In early June 2026, Rocket Lab USA (RKLB) holds a rare position in the commercial space market. Once known mainly as a small-launch upstart, the company has become a credible end-to-end space infrastructure provider with more than $2 billion in contracted backlog. Its growth story now extends beyond Electron launches to Space Systems, defense partnerships, and the upcoming debut of its medium-lift Neutron rocket. After a roughly 400% stock gain over the past year, the key question is whether RKLB can keep growing into its valuation.

The bull case is that Rocket Lab is one of the few public companies building across launch services, spacecraft platforms, satellite components, and national security space infrastructure at the same time. Analysts including Stifel have raised price targets, with Neutron execution seen as the main driver of long-term upside. The risk is that Rocket Lab has not yet launched a medium-lift rocket, remains loss-making, and already trades at a valuation that prices in major future success. This guide breaks down the Rocket Lab stock forecast, 2026 price scenarios, key risks, and how to trade RKLB stock futures on BingX TradFi with USDT collateral.

Why Is Rocket Lab (RKLB) Stock Surging in 2026?

Rocket Lab’s 2026 rally is driven by stronger financial execution, rising defense demand, progress toward Neutron’s first launch, and a broader re-rating of commercial space stocks.

- Rocket Lab is proving it can grow beyond Electron launches: Rocket Lab’s Q1 2026 revenue reached $200.3 million, up 63.5% year over year and above guidance. Space Systems delivered $136.7 million, while Launch Services reached $63.7 million. Record gross margins also showed that the company’s business mix is shifting toward higher-value satellite platforms, components, and infrastructure services.

- The $2.2 billion backlog gives RKLB stronger revenue visibility: Rocket Lab’s backlog climbed above $2.2 billion, more than doubling year over year. The company secured 31 new Electron and HASTE missions plus five Neutron contracts, including its largest launch deal to date. This gives investors more confidence that demand is not limited to short-term launch cadence.

- Defense contracts are turning Rocket Lab into a national security space supplier: Rocket Lab’s selection for the Space-Based Interceptor program and its partnership with Anduril for HASTE hypersonic launches show that the company is gaining strategic defense relevance. These contracts can support longer-duration revenue, stronger margins, and a higher valuation framework than commercial launch alone.

- Neutron remains the biggest upside catalyst and execution test: Management is still targeting a Q4 2026 first launch for Neutron, with Archimedes engine testing, AFP-manufactured components, and the Return on Investment landing barge all progressing. If successful, Neutron could move Rocket Lab from a small-launch leader into the medium-lift market, but any delay would directly pressure the bull case.

- The SpaceX IPO narrative is lifting the entire commercial space sector: SpaceX’s expected IPO has brought more institutional attention to listed space companies. As one of the few public pure-play alternatives to SpaceX, RKLB has benefited from renewed demand for commercial space infrastructure exposure and a broader sector re-rating.

Read More: Top Space Stocks to Buy Ahead of SpaceX IPO

What Is Rocket Lab?

Rocket Lab USA, Inc. (Nasdaq: RKLB) is a Long Beach, California-based space company operating across two core segments: Launch Services and Space Systems. Founded by Peter Beck in New Zealand in 2006 and listed on Nasdaq in 2021, Rocket Lab has become one of the most active launch providers in the Western market after SpaceX. Its Electron rocket serves the dedicated small-launch market, with launch operations in New Zealand and Virginia.

Rocket Lab is more than a launch company. Over the past several years, it has built a vertically integrated space infrastructure business that covers satellite platforms, spacecraft components, mission management, electric propulsion, solar panels, reaction wheels, and star trackers. Recent acquisitions such as Mynaric for optical communications and Motiv Space Systems for space robotics have expanded this Space Systems portfolio further.

As of 2026, Rocket Lab’s core markets include dedicated small-lift launch through Electron, future medium-lift launch through Neutron, hypersonic test flights through HASTE, national security satellite platforms, and components sold to third-party spacecraft manufacturers.

Rocket Lab’s Performance in Early 2026: Strong Q1 Results Before Neutron Launch

Rocket Lab entered 2026 with strong momentum, and Q1 showed that growth was accelerating. Revenue reached $200.3 million, crossing the $200 million quarterly mark for the first time. Growth was supported by record bookings and rising Space Systems contributions from SDA Tranche II and III contracts. Adjusted EBITDA loss also narrowed to $11.8 million, much better than the $25.1 million consensus estimate, showing improving operating leverage before Neutron has even launched.

For Q2 2026, management guided revenue of $225 million to $240 million, again ahead of analyst expectations, with GAAP gross margin expected at 33% to 35%. Rocket Lab also held about $1.48 billion in cash and equivalents, with access to more than $2 billion in total liquidity. This gives the company enough runway to fund Neutron development without relying on near-term dilutive financing.

Neutron remains the key execution milestone. Rocket Lab plans to attempt a soft-splashdown reusability test on Neutron’s first flight, followed by a barge-catch attempt on the second flight. If successful, this staged reusability strategy could help Rocket Lab move closer to the economics that made SpaceX’s Falcon 9 model so powerful.

Rocket Lab’s 2026 Trading Strategy: Navigating the Neutron Inflection

To trade Rocket Lab’s 2026 rally, investors need to watch three forces: whether Neutron stays on schedule, whether defense and Space Systems contracts keep expanding the backlog, and whether SpaceX IPO-driven sentiment creates better entry or exit points.

1. The $95 to $105 Zone Is the Key Support Floor

Technical analysts see $95 to $105 as the near-term support range, where the 50-day moving average overlaps with the breakout level after Q1 earnings. RKLB’s 52-week range of $25.24 to $151.00 shows how sensitive the stock is to news flow. A decisive break below $95 could open downside toward $75 to $80, while confirmed support above $100 would strengthen the setup heading into the Neutron launch window.

2. The Main Valuation Debate Is Space Infrastructure Premium vs. Neutron Execution Risk

Bulls value Rocket Lab as an end-to-end space infrastructure company with launch, satellite systems, defense, and medium-lift upside. Bears argue that Neutron has not yet flown, the company remains loss-making, and elevated revenue multiples leave little room for delays. For swing traders, a volume-confirmed move above $130 would suggest the market is pricing in a successful Neutron launch, not just anticipation.

3. SpaceX IPO Sentiment Can Amplify RKLB Volatility

Rocket Lab has benefited from the SpaceX IPO narrative as investors look for public space-sector exposure. However, a SpaceX listing could also pull capital away from RKLB if investors rotate into the primary asset. Position sizing should account for binary catalysts such as Neutron launch results, Golden Dome contract updates, and SpaceX IPO developments, rather than relying only on backlog growth.

Read More: How to Trade SpaceX Pre-IPO on BingX Pre-IPO: SPACEX (VNTL), SPACEX (PreStocks), and SPCX

The Rocket Lab 2026 Forecast: $150+ Space Infrastructure Upside vs. $60 Execution Risk Floor

Rocket Lab’s 2026 price outlook depends on one central question: can Neutron complete its first launch and turn pre-signed contracts into a durable medium-lift business? The bull case rests on a successful Neutron debut, continued defense contract momentum, and broader investor interest in space stocks. The bear case centers on Neutron delays, slower backlog conversion, and valuation compression if investors rotate away from high-growth, loss-making companies.

The Bull Case: RKLB Breaks Above $150 on Neutron Success

The bullish scenario depends on Neutron reaching the pad and completing a technically successful first launch, even if full reusability comes later. Five pre-signed Neutron contracts, the Anduril partnership, and Raytheon’s Golden Dome selection all support the view that demand for non-SpaceX medium-lift capacity is real. Stifel raised its price target to a street-high $132, while Clear Street lifted its target to $129.

If Neutron launches successfully and Rocket Lab wins more national security missions, RKLB could move toward $150 or higher as the market begins pricing in reusable medium-lift economics. Longer-term upside depends on whether Rocket Lab can turn Neutron from a development milestone into a scalable launch business.

The Base Case: RKLB Consolidates Between $95 and $130

The base case is volatile consolidation. Space Systems and Electron continue growing, backlog remains strong, and defense contracts keep supporting the revenue story. However, investors may wait for Neutron to fly before giving Rocket Lab full credit as a medium-lift launch provider.

Under this scenario, RKLB trades between roughly $95 and $130 as the market balances strong operating momentum against the lack of Neutron revenue. Wall Street’s consensus target near $102 to $110 reflects this cautious but constructive view, with mostly Buy and Hold ratings.

The Bear Case: RKLB Falls Toward $60 on Neutron Delay or Market Rotation

The bearish scenario starts with Neutron missing its launch window or facing another major technical delay. If the first launch slips into 2027, investors could revalue Rocket Lab as an Electron and Space Systems business rather than a future medium-lift competitor.

Valuation is the second major risk. With RKLB trading at elevated revenue multiples, the stock is highly sensitive to rising real rates, weaker risk appetite, or rotation out of speculative growth names. If Neutron is delayed, space-sector sentiment cools, and competitors such as Blue Origin or Firefly gain ground, RKLB could retrace toward $60, where more traditional aerospace growth multiples would apply.

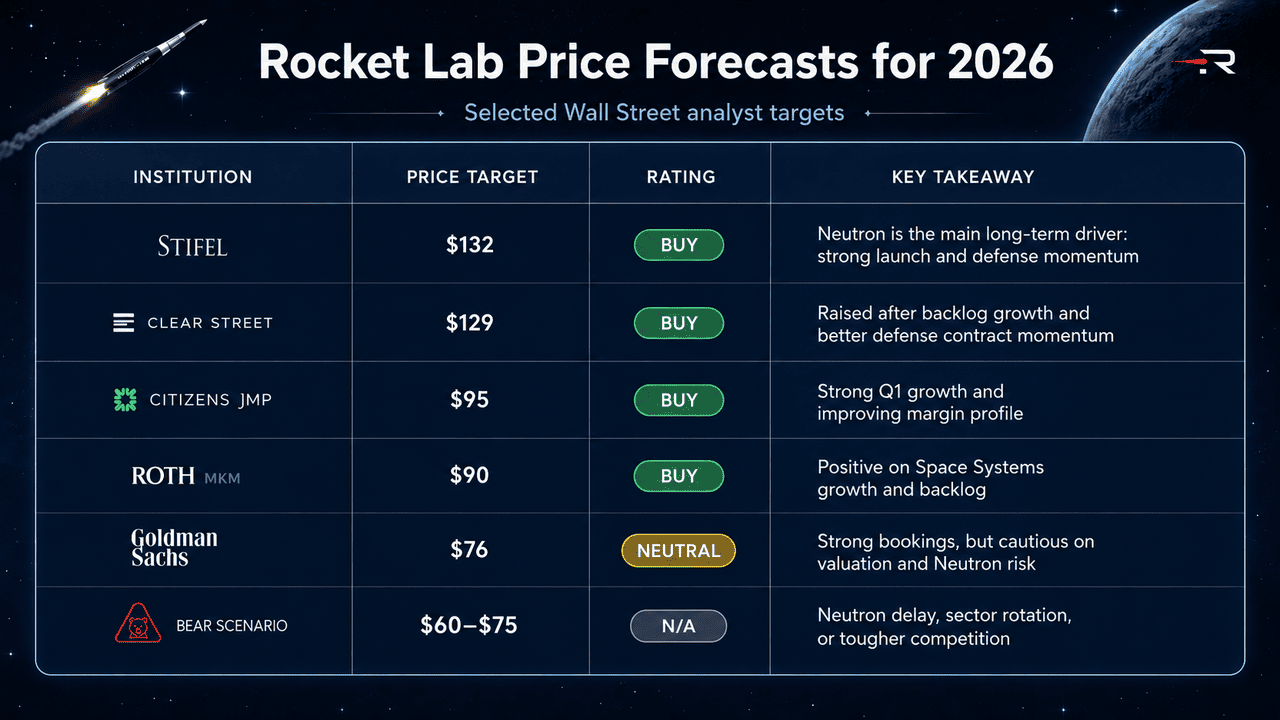

Rocket Lab Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Analyst |

Price Target |

Rating |

Market Outlook |

|

Stifel / Erik Rasmussen |

$132 |

Buy |

Bullish. Sees Neutron as the main long-term value driver, supported by strong launch execution, Space Systems growth, and expanding defense exposure. |

|

Clear Street |

$129 |

Buy |

Bullish. Raised its target from $98 after stronger backlog growth and improving defense contract momentum. |

|

Citizens JMP / Trevor Walsh |

$95 |

Buy |

Constructive. Highlights 63% Q1 revenue growth, improving EBITDA margin, and diversification beyond launch into defense and space systems. |

|

Roth MKM / Sujeeva De Silva |

$90 |

Buy |

Constructive. Positive on Space Systems growth, rising backlog, and long-term demand for satellite components and platforms. |

|

Goldman Sachs / Noah Poponak |

$76 |

Neutral |

Cautious. Recognizes strong bookings and improving metrics, but remains cautious on valuation and Neutron execution risk. |

|

Bear Scenario |

$60-$75 |

N/A |

Cautious. Assumes Neutron delay, sector rotation out of high-multiple growth stocks, or rising competition from Blue Origin and Firefly in medium-lift launch. |

How to Trade Rocket Lab (RKLB) Stock Futures on BingX TradFi

As Rocket Lab approaches the highest-stakes launch in its history alongside a rapidly growing defense business, tactical traders can take advantage of its sharp bidirectional volatility through the BingX TradFi platform.

- Access BingX TradFi: Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

- Select Rocket Lab (RKLB): Search for and select the RKLB-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe Neutron's Q4 2026 first launch, continued defense contract wins, and the SpaceX IPO halo will drive RKLB toward street-high targets above $130 to $150. Select Open Short to capitalize on potential Neutron timeline slippage, post-rally valuation compression, or macro-driven sector rotation.

- Select Leverage and Margin Mode: Apply your preferred Isolated or Cross-Margin parameters alongside disciplined leverage ratios to maximize capital efficiency while controlling liquidation risk.

- Execute Strict Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in gains and protect against sudden overnight gap events tied to Neutron test results, NASA or DoD contract announcements, and SpaceX IPO developments that routinely move the entire space equity sector.

Top 5 Risks to Consider Before Investing in Rocket Lab Stock

Rocket Lab has one of the strongest growth stories in commercial space, but RKLB also carries major risks tied to Neutron execution, valuation, competition, cash burn, and defense contract timing.

- Neutron launch risk: Neutron is the main driver of Rocket Lab’s medium-term valuation. A delay or launch failure could force the market to remove the medium-lift premium and revalue RKLB based mainly on Electron and Space Systems.

- Valuation compression risk: RKLB trades at a high revenue multiple, leaving little room for execution mistakes. Rising real rates, weaker growth-stock sentiment, or a revenue miss could pressure the stock quickly.

- SpaceX competition and IPO risk: Rocket Lab has benefited from being a public SpaceX proxy, but a SpaceX IPO could pull investor flows away from RKLB. SpaceX’s reusable launch economics also remain a long-term competitive ceiling.

- Cash burn and dilution risk: Rocket Lab has a strong cash position, but Neutron development remains capital-intensive. Cost overruns, delays, or revenue shortfalls could increase the risk of future equity financing.

- Defense program execution risk: Golden Dome and SDA contracts can support higher-margin growth, but government programs come with procurement delays, budget risk, and shifting defense priorities that could push out revenue recognition.

Final Thoughts: Is Rocket Lab Stock a Buy in 2026?

As of June 2026, Rocket Lab (RKLB) is one of the most compelling public space infrastructure stocks. Its record Q1 revenue, $2.2 billion backlog, Golden Dome selection, Anduril partnership, and five pre-signed Neutron contracts show that the company has expanded beyond small-lift launch into a broader space systems and defense platform. Stifel’s street-high $132 target reflects growing confidence that Neutron could become a major Western medium-lift rocket if execution stays on track.

The risk is that Rocket Lab still has to prove the hardest part. Neutron has not launched, the company remains loss-making, and RKLB trades at a valuation that leaves little room for delays. A successful Q4 2026 Neutron debut could support further upside toward $150 or higher, while a delay or failure could push the stock back toward Goldman’s $76 target or lower. For active traders, RKLB futures on BingX TradFi offer a high-volatility way to trade both directions around these catalysts; for longer-term investors, the core question is whether Rocket Lab can turn Neutron from a development milestone into a scalable medium-lift business.

Related Reading

- Top Space Stocks to Buy Ahead of SpaceX IPO

- How to Trade SpaceX Pre-IPO on BingX Pre-IPO: SPACEX (VNTL), SPACEX (PreStocks), and SPCX

- Should You Participate in SpaceX IPO: Pros and Cons

- Firefly Aerospace Stock Outlook 2026: Can Launch Vehicles, Spacecraft Services Drive FLY to $45+?

- AST SpaceMobile Stock Outlook 2026: Can BlueBird, Space-to-Phone Services Drive ASTS to $130+?