Memory and storage have become one of the most aggressively re-rated corners of the Artificial intelligence (AI) hardware supply chain in 2026. High-bandwidth memory is sold out through year-end, NAND contract prices rose roughly 60% in Q1 alone, and the small handful of companies positioned to supply the data center buildout have produced returns that would normally take a decade to deliver. Micron, SanDisk, Western Digital, Seagate, and the Roundhill Memory ETF each capture a different slice of this cycle, from HBM and NAND to enterprise SSDs, hard drives, and diversified global memory exposure. This guide walks through what changed, why it changed, and how to trade these names through BingX TradFi using USDT-margined stock futures.

The shift in 2026 is structural rather than cyclical. AI training and inference workloads consume memory bandwidth at rates that no previous workload class ever required, and the suppliers capable of producing HBM at scale are essentially price-makers for the first time in the industry's history. Memory is no longer the boom-and-bust commodity it was through 2022. For investors, that has changed the calculus on what these stocks are actually worth.

2026 AI Memory Market Overview: Why HBM, NAND, and DRAM Are Repricing

The memory market has shifted sharply in 2026 as AI infrastructure demand collides with limited supply. What was once treated as a highly cyclical, low-multiple sector is now being repriced around multi-year visibility, tighter capacity, and structurally stronger pricing power. Three forces explain the change.

1. HBM Has Become a Critical AI Bottleneck

HBM, or high-bandwidth memory, is a type of advanced DRAM stacked close to AI accelerators to deliver extremely fast data transfer. It is critical for AI chips because GPUs and ASICs need massive memory bandwidth to train and run large models efficiently.

High-bandwidth memory is now essential to every major AI accelerator shipped by NVIDIA, AMD, and Google. Only three suppliers can produce HBM at the scale and yield required: SK hynix, Samsung, and Micron. With the HBM market projected to grow from roughly $35 billion in 2025 to more than $100 billion by 2028, supply has become one of the most important bottlenecks in the AI hardware stack.

All three major suppliers have indicated that HBM capacity is already fully committed through the end of 2026. Micron’s early volume production of HBM4 in Q1 2026, with output tied to NVIDIA’s Vera Rubin platform, shows how closely next-generation memory supply is now linked to the AI accelerator cycle.

Read More: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

2. NAND Pricing Has Reset Higher

NAND flash is non-volatile memory used for storage, meaning it retains data even when power is off. It is the core technology behind SSDs, including the enterprise SSDs used in AI data centers for inference workloads.

NAND flash has moved into a tighter pricing environment as enterprise SSD demand rises for AI inference. Large-scale inference requires dense, high-performance storage, and the supplier base remains concentrated across Kioxia, Samsung, SK hynix, Micron, and SanDisk.

NAND contract prices rose sharply in Q1 2026, with further increases expected in Q2 as customers secure supply for AI data center deployments. If supply remains constrained through 2028 as some analysts expect, NAND could become a stronger earnings driver than in previous memory cycles.

3. Capital Discipline Is Extending the DRAM Cycle

DRAM is the main working memory used in servers, PCs, smartphones, and data centers. Unlike NAND, DRAM is volatile memory, meaning it temporarily stores data while systems are running but loses that data when power is turned off.

The biggest surprise in 2026 is supplier discipline. In past memory upcycles, producers often expanded aggressively and eventually created oversupply. This time, major DRAM suppliers have been more cautious, partly because HBM production consumes DRAM wafer capacity that would otherwise support commodity products.

That shift makes the cycle more self-rationing. As more capacity moves into high-margin HBM, less supply is available for standard DRAM products, helping support broader pricing. The fact that spot and contract DRAM prices have moved together in 2026 suggests buyers are accepting tighter supply conditions rather than waiting for a quick reversal.

What Are the Top AI Memory and Storage Stocks to Watch in 2026?

For U.S.-listed AI memory and storage exposure, five names stand out in 2026: Micron Technology, SanDisk, the Roundhill Memory ETF (DRAM), Western Digital, and Seagate Technology. Micron covers HBM, DRAM, and NAND; SanDisk offers pure NAND and enterprise SSD exposure; and DRAM provides diversified access to global memory leaders like SK hynix and Samsung. WDC and STXUS extend the theme into AI data storage infrastructure, including enterprise storage and high-capacity hard drives for cloud and AI data centers.

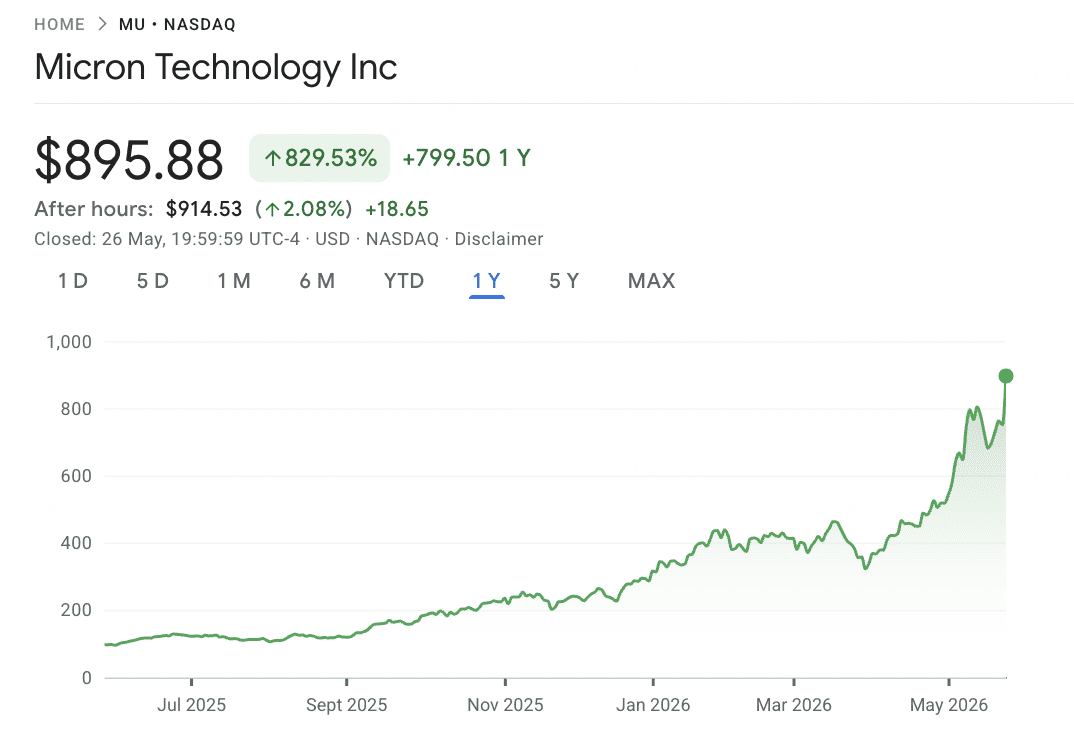

1. Micron Technology (MU)

Core Role: HBM, DRAM, and NAND manufacturer

Micron is the only U.S.-headquartered HBM supplier and one of the clearest beneficiaries of the 2026 memory repricing cycle. The company manufactures DRAM, NAND flash, and the high-bandwidth memory stacks required for advanced AI accelerators. As AI infrastructure demand accelerates, Micron’s HBM capacity has become increasingly strategic, with much of its 2026 production already committed.

The key technical milestone came in March 2026, when Micron began volume production of HBM4 36GB 12-high stacks designed for NVIDIA’s Vera Rubin platform. The product delivers 2.8 TB/s of bandwidth, roughly 2.3x higher than HBM3E, with 20% better power efficiency. Micron has also shipped samples of a larger 48GB 16-high configuration, strengthening its position in next-generation AI memory.

The financial results have followed the product cycle. Q2 FY2026 revenue reached $23.86 billion versus a $20.07 billion consensus, while adjusted EPS came in at $12.20 versus $9.31 expected. Full-year FY2026 consensus revenue estimates have been upgraded to roughly $109 billion, and sell-side price targets have moved sharply higher, including Mizuho at $800, Citi at $840, and Melius Research at $1,100. With shares trading near $698 in mid-May 2026, Micron has become one of the most important U.S.-listed AI memory stocks to watch.

Read More: Micron (MU) Stock Price Forecast 2026: Can AI Memory and DRAM Demand Push MU to $500?

MU Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$73.50 |

$33.70 |

0.3979 |

Pandemic-era DRAM demand surge, work-from-home capex |

|

2021 |

$94.15 |

$64.99 |

0.2421 |

Cyclical peak; supply constraints across consumer DRAM |

|

2022 |

$95.42 |

$48.06 |

−45.93% |

Memory glut, smartphone weakness, Fed rate-hike cycle |

|

2023 |

$86.46 |

$49.75 |

0.7193 |

AI narrative emerges; HBM3 ramp begins late year |

|

2024 |

$152.75 |

$79.06 |

−0.96% |

Volatile year; HBM3E qualified with NVIDIA, profit-taking offset gains |

|

2025 |

$109.24 |

$64.72 |

−18.14% |

Mid-cycle pullback before HBM4 ramp; consolidation phase |

|

2026 YTD |

$818.67 (5/14) |

$90.93 range |

+630% TTM |

HBM4 launch, sold-out 2026 capacity, full re-rating to AI infrastructure play |

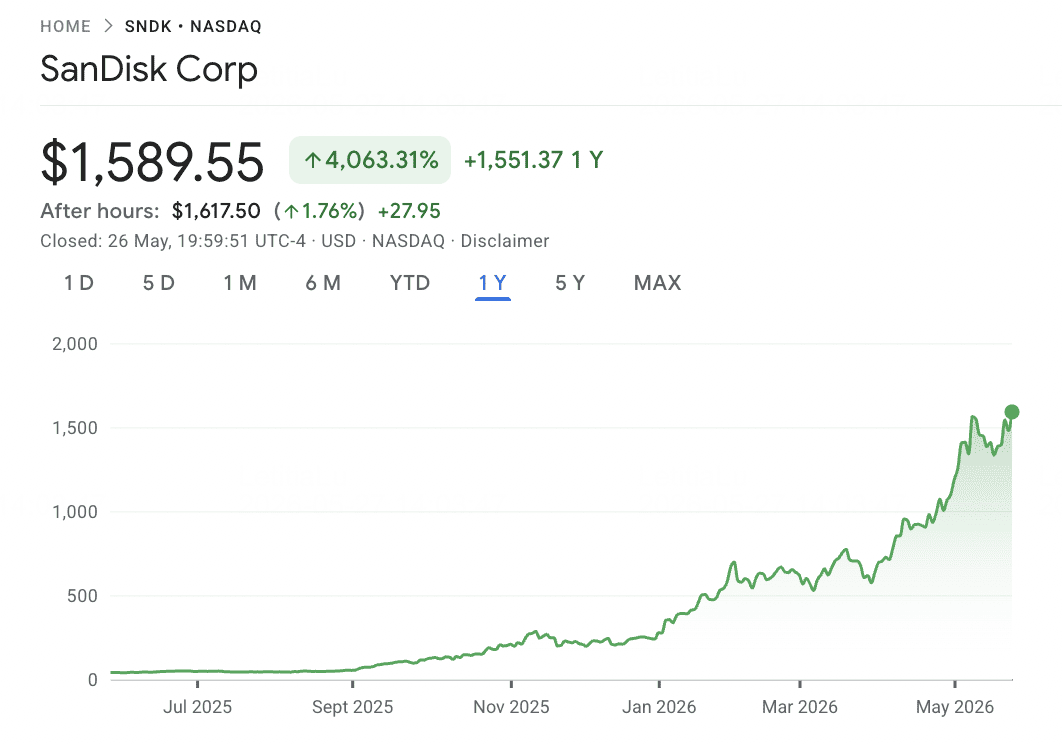

2. SanDisk (SNDK)

Core Role: Pure-play NAND flash and enterprise SSD specialist

SanDisk is one of the most aggressive semiconductor momentum stories in 2026. After completing its tax-free spinoff from Western Digital on February 24, 2025, the company relisted on Nasdaq as a standalone NAND flash business. As part of Western Digital, SanDisk’s NAND franchise was often blended with the slower hard disk business. As an independent company, its exposure is much clearer: enterprise SSD demand, BiCS8 3D NAND architecture, and wafer capacity from its Kioxia joint venture in Japan.

The post-spinoff rally has been extraordinary. SanDisk debuted near $32 in February 2025, traded above $626 by mid-February 2026, and moved past $1,096 in May 2026. That represents a trailing twelve-month return of roughly 3,314%, with more than 550% upside year to date in 2026. The main drivers are sharply higher NAND pricing, AI inference demand for enterprise SSDs, and tight Kioxia-linked supply. NAND contract prices rose about 60% in Q1 2026, with forecasts pointing to another 70% to 75% increase in Q2.

The risk is that SanDisk’s upside is highly tied to the NAND cycle. The company carries meaningful leverage, including a $2.0 billion term loan and a $1.2 billion payment commitment to Kioxia from 2026 to 2029. If NAND supply normalizes or AI-related SSD demand slows, margins could compress quickly because SanDisk’s revenue base is concentrated in one memory category.

Read More: SanDisk (SNDK) Price Prediction 2026: AI Memory Supercycle or $913 Technical Peak?

SNDK Price Trend (2025 Spinoff–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2025 |

~$95 |

$32.11 (Feb) |

+100% (partial) |

Spinoff from Western Digital; standalone NAND pure-play emerges |

|

2026 YTD |

$1,096+ (May) |

~$160 (Jan) |

+550% YTD |

NAND contract prices +60% Q1; AI SSD demand; best 2026 S&P 500 performer |

Note: SanDisk began trading as a standalone company only on February 24, 2025, so multi-year historical data prior to the spinoff is not directly comparable. The pre-spinoff Flash business was consolidated inside Western Digital.

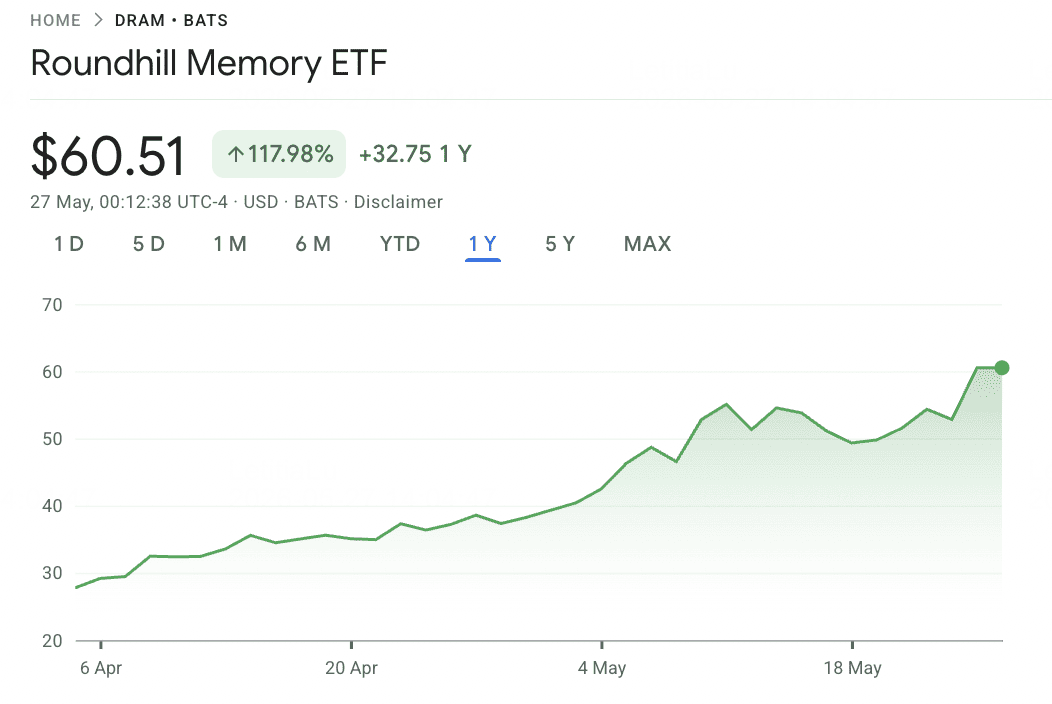

3. Roundhill Memory DRAM ETF (DRAM)

Core Role: First U.S.-listed pure-play memory chip ETF

Roundhill Memory DRAM ETF is the first U.S.-listed ETF focused entirely on memory chip manufacturers. Launched on April 2, 2026, the fund gives U.S. investors direct thematic exposure to the global memory cycle, including companies that are otherwise difficult to access through standard U.S. semiconductor ETFs. This matters because SK hynix and Samsung Electronics together produce a major share of global DRAM, but neither trades directly on U.S. exchanges or appears meaningfully in funds like SOXX or SMH.

The portfolio is highly concentrated. SK hynix accounts for roughly 28% of the fund, Samsung Electronics around 21%, and Micron Technology about 20% through direct shares and swap exposure. Kioxia Holdings adds another major memory exposure, while smaller positions include SanDisk, Western Digital, Seagate, Nanya, and Winbond. Because roughly 73% of assets sit in SK hynix, Samsung, and Micron, DRAM should be viewed as a focused memory-cycle bet rather than a broad semiconductor ETF.

Performance since launch has been extremely strong, with the ETF returning roughly 98% in its first seven weeks and about 63% over the past month. The key catalysts are Samsung’s HBM4 qualification progress with NVIDIA and SK hynix’s ability to maintain leadership in HBM3E and HBM4. The main risk is concentration: any major repricing in Samsung, SK hynix, or Micron can quickly move the entire fund, and U.S. trading-hour pricing partly depends on estimates for Korean-listed shares that are not actively trading during U.S. market hours.

Read More: Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

DRAM ETF Price Trend (2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2026 YTD |

~$50 (May) |

$25 (launch Apr 2) |

+98% since inception |

Pure-play memory ETF debut; AI memory supercycle drives all three core holdings |

Note: DRAM launched on April 2, 2026, so no multi-year historical data exists. The fund references underlying memory company performance through its DRAM, HBM, NAND, and SSD ecosystem holdings.

4. Western Digital (WDC)

Core Role: Data storage and enterprise storage infrastructure

Western Digital is no longer the same memory story it was before the SanDisk spinoff. After separating its NAND flash business, WDC is now more focused on hard drives and data storage infrastructure, making it a storage-adjacent AI infrastructure play rather than a pure memory stock.

Its relevance to AI comes from the explosive growth in data storage needs. AI training, inference logs, enterprise datasets, model checkpoints, and cloud workloads all require large-scale storage systems. While WDC does not offer the same direct HBM or NAND exposure as Micron or SanDisk, it can benefit from rising demand for high-capacity enterprise storage across AI data centers.

The main risk is that WDC remains more tied to the storage cycle than the AI accelerator cycle. It may benefit from data center demand, but it does not have the same pricing power as HBM suppliers or the same pure NAND exposure as SanDisk. For investors, WDC is best framed as an AI storage infrastructure name rather than a core AI memory supplier.

WDC Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$52.70 |

$21.69 |

−10.88% |

Pandemic volatility; storage demand mixed across segments |

|

2021 |

$58.09 |

$37.24 |

0.1773 |

Cyclical recovery; chip shortage tailwind |

|

2022 |

$50.90 |

$22.74 |

−51.62% |

HDD downcycle, NAND glut, Fed rate hikes |

|

2023 |

$39.84 |

$23.64 |

0.6599 |

AI narrative emerges; spinoff plans gain credibility |

|

2024 |

$60.40 |

$37.21 |

0.1386 |

Modest recovery; spinoff preparations underway |

|

2025 |

$187.20 |

$30.42 |

2.838 |

SanDisk spinoff Feb 2025; pure-play HDD re-rating, AI cold storage thesis |

|

2026 YTD |

$525.15 (52-wk) |

$187.68 (Jan) |

+157% YTD |

Q3 FY26 blowout: rev +45%, GM 50.5%; capacity sold out through 2026 |

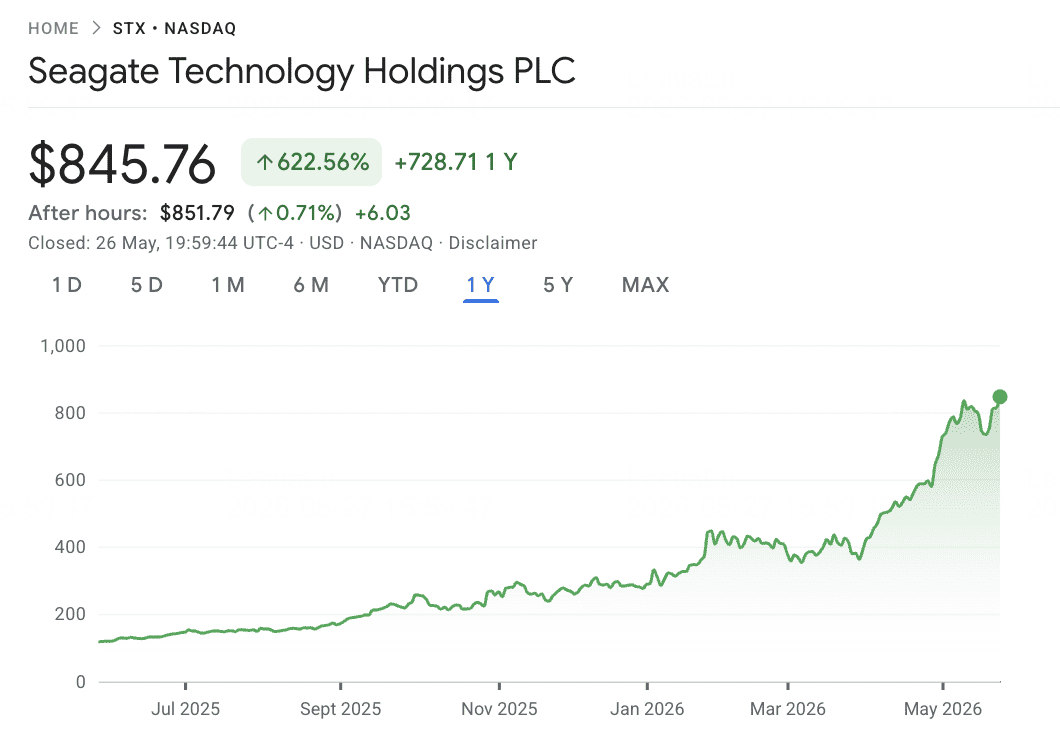

5. Seagate Technology (STX)

Core Role: Enterprise hard drives and mass data storage

Seagate is another AI storage beneficiary, focused primarily on high-capacity hard drives used in enterprise and cloud data centers. As AI workloads generate and process larger datasets, demand for cost-efficient mass storage continues to rise, especially for archival data, training datasets, model outputs, and hyperscale cloud infrastructure.

Unlike Micron, SanDisk, or the DRAM ETF, Seagate is not a pure semiconductor memory play. Its exposure is more closely tied to enterprise storage demand and hyperscaler infrastructure expansion. That makes STXUS a useful complement to memory names, especially for investors who want exposure to the storage side of the AI data center buildout.

The key risk is that hard drive demand remains cyclical and can be affected by cloud customer inventory cycles, pricing pressure, and shifts toward SSD-based storage in higher-performance applications. Seagate should therefore be positioned as an AI data storage play, not as a direct HBM or DRAM supplier.

STX Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$61.77 |

$36.40 |

0.1014 |

Modest pandemic year; enterprise storage demand stable |

|

2021 |

$111.71 |

$55.27 |

0.875 |

Cyclical peak; pandemic-era data center buildout |

|

2022 |

$112.70 |

$48.49 |

−51.42% |

HDD downcycle, hyperscaler digestion, Fed rate hikes |

|

2023 |

$86.79 |

$51.88 |

0.6917 |

AI narrative emerges; HAMR development on track |

|

2024 |

$112.64 |

$80.11 |

0.011 |

HAMR Mozaic platform begins commercial ramp |

|

2025 |

$151.94 |

$66.19 |

0.7506 |

AI storage demand builds; HAMR adoption accelerates |

|

2026 YTD |

$727.20 (5/1) |

~$200 (Jan) |

+184% YTD |

Q3 FY26 blowout: rev +44%, GM 47%; nearline sold out through 2027 |

2026 AI Memory Stocks Comparison by Market Exposure

AI memory and storage stocks sit across different parts of the AI infrastructure cycle, from HBM and DRAM manufacturing to NAND flash, enterprise SSDs, diversified memory ETFs, and high-capacity data storage. This comparison shows how each name benefits from AI accelerator demand, enterprise storage growth, and the broader repricing of memory supply.

|

Ticker |

Primary Exposure |

Core Advantage |

2026 Catalyst |

|

MU |

HBM, DRAM, NAND |

Only U.S.-headquartered HBM supplier; HBM4 in volume production |

HBM capacity committed; FY2026 revenue estimates raised sharply |

|

SNDK |

NAND flash, enterprise SSDs |

Pure-play NAND exposure after Western Digital spinoff |

NAND repricing and AI inference SSD demand |

|

DRAM ETF |

Global memory basket |

Exposure to SK hynix, Samsung, Micron, Kioxia, and other memory names |

Direct thematic exposure to HBM, DRAM, and NAND upcycle |

|

WDC |

Enterprise storage, HDD infrastructure |

AI storage infrastructure exposure after SanDisk spinoff |

Rising data center storage demand from AI workloads |

|

STXUS |

Enterprise HDD and mass storage |

High-capacity storage supplier for cloud and AI data centers |

Hyperscaler storage demand and AI data growth |

How to Trade AI Memory Stocks on BingX

BingX offers a crypto-native way to gain exposure to AI memory stocks and memory-focused ETFs without using a traditional brokerage account. Since dedicated AI memory tokenized stocks may not be available on the spot market, the main execution path is through USDT-margined perpetual contracts on BingX TradFi, which allow active traders to go long or short and trade around earnings, NAND pricing moves, HBM-related catalysts, and broader memory-cycle trends.

Long or Short AI Memory Stock Futures with USDT on BingX TradFi

For active traders looking to capitalize on short-term momentum, earnings volatility, NAND pricing moves, or HBM-related catalysts, BingX TradFi allows users to trade memory-linked stock futures with USDT. These USDT-settled perpetual contracts mirror the price movements of underlying equities and ETFs, offering flexible long and short exposure without requiring users to hold the physical stock.

Step 1: Account setup and security. Sign up and log into your BingX account, complete the identity verification (KYC) required in your region, and enable two-factor authentication.

Step 2: Allocate trading capital. Transfer USDT from your spot wallet into your futures account, where it will serve as collateral.

Step 3: Select your contract. Navigate to the TradFi markets page or the futures trading section. Choose memory-linked perpetual contracts such as MU-USDT, SNDK-USDT, DRAM-USDT, WDC-USDT, or STXUS-USDT.

Step 4: Set direction and leverage. Open long if you expect the stock or ETF price to rise, or open short if you expect a pullback. Choose leverage based on your risk plan.

Step 5: Execute and manage risk. Set stop-loss and take-profit orders before submitting the trade. PnL settles dynamically in USDT.

Risks and Core Considerations When Trading AI Memory Stocks

Memory stocks offer direct exposure to the AI infrastructure cycle, but they also carry meaningful risks tied to pricing cycles, fund concentration, market timing, and volatility.

- Memory cycle risk: Memory has historically been one of the most boom-and-bust segments of semiconductors. The current cycle is supported by stronger supplier discipline, but oversupply risk could return if major producers expand capacity too aggressively.

- DRAM ETF concentration risk: The Roundhill Memory DRAM ETF is heavily concentrated in SK hynix, Samsung, and Micron, with roughly 73% of net assets in these three names. It should be viewed as a focused memory-cycle bet rather than a broad semiconductor diversifier.

- Korean market hours mismatch: Because Samsung and SK hynix trade outside U.S. market hours, the DRAM ETF may rely partly on fair-value estimates during U.S. trading sessions. Tracking differences can widen around major news or earnings updates.

- NAND pricing risk for SanDisk: SanDisk is highly exposed to NAND contract prices and enterprise SSD demand. If supply normalizes or AI storage demand slows, margins could compress quickly because the business is concentrated in one memory category.

- Leverage and liquidation risk: Memory names have shown sharp intraday moves around earnings, pricing updates, and AI demand news. Traders using USDT-margined futures should manage position size carefully and use stop-loss orders.

- Storage cycle risk: Western Digital and Seagate are more exposed to enterprise storage and hard drive demand than pure HBM or DRAM pricing. Cloud customer inventory cycles, HDD pricing pressure, or a shift toward SSD-heavy deployments could affect performance.

Final Thoughts: Should You Add AI Memory Stocks to Your 2026 Portfolio?

The 2026 memory cycle is one of the clearest public-market expressions of the AI infrastructure buildout. HBM demand is tied directly to next-generation AI accelerators, NAND is being repriced by enterprise SSD demand for inference workloads, and DRAM supply remains tighter as capacity shifts toward higher-margin HBM. Micron offers direct exposure to HBM, DRAM, and NAND, SanDisk captures the NAND pricing cycle, the DRAM ETF provides broader access to global memory leaders, and Western Digital and Seagate extend the theme into AI data storage infrastructure.

The main risk is that memory has always been cyclical. The key question in 2026 is whether AI demand has structurally extended the cycle, or whether today’s pricing power eventually gives way to another supply-driven correction. For traders using BingX TradFi, conservative position sizing, leverage control, and stop-loss orders are essential when trading high-volatility memory names through USDT-margined perpetuals.

Related Reading

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Micron (MU) Stock Price Forecast 2026: Can AI Memory and DRAM Demand Push MU to $500?

- SanDisk (SNDK) Price Prediction 2026: AI Memory Supercycle or $913 Technical Peak?

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom