Artificial intelligence (AI) has moved from a software story to a hardware bottleneck. In 2026, the AI trade is increasingly defined by the semiconductor companies that make large-scale AI infrastructure possible, from ASML’s EUV machines and TSMC’s advanced manufacturing to NVIDIA’s GPU ecosystem, Broadcom’s custom AI silicon, and Marvell’s data center interconnects. With hyperscaler capex approaching $700 billion, the biggest opportunities are concentrated across a small number of companies controlling critical layers of the AI chip supply chain.

At the same time, access to these semiconductor leaders is becoming more flexible through crypto-native trading rails. BingX TradFi lets users trade leading U.S. stock futures with USDT, while tokenized stocks provide another way to gain equity price exposure without a traditional brokerage account. This guide breaks down the 2026 AI semiconductor supply chain, the eight stocks that matter most, the structural trends driving the cycle, and the key risks investors should understand before trading them.

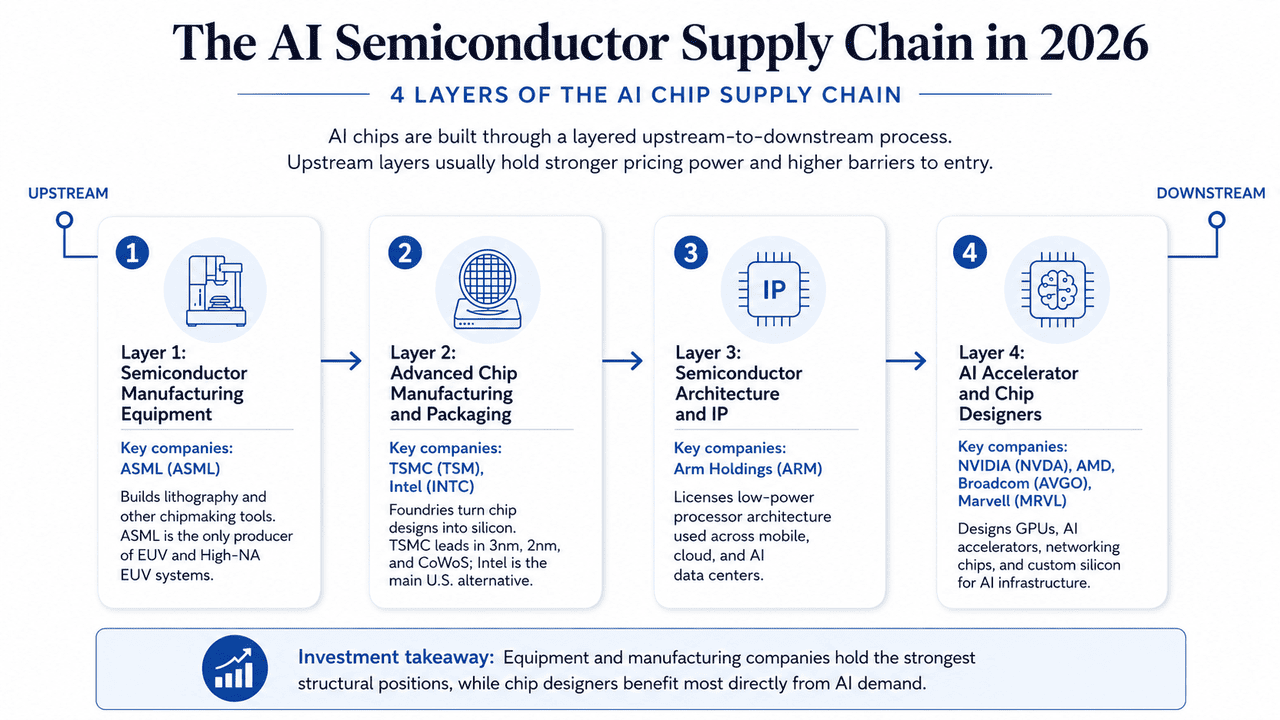

The AI Semiconductor Supply Chain in 2026: 4 Layers of the AI Chip Supply Chain

Before looking at individual AI semiconductor stocks, it helps to map the chip supply chain first. Modern AI chips depend on four main layers: equipment, manufacturing and packaging, architecture and IP, and chip design. Each layer has a different role in the AI hardware cycle, from upstream bottlenecks like EUV lithography to downstream competition among GPU, ASIC, and networking chip designers.

Layer 1: Semiconductor Manufacturing Equipment

Key companies: ASML (ASML)

Advanced chip production starts with the machines that make semiconductor manufacturing possible. Equipment suppliers provide lithography, deposition, etching, and metrology systems, making this one of the most technically demanding and concentrated parts of the chip supply chain. ASML is the key company in this layer because it is the only producer of EUV and High-NA EUV lithography systems, which are required for leading-edge chip production. These machines are essential for manufacturing advanced AI accelerators at sub-3nm process nodes.

Layer 2: Advanced Chip Manufacturing and Packaging

Key companies: TSMC (TSM), Intel (INTC)

Once a chip is designed, foundries turn that blueprint into physical silicon using advanced process nodes and packaging technologies. Manufacturing yield, process leadership, and packaging capacity all determine whether AI chips can be produced at scale. TSMC remains the leader in advanced manufacturing, including 3nm production, 2nm ramp-up, and CoWoS advanced packaging. Intel is working to become the main U.S.-based alternative through its 18A and future 14A process roadmap.

Layer 3: Semiconductor Architecture and IP

Key companies: Arm Holdings (ARM)

Before chip designers build final products, many rely on licensed processor architectures and semiconductor IP. These businesses do not manufacture chips directly; instead, they earn licensing and royalty revenue as their architectures are adopted across different end markets. Arm is the key company in this layer, with low-power processor architecture used across smartphones, embedded devices, cloud infrastructure, and increasingly AI data centers. Custom chips from AWS, Google, and Microsoft all rely on Arm-based designs.

Layer 4: AI Accelerator and Chip Designers

Key companies: NVIDIA (NVDA), Advanced Micro Devices (AMD), Broadcom (AVGO), Marvell Technology (MRVL)

At the downstream end of the supply chain, fabless companies design the AI accelerators, GPUs, networking chips, and custom silicon that power modern AI infrastructure. These companies outsource manufacturing to foundries such as TSMC while competing on performance, software ecosystems, efficiency, and customer adoption. NVIDIA leads in general-purpose AI compute with Hopper, Blackwell, and future Rubin GPUs. AMD competes through MI-series accelerators and EPYC CPUs, Broadcom focuses on hyperscaler custom AI chips, and Marvell provides networking and optical interconnect solutions for large-scale AI clusters.

AI Semiconductor Supply Chain Trends in 2026: Inference, HBM, and Advanced Packaging

Several structural shifts are reshaping where pricing power and long-term value accumulate across the AI semiconductor supply chain in 2026.

1. AI Inference Demand Is Overtaking Training

AI infrastructure demand is increasingly driven by inference rather than training as agentic AI systems, reasoning models, and enterprise AI applications scale globally. This shifts industry focus from raw compute performance to performance-per-watt and cost-per-token efficiency, benefiting companies like NVIDIA as it prepares its Vera Rubin AI platform.

2. High-Bandwidth Memory (HBM) Has Become a Bottleneck

HBM has become one of the most supply-constrained parts of the AI hardware stack, with production concentrated among Micron Technology, SK hynix, and Samsung Electronics. Tight supply and surging AI accelerator demand have transformed memory from a cyclical commodity business into a higher-margin pricing-power story.

3. Advanced Packaging Is Becoming as Important as Process Nodes

As transistor scaling becomes more difficult, advanced packaging technologies such as CoWoS, chiplets, and 3D stacking are becoming critical performance bottlenecks for AI accelerators. TSMC’s dominance in advanced packaging capacity has become a major competitive advantage across the AI supply chain.

4. Hyperscalers Are Building More Custom AI Chips

Large cloud companies such as Google, Meta, Amazon, and Microsoft are increasingly designing custom AI accelerators optimized for specific inference workloads rather than relying entirely on general-purpose GPUs. This trend has significantly benefited Broadcom in custom AI silicon and Marvell Technology in networking and optical interconnect infrastructure.

What Are the Top 8 AI Semiconductor Stocks to Watch in 2026?

The companies below are organized by their position in the AI semiconductor supply chain, starting upstream with equipment and moving downstream through manufacturing, architecture, and chip design. This structure matters because upstream layers generally hold stronger pricing power, higher barriers to entry, and more durable competitive advantages. All eight companies are accessible through BingX TradFi USDT-margined stock futures.

1. ASML Holding (ASML)

Core Role: EUV and High-NA EUV lithography monopoly

Supply Chain Layer: Layer 1 - Semiconductor Manufacturing Equipment

ASML sits at the most structurally powerful point in the semiconductor supply chain. The company is the world’s only producer of EUV lithography systems, which are required to manufacture advanced AI chips below the 3nm node. High-NA EUV systems, essential for next-generation process nodes, now cost hundreds of millions of euros per machine, reinforcing ASML’s pricing power and technological moat.

Demand remains driven by foundries and memory manufacturers racing to expand AI infrastructure capacity. The company reported €8.8 billion in Q1 2026 revenue at a 53% gross margin and raised full-year guidance to €36–40 billion. Despite geopolitical export restrictions affecting China, ASML exited 2025 with a backlog above €38 billion, supported by long-term demand from customers including TSMC, Samsung, and SK hynix.

Read More: ASML Holding (ASML) Stock Price Forecast 2026: AI Infrastructure King or Geopolitical Target?

2. Taiwan Semiconductor Manufacturing (TSM)

Core Role: Pure-play foundry and advanced packaging leader

Supply Chain Layer: Layer 2 - Advanced Manufacturing and Packaging

TSMC is the manufacturing backbone of the global AI industry. The company physically fabricates chips for NVIDIA, AMD, Apple, Broadcom, and most leading semiconductor designers. Its dominance in advanced nodes, including 3nm volume production, 2nm ramp-up, and the future A16 node, gives it a near-irreplaceable role in AI chip production.

TSMC’s advantage is no longer limited to wafer manufacturing. Its CoWoS advanced packaging capacity has become one of the industry’s most important bottlenecks because every leading-edge AI accelerator depends on it. In 2026, TSMC raised full-year revenue growth guidance above 30% as AI-driven HPC demand overtook smartphones as its largest revenue segment for the first time in company history.

Read More: TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

3. Intel (INTC)

Core Role: Integrated device manufacturer and U.S. foundry alternative

Supply Chain Layer: Layer 2 - Advanced Manufacturing and Packaging

Intel is the most contested turnaround story in the AI semiconductor supply chain. Under CEO Lip-Bu Tan, the company has stabilized its foundry roadmap around the 18A node, while its future 14A process, using High-NA EUV, is positioned for external custom-chip customers. The strategic case is that Intel remains the only credible U.S.-based leading-edge foundry alternative to TSMC.

The Q1 2026 print improved the bull case significantly. Revenue reached $13.58 billion, up 7.18% year over year, while Data Center and AI revenue rose 22% to $5.05 billion. Intel still carries execution risk, but CHIPS Act support, defense-related demand, and supply chain diversification make the company politically and strategically important in a way most fabless chip designers are not.

Read More: Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

4. Arm Holdings (ARM)

Core Role: Energy-efficient processor architecture licensing

Supply Chain Layer: Layer 3 - Semiconductor Architecture and IP

Arm provides the processor architecture that much of the modern chip industry builds on top of. The company does not manufacture chips directly; it licenses the blueprints. As data center power constraints become more important in the AI era, Arm’s energy-efficient designs are becoming increasingly relevant for both cloud CPUs and custom silicon.

Major hyperscaler chips such as AWS Graviton, Google Axion, and Microsoft Cobalt are all built on Arm architecture. This gives Arm a royalty-driven model that scales with chip shipments across the industry. Shares surged roughly 39% in April 2026 alone as investors connected the inference pivot and custom CPU trend to Arm’s long-term royalty opportunity.

Read More: Arm Holdings (ARM) Stock Outlook 2026: AI Licensing and the $200+ Price Target

5. NVIDIA (NVDA)

Core Role: GPU design and CUDA software ecosystem

Supply Chain Layer: Layer 4 - AI Accelerator and Chip Design

NVIDIA remains the center of the AI infrastructure stack. Its GPUs power the majority of frontier training workloads and a growing share of inference, while CUDA remains the software moat that competitors have struggled to break. NVIDIA’s advantage is not only chip performance; it is also the developer ecosystem, libraries, frameworks, and platform dependency built around its hardware.

Q1 FY2027 results reinforced the thesis, with revenue reaching $81.6 billion and adjusted EPS of $1.87, ahead of expectations. The next major catalyst is the Vera Rubin platform, expected in the second half of 2026, which management says will remain supply-constrained throughout its lifecycle. NVIDIA’s market cap now reflects its role as both a hardware supplier and the operating layer of modern AI compute.

On-chain investors track this price action directly via fully backed NVIDIA's tokenized stocks like NVDAON (Ondo Finance) and NVDAX Solana-based xStock.

Read More: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

6. Advanced Micro Devices (AMD)

Core Role: Fabless GPU and CPU design

Supply Chain Layer: Layer 4 - AI Accelerator and Chip Design

AMD is the primary commercial alternative to NVIDIA in AI accelerators. Its opportunity is strongest where customers care about total cost of ownership, supply diversification, and reducing dependence on a single GPU vendor. The MI-series accelerator roadmap and EPYC server CPU franchise give AMD exposure to both AI compute and the broader data center infrastructure cycle.

Q1 2026 revenue reached $10.3 billion, up 38% year over year, while Data Center revenue surged 57% to $5.8 billion. AMD’s AI momentum accelerated after Meta announced a multi-year deployment agreement centered around the MI450 accelerator platform. Management also expects server CPU revenue to grow more than 70% in 2026 as agentic AI workloads increase CPU requirements per accelerator deployed.

Read More: AMD Price Prediction 2026: $525 AI Sovereignty or $300 Valuation Trap?

7. Broadcom (AVGO)

Core Role: Custom AI accelerators and high-speed networking silicon

Supply Chain Layer: Layer 4 - AI Accelerator and Chip Design

Broadcom is the strongest pure expression of the custom silicon thesis. Instead of competing directly with NVIDIA in general-purpose GPUs, Broadcom co-designs application-specific AI accelerators for hyperscalers, including Google’s TPU program and major custom AI deployments with companies such as Anthropic. This positions Broadcom at the center of the shift from general-purpose compute toward workload-specific inference hardware.

The financial evidence is already visible. Q1 FY2026 AI semiconductor revenue reached $8.4 billion, up 106% year over year, and management guided Q2 AI revenue to $10.7 billion. Broadcom’s $73 billion AI-specific backlog gives credibility to management’s path toward more than $100 billion in AI chip revenue in 2027.

Read More: Broadcom (AVGO) Stock Outlook for 2026: AI Infrastructure King or Margin Victim?

8. Marvell Technology (MRVL)

Core Role: Electro-optics and custom data center silicon

Supply Chain Layer: Layer 4 - AI Accelerator and Chip Design

Marvell addresses one of the least visible but most important constraints in AI data centers: moving data between thousands of accelerators. As clusters scale beyond what copper networking can efficiently support, optical interconnects and electro-optics become critical. Marvell’s portfolio is positioned directly around this connectivity bottleneck.

The bull case is that every new gigawatt of AI data center capacity requires Marvell-class networking and interconnect infrastructure, regardless of whose accelerators sit inside the cluster. The company still has exposure to more cyclical storage and consumer networking markets, but investors are increasingly focused on its electro-optics pipeline, custom ASIC programs, and role in next-generation AI cluster connectivity.

Read More: Marvell (MRVL) 2026 Outlook: Can AI & Silicon Momentum Drive Stock to $150?

2026 AI Semiconductor Stocks Comparison by Supply Chain Position

AI semiconductor stocks sit across different parts of the chip supply chain, from equipment and manufacturing to architecture and chip design. This comparison shows how each company benefits from structural bottlenecks, AI demand growth, and long-term pricing power.

|

Supply Chain Layer |

Ticker |

Core Advantage |

2026 Catalyst |

|

Equipment |

ASML |

Sole supplier of EUV and High-NA EUV lithography systems |

2026 revenue guidance raised to €36–40B; EUV demand remains structurally strong |

|

Manufacturing |

TSM |

Leading-edge foundry and CoWoS advanced packaging leader |

Full-year revenue growth guidance raised above 30% as AI/HPC demand accelerates |

|

Manufacturing |

INTC |

U.S.-based advanced foundry alternative with 18A/14A roadmap |

Q1 2026 results beat expectations; 14A positioned for external AI chip customers |

|

Architecture & IP |

ARM |

Energy-efficient CPU architecture powering hyperscaler custom chips |

AI royalty step-up and hyperscaler CPU adoption support margin expansion |

|

Chip Design |

NVDA |

CUDA ecosystem lock-in and leading AI GPU platform |

Q1 FY2027 beat; Vera Rubin ramp expected in H2 2026 |

|

Chip Design |

AMD |

MI-series AI accelerators and EPYC server CPU franchise |

Meta 6GW deployment agreement; Q2 revenue guide raised to $11.2B |

|

Chip Design |

AVGO |

Hyperscaler custom AI ASICs and networking silicon |

AI semiconductor revenue up 106% YoY; path toward $100B AI revenue run rate by FY2027 |

|

Chip Design |

MRVL |

Optical interconnects and custom data center silicon for AI clusters |

Electro-optics and ASIC pipeline expected to drive next data center growth phase |

How to Trade AI Semiconductor Stocks on BingX

BingX offers two distinct paths to gain exposure to these names without a traditional brokerage account. Tokenized stocks on the spot market track underlying shares on a 1:1 economic basis, while USDT-margined perpetual contracts on BingX TradFi provide leveraged exposure to price movement around the clock.

Buy, Sell, or HODL AI Semiconductor Tokenized Stocks on BingX Spot

For long-term investors seeking direct equity price exposure without leverage, the BingX Spot market offers access to fully backed tokenized stocks issued through regulated asset frameworks such as Backed Finance and Ondo Finance. These digital assets are designed to track real-world stock prices on a 1:1 economic basis and can be traded directly with stablecoins like USDT.

Step 1: Account setup and security. Sign up and log into your BingX account, complete the identity verification (KYC) required in your region, and enable two-factor authentication.

Step 2: Fund your spot wallet. Deposit USDT using your preferred network, e.g., TRC-20, ERC-20, or Arbitrum are common choices. Confirm minimum deposit and network fees before transferring.

Step 3: Navigate to the spot market. Search for tokenized stock pairs such as NVDAON/USDT or NVDAX/USDT for fully backed, non-leveraged exposure.

Step 4: Use the BingX AI Analyst. The embedded BingX AI tool surfaces support and resistance levels, moving averages, and volatility indicators directly on the chart to help refine entries.

Step 5: Execute and settle. Select a market or limit order, enter your USDT amount, and confirm. The tokenized stock balance populates your spot wallet immediately on fill.

Trade AI Semiconductor Stock Futures with USDT on BingX TradFi

For active traders looking to capitalize on short-term market momentum, earnings volatility, or hedging strategies, BingX TradFi allows users to trade leading U.S. stock futures with USDT. These USDT-settled perpetual contracts mirror the price movements of underlying equities, offering flexible long and short exposure without requiring users to hold the physical stock or tokenized asset.

Step 1: Access the BingX TradFi interface. Sign up, log in and navigate to the TradFi markets page or the futures trading section.

Step 2: Capital allocation. Transfer USDT from your spot wallet into the futures account, where it serves as collateral.

Step 3: Select your contract. Choose from the lineup of stock-linked perpetuals such as ASML-USDT, TSMU-USDT, INTC-USDT, ARM-USDT, NVDA-USDT, AMD-USDT, AVGO-USDT, or MRVL-USDT.

Step 4: Set direction and leverage. Open long if you expect the stock to rise, open short to profit from a decline. Choose leverage according to your risk plan.

Step 5: Execute and manage risk. Set strict stop-loss and take-profit orders before submitting the trade. PnL settles dynamically in USDT.

Risks and Core Considerations When Trading Semiconductor Stocks

Semiconductor stocks offer strong exposure to the AI infrastructure cycle, but they also carry meaningful risks tied to valuation, capex expectations, geopolitics, and volatility.

- Valuation compression risk: Many AI semiconductor stocks trade at premium forward multiples. If hyperscaler spending slows or earnings guidance weakens, these names can reprice sharply.

- Semiconductor cycle risk: Memory, foundry capacity, and equipment demand remain cyclical. Oversupply can emerge if companies expand too aggressively or cloud customers delay new orders.

- Geopolitical concentration risk: Leading-edge chip manufacturing is still heavily concentrated in Taiwan, while equipment supply is exposed to export controls and trade policy shifts. This can pressure names like TSM and ASML.

- Leverage and liquidation risk: Stock futures amplify both gains and losses. Traders should manage position size carefully and use stop-loss orders, especially around earnings and AI capex news.

- Tokenized stock limitations: Tokenized equities track stock price performance, but they may not provide voting rights, dividend entitlement, or physical share delivery.

Final Thoughts: Should You Add Semiconductor Stocks to Your 2026 Portfolio?

The 2026 semiconductor cycle is different from previous chip booms because demand is being driven by real AI infrastructure spending from hyperscalers with strong balance sheets. NVIDIA’s CUDA ecosystem, TSMC’s foundry and CoWoS leadership, ASML’s EUV lithography monopoly, and Broadcom’s custom AI ASIC pipeline each represent a different bottleneck in the AI hardware stack. For investors, diversifying across design, manufacturing, equipment, and IP can provide broader exposure to the AI chip cycle without relying too heavily on a single company’s execution.

However, the sector already trades at premium valuations and remains highly sensitive to hyperscaler capex plans, earnings guidance, and AI infrastructure spending trends. Long-term investors should focus on position sizing and diversification, while active traders using BingX TradFi should manage leverage carefully with stop-loss and take-profit controls. Whether through tokenized spot exposure or USDT-margined perpetuals, AI semiconductor stocks have become more accessible to global investors through crypto-native trading rails.

Related Reading

- Top AI Tokenized Stocks to Watch in 2026

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?