The global agricultural matrix in mid-2026 is grappling with contraction, supply imbalances, and shifting localized weather patterns. Wheat (Wheat), the foundational metric for global food security, is entering a highly complex 2026/27 marketing year characterized by shrinking aggregate production and tightening ending stocks.

While severe droughts have hammered output across key Western exporters, pushing some crops to multi-decade lows, persistent, heavy output from the Black Sea region and improved localized rainfalls are keeping a definitive lid on runaway prices. For global commodity traders, structural volatility across key benchmarks remains closely tied to near-term crop progress reports, changing animal feed economics, and the ultimate realization of the Northern Hemisphere harvest.

Read more: How to Trade Commodities With Crypto in 2026 as Oil, Gold, Silver, and TradFi Go On-Chain

Key Highlights: Top 5 Things for Wheat Investors to Know in 2026

- Shrinking Global Production Track: Global Wheat (Wheat) production for the 2026/27 season is forecast at approximately 820 million metric tons (MMT) by the International Grains Council (IGC). This marks a 3% drop (roughly 24 MMT) from the previous season’s record-shattering high of 842+ MMT.

- U.S. Output Hits a 54-Year Structural Low: A severe, widespread drought primarily impacting Hard Red Winter (HRW) crops has crippled American output. Total U.S. all-wheat production is projected at its lowest level since the 1972/73 season, severely constraining U.S. export capacity.

- Black Sea Dominance Caps Upside: Despite global deficits, Russia continues to dictate baseline export pricing. With private estimates pushing Russian production back toward 90 MMT, abundant near-term supplies are preventing sustained bullish contract breakaways.

- Tightening Global Ending Stocks: Aggregated balance sheets are showing structurally leaner reserves. The USDA pegs upcoming 2026/27 global ending stocks at 275 MMT, down from the previous year's 279 MMT baseline, while the IGC tracks an even sharper downshift to 282 MMT.

- Flattening Feed Demand in Importing Regions: High Western cash prices have disrupted standard substitution ratios. Major importers across Southeast Asia are actively scaling back Wheat (Wheat) allocations intended for livestock feed, shifting heavily into more competitive coarse grains like corn.

Read more: How to Invest in Gold on BingX: A 2026 Beginner’s Guide

Understanding Global Wheat Benchmarks

Source: USDA

The international trade of Wheat (Wheat) is not uniform; it relies on distinct pricing nodes that reflect localized grain varieties, protein structures, and transport logistics:

- Chicago Board of Trade (CBOT) Soft Red Winter: The global foundational benchmark for baseline milling and feed quality.

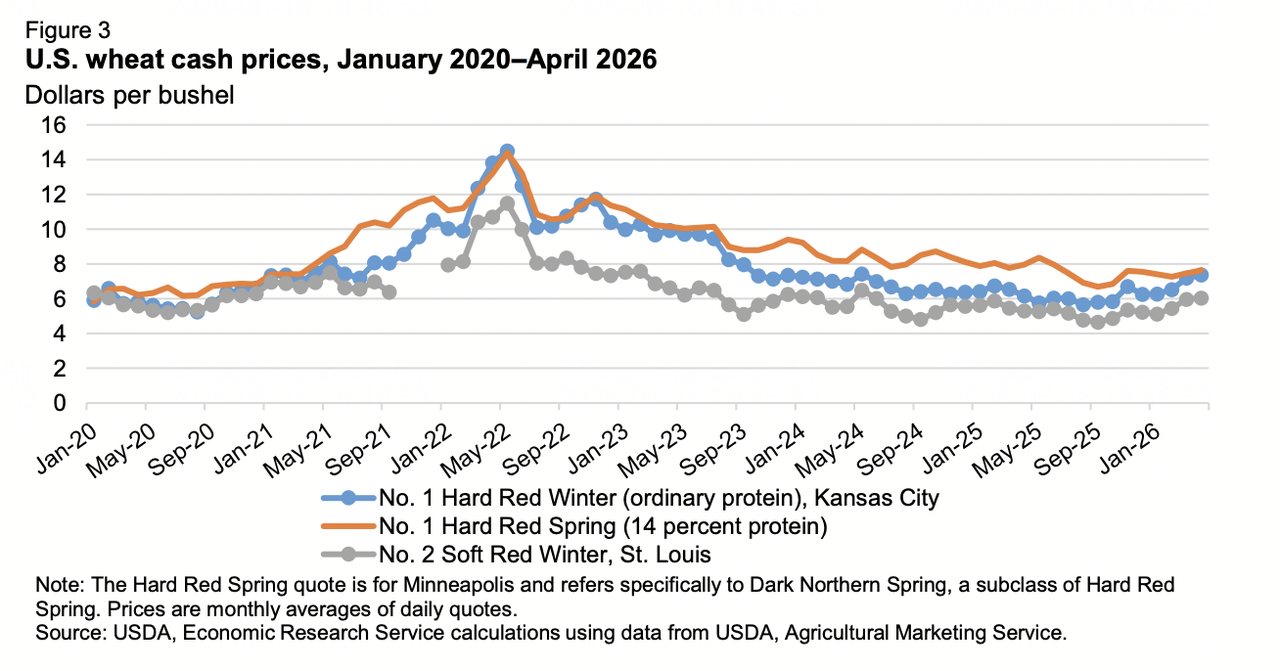

- Kansas City Board of Trade (KCBT) Hard Red Winter: The premium standard for industrial breadmaking, currently bearing the brunt of North American environmental strains.

- Minneapolis Grain Exchange (MGEX) Hard Red Spring: High-protein spring varieties prized for blending, largely reflecting northern plains weather premiums.

Source: USDA

Key Supply and Demand Drivers for Wheat by Region

The Americas: Severe Historical Droughts

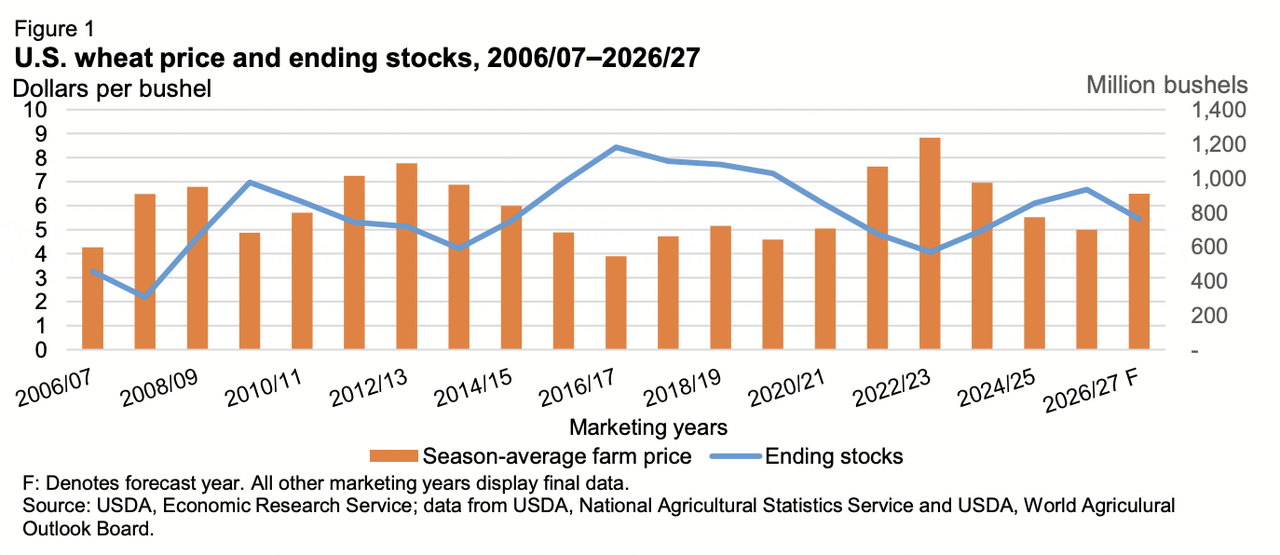

The United States is managing an exceptional structural supply squeeze. Driven by failing yields and reduced acreage, with all-wheat planted area hitting its lowest footprint since 1919, the U.S. winter crop is trending at its smallest size since 1965. Yield expectations have been trimmed 5% to 50.8 bushels per acre. Consequently, the USDA projects U.S. exports to hit a multi-year low of 21.5 MMT (775 million bushels), driving the projected domestic season-average farm price up to a 3-year high of $6.50 per bushel.

The Black Sea: Aggressive Pricing Power

Russia remains the world's undisputed leading exporter, forecast to ship a massive 47 MMT. While yields are down roughly 5% from historical peaks, private analytical desks are building a strong case for a 90 million tonne aggregate crop as spring conditions improve. Meanwhile, the Ukrainian Grain Association projects domestic production at 22.8 million tonnes. However, Ukraine's actual export chain (projected at 13 MMT of shipped volume) remains fundamentally constrained by logistical bottlenecks, high risk premiums, and damaged agricultural infrastructure.

Europe and Australia: Weather Transitions

European common wheat expectations have been trimmed down to 128.8 MMT following unseasonably dry spring conditions across central crop monitors. In the Southern Hemisphere, Australia’s ABARES has projected a sharp 26% year-over-year production plunge to 26.7 MMT due to crippling early-season dryness. However, substantial winter rain events are sparking late-stage recovery hopes. Elsewhere, South America presents a stable front, with Argentina’s planting completing smoothly under excellent soil moisture parameters.

Historical Backtesting: Recapping the Disruptive 2025/26 Cycle Adjustments

To understand the current tightness in the 2026/27 landscape, traders must review the volatile data corrections that concluded the previous 2025/26 marketing year. Recent updates by the USDA showcase how hidden consumption surges and trade flow accelerations eroded global balance sheets faster than initially modeled.

- The Chinese Substitution Surge: The largest demand shock came from China, where domestic feed and residual consumption spiked by 2.0 MMT to a massive 33.0 MMT. This trend occurred because global Wheat (Wheat) values had crashed to multi-year lows relative to domestic corn, prompting Chinese industrial livestock operations to aggressively substitute corn for wheat in animal feed rations.

- Production Rebalancing Act: Global production for 2025/26 settled at 843.8 MMT. Minor adjustments saw a downgraded Turkish crop (falling 0.7 MMT to 16.8 MMT) mostly offset by a surprise bumper crop in the United Kingdom, which rose to 12.3 MMT. However, structural demand heavily outpaced these marginal supply changes.

- Global Inventory Eradication: Accelerated trade dynamics eroded global reserves far quicker than anticipated. Trade tracking revealed brisk shipping velocities, pushing total exports to 224.4 MMT. Russia (up to 46.0 MMT), Canada (up to 30.0 MMT), and Kazakhstan (up to 12.0 MMT) cleared out heavy volumes, outperforming slower tempos outside of Argentina and Australia.

- The Stockpile Drain: This convergence of relentless livestock feed usage in Asia and aggressive export liquidations forced a massive 3.9 MMT downward revision to global 2025/26 ending stocks, reducing them to 279.2 MMT. This drawdown was led primarily by significant storage drops in China, Kazakhstan, and Russia, setting a vulnerable, lower-stock foundation for the current year.

Wheat Commodity Pricing Profile as of Mid-2026

The fundamental marketplace highlights a heavily compressed, range-bound pricing structure across major international trading desks.

|

Futures and Cash Benchmarks |

Operational Position / Data |

|

Chicago July Contract (CBOT) |

$5.84 / bushel |

|

Trading Economics Benchmark |

$5.95 / bushel |

|

Minneapolis Spring Wheat (MGEX) |

$6.18 / bushel |

|

Canadian Western Red Spring (CWRS 1, 13.5%) |

~$275 / tonne (Saskatchewan Spot) |

|

Ontario Soft Red Winter (SRW) Bids |

~$7.00 - $7.04 / bushel |

|

USDA U.S. All-Wheat Farm Price Projection |

$5.00 - $6.50 / bushel range |

|

Global Ending Stocks (USDA / IGC) |

275 MMT - 282 MMT |

Shifting Wheat Importer Dynamics

The Rise of Domestic Harvests in Key Corridors

A major structural weight on international Wheat (Wheat) values in 2026 is the rapid demand deceleration across historical import hubs. Regions such as North Africa and Near East Asia, specifically Morocco, Egypt, Syria, and Turkey, are actively cutting back international purchase orders. Strong, record-breaking aggregate domestic harvests have significantly cushioned these nations, insulating their local economies and diminishing their traditional reliance on Western shipping lanes.

The Corn Displace Effect in Livestock Feed

The structural reality of lower global production has kept premium milling varieties valued at a notable premium. Because Wheat (Wheat) is underperforming on cost-competitiveness against rival coarse feed grains, major importing economies across East and Southeast Asia, such as Indonesia, Vietnam, and the Philippines, have systematically updated their import profiles. Industrial livestock operators are actively swapping out grain ratios, decreasing their aggregate wheat imports to preserve margin structures.

Market Forecasts for Wheat in 2026: Bull vs. Bear Outlook

The Bull Case: Weather Disruptions and Geopolitical Friction

The structural bull case relies heavily on the realization of localized crop failure. If late-season heat or sudden frosts hit the advancing European winter filling stage, or if the recent rain across the Australian wheat belt proves insufficient to heal early dryness, global ending stocks could contract past psychological breaking points. Furthermore, any renewed escalations or infrastructure bottlenecks across Black Sea shipping channels could instantly trigger sharp short-covering rallies across Chicago contracts.

The Bear Case: Black Sea Volume Ramps and Lacklustre Demand

The bear case assumes that the impending European and Black Sea harvests arrive without major disruption. If private estimates of a 90 MMT Russian crop materialize, the market will face a wave of near-term cash availability that could overwhelm Western pricing structures. With global consumption softening and North African import demand remaining structurally low, Wheat (Wheat) values face a prolonged period of sideways consolidation or downward price pressure.

Read more: Commodities, Forex, and Gold Heating Up On-Chain Amid 2026 Precious Metal Highs

How to Trade Wheat Futures on BingX TradFi

The TradFi architecture on BingX provides a highly fluid, modern infrastructure for entering agricultural commodity markets using USDT-settled perpetual contracts, allowing traders to circumvent old-world futures brokerage loops.

Long or Short Wheat Perpetuals with USDT on BingX Futures

Wheat (Wheat) perpetual contract on BingX futures market

- Navigate to the BingX trading platform and navigate directly to the TradFi Stock/Commodity Futures interface.

- Select the Wheat (Wheat) perpetual contract.

- Verify active trading sessions before submitting order tickets. Spreads and localized volatility may widen during extended-hour sessions due to lower immediate order book density.

- Configure your preferred Margin Mode (Isolated for defined boundary isolation, or Cross for collective portfolio pooling) and select leverage metrics.

- Execute Open Long if you anticipate positive backlog conversions, consecutive earnings outperformance, or strong margin guidance updates. Execute Open Short if you look to hedge against tech sector pullbacks, overextended valuations, or potential manufacturing execution friction.

- Implement protective Take-Profit (TP) and Stop-Loss (SL) boundary parameters immediately upon order entry to shield capital configurations from sudden macro market swings.

Conclusion: Navigating the 2026 Wheat Market on BingX

The global Wheat (Wheat) market in 2026 presents a classic fundamental standoff. While structurally tight balance sheets, multi-decade American production drops, and Australian weather anxieties provide a solid long-term floor, the immediate pricing reality is kept in check by robust Black Sea shipping volumes and insulated importing nations.

For commodity participants, success in this environment requires tracking localized weather developments across the Northern Hemisphere plains alongside structural global export velocities.

Risk Reminder: Trading agricultural commodities involves extreme exposure to environmental unpredictability, government export interventions, and geopolitical policy adjustments. Always engage in comprehensive risk management and deploy protective trading protocols across all positions.

Related Reading

- How to Trade Gold Futures With Crypto: A Beginner's Guide for 2026

- How to Trade Forex, Commodities, Stocks, and Indices With BingX TradFi: A Beginner’s Guide (2026)

- Is Gold a Good Investment in 2026? Risks & Returns Explained

- Commodities, Forex, and Gold Heating Up On-Chain Amid 2026 Precious Metal Highs