Penguin Mk3 contract, and SHIELD and Golden Dome exposure all point to a business benefiting from powerful multi-year tailwinds in space infrastructure and defense modernization. The 2026 revenue guidance of $450 million to $500 million would represent roughly 42% year-over-year growth at the midpoint.

The risk is that RDW's rally has already priced in a lot of that story, while the underlying business is still adjusted EBITDA-negative and diluting shareholders through a $500 million ATM program. Analyst targets remain widely dispersed, from Cantor Fitzgerald's $9 and BofA's $6 on the cautious side to HC Wainwright's $22 on the bullish side, with the consensus clustered around $14 to $16. For traders, RDW futures on BingX TradFi offer a way to trade around Q2 earnings, contract wins, ATM issuance updates, and space-sector sentiment. For longer-term investors, the key question is whether Redwire can convert its record backlog and Golden Dome exposure into sustained, cash-generative growth without letting dilution or execution setbacks reset the story.

Related Reading

- Top Space Stocks to Buy Ahead of SpaceX IPO

- How to Trade SpaceX (SPCX) Using Crypto: A Complete Beginner’s Guide (2026)

- What Is SpaceX Tokenized Stock (SPCXB) and How to Buy SPCX Tokenized Stock?

- SpaceX (SPCX) Price Prediction 2026: $227 Street-High AI Fusion or Trillion-Dollar Valuation Bubble?

- Firefly Aerospace Stock Outlook 2026: Can Launch Vehicles, Spacecraft Services Drive FLY to $45+?

- Rocket Lab Stock Forecast 2026: Can RKLB's Space Infrastructure Play Break $150 After Its 400% Run?