Artificial intelligence (AI) has moved from a software experiment to a physical infrastructure race. In 2026, the most important AI bottlenecks are model deployment, cloud demand, and the advanced manufacturing capacity required to produce leading-edge AI chips. NVIDIA and Broadcom may design the processors, but the physical production of next-generation AI silicon depends heavily on Taiwan Semiconductor Manufacturing Company (TSMC), ASML, and Intel’s attempt to re-enter advanced foundry manufacturing.

TSMC manufactures many of the advanced chips that power the AI economy, ASML supplies the extreme ultraviolet (EUV) and High-NA EUV lithography machines needed to print sub-3nm circuitry, and Intel represents the most important U.S.-based foundry challenger through its 18A and future 14A roadmap. Together, these companies define the manufacturing layer of the 2026 AI semiconductor cycle, from advanced nodes and CoWoS packaging to EUV equipment and supply chain reshoring.

AI Chip Manufacturing Market Overview in 2026: Why TSMC, ASML, and Intel Define the Cycle

The AI chip manufacturing layer is where the 2026 semiconductor cycle becomes most concentrated. Demand for advanced AI processors remains strong, but the real constraint is the limited capacity to manufacture, package, and scale them at leading-edge nodes. Three structural realities define this part of the supply chain: TSMC’s advanced-node and packaging leadership, ASML’s EUV monopoly, and Intel’s push to become a credible U.S.-based foundry alternative.

1. Advanced Node Capacity Is Limited by Capex and Build Time

Leading-edge AI chips from NVIDIA, AMD, Broadcom, Apple, and other major designers depend heavily on TSMC’s advanced process nodes, including 3nm and 5nm. TSMC’s 2nm node is now ramping, while its A16 process is being developed for future high-performance chips.

The key constraint is not demand, but physical capacity. Building an advanced-node fab can cost around $20 billion and take three to four years before reaching volume production. Even with strong customer orders, supply cannot expand quickly because fabs require massive capital investment, specialized equipment, engineering talent, and long qualification cycles.

2. Advanced Packaging Has Become a Core Competitive Advantage

As AI chips become more complex, performance increasingly depends on advanced packaging rather than node shrinks alone. Chiplet architectures, 2.5D stacking, and 3D integration now determine which AI accelerators can reach the market efficiently.

TSMC’s CoWoS packaging capacity has become one of the most important bottlenecks in the AI hardware stack. CoWoS allows compute, memory, and I/O components to be integrated on a single substrate, making it essential for high-performance AI accelerators. With hyperscalers competing for limited packaging capacity, TSMC’s leadership in CoWoS has become a major source of pricing power.

3. ASML’s EUV Monopoly Remains the Key Equipment Bottleneck

ASML remains the only company in the world capable of producing extreme ultraviolet lithography systems, the machines required to manufacture the most advanced chips. Low-NA EUV systems cost roughly €180 million each, while newer High-NA EUV systems can exceed €380 million.

This gives ASML one of the strongest structural positions in the semiconductor supply chain. Its High-NA platform is years ahead of any realistic alternative, and its 2026 backlog of roughly €38 billion provides strong multi-year revenue visibility. Export restrictions to China remain a risk, but demand from TSMC, Samsung, SK hynix, and Intel continues to support the long-term growth case.

Read More: Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

4. Intel Is the U.S. Foundry Challenger

Intel is not yet in the same structural position as TSMC or ASML, but it has become an important manufacturing name because of the U.S. reshoring theme. Its 18A node is central to the company’s foundry turnaround, while the future 14A roadmap is positioned for external AI and custom-chip customers.

The bull case is that Intel becomes the most credible U.S.-based alternative to TSMC for advanced manufacturing. CHIPS Act support, defense-related demand, and supply chain diversification all strengthen the strategic case. The risk is execution: Intel still needs to prove that its foundry roadmap can attract external customers at scale.

What Are the Best AI Chip Manufacturing Stocks to Buy in 2026?

Three names define the AI chip manufacturing layer in 2026. TSMC is the leading foundry that physically manufactures many of today’s advanced AI processors, ASML supplies the EUV lithography machines required for leading-edge production, and Intel is the most important U.S.-based foundry challenger. Together, these stocks cover the key manufacturing bottlenecks behind the AI semiconductor cycle: wafer fabrication, advanced packaging, EUV equipment, and supply chain reshoring.

1. Taiwan Semiconductor Manufacturing (TSM)

Core Role: Global leading-edge foundry and advanced packaging leader

TSMC is the physical manufacturing center of the AI hardware economy. The company produces chips for NVIDIA, AMD, Apple, Broadcom, Qualcomm, MediaTek, and much of the fabless semiconductor industry. Its leadership in advanced process nodes gives it a near-irreplaceable position in AI chip production, with 3nm already in volume production, 2nm ramping, and the A16 node under development.

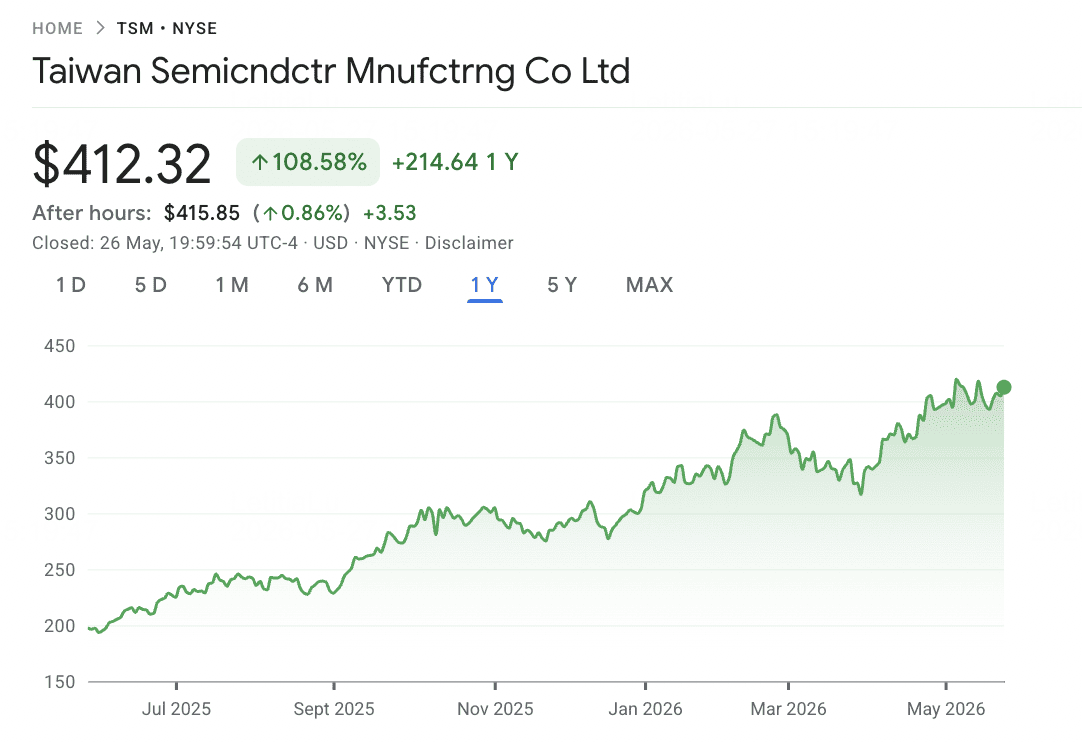

AI demand has reshaped TSMC’s revenue mix and growth outlook. For the first time in company history, high-performance computing has overtaken smartphones as its largest revenue segment, accounting for 61% of revenue versus 26% from mobile. In 2026, TSMC raised full-year revenue growth guidance to above 30% in U.S. dollar terms, while Q1 revenue reached $35.9 billion, reflecting strong demand from AI accelerators, data center chips, and advanced packaging.

The company is also investing aggressively to protect its manufacturing lead, spending near the upper end of its $52 billion to $56 billion capex range and approving a $20 billion capital injection into its U.S. subsidiary to accelerate the Arizona buildout. The stock is up roughly 31% year to date in 2026, with a market cap near $1.9 trillion and analyst price targets clustered between $423 and $490.

Read More: TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

TSM Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$100.92 |

$39.94 |

0.9271 |

Pandemic-era chip demand surge; 5nm volume ramp begins |

|

2021 |

$129.62 |

$100.52 |

0.1208 |

Global chip shortage; capacity tight across all nodes |

|

2022 |

$132.24 |

$57.57 |

−36.75% |

Buffett's Berkshire exits; Fed rate hikes, geopolitical tension |

|

2023 |

$103.67 |

$71.10 |

0.4233 |

AI narrative emerges; 3nm node ramps with Apple as lead customer |

|

2024 |

$205.89 |

$97.06 |

0.9258 |

NVIDIA Blackwell ramp; CoWoS demand becomes the bottleneck |

|

2025 |

$245.60 |

$140.92 |

0.2321 |

Tariff uncertainty, but AI demand offsets weakness |

|

2026 YTD |

$421.97 (5/14) |

$188.81 range |

+31.22% YTD |

Revenue guidance raised above 30%; $20B Arizona capital injection |

2. ASML Holding (ASML)

Core Role: Sole global supplier of EUV and High-NA EUV lithography

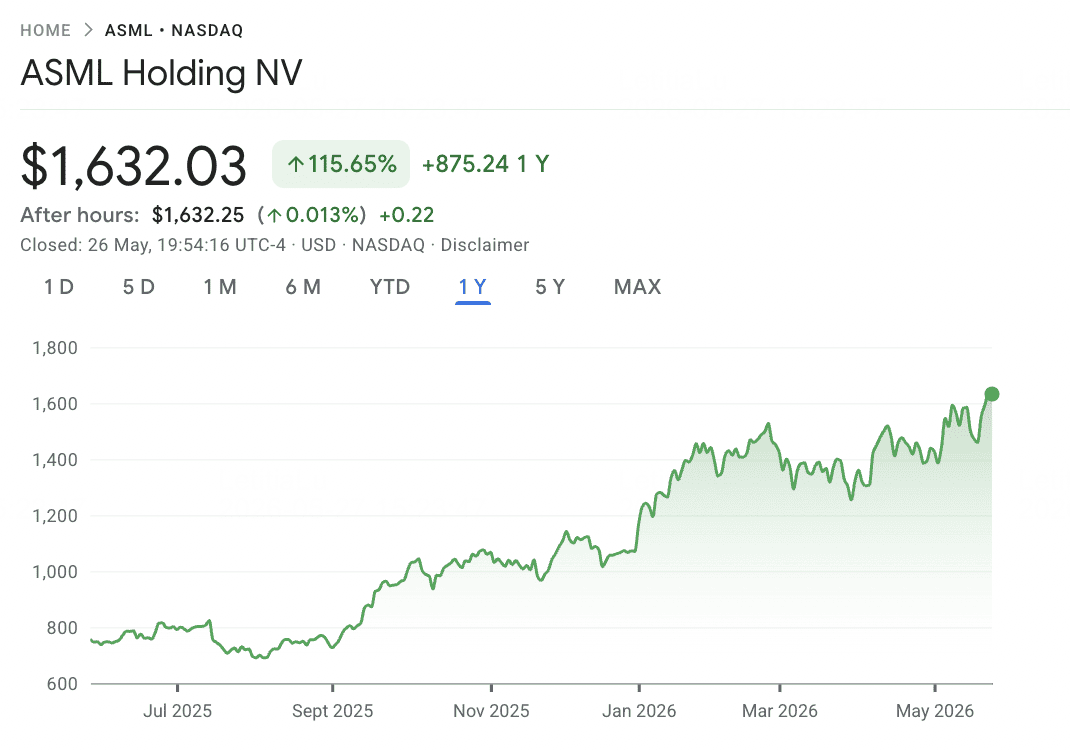

ASML is one of the most strategically important suppliers in the global chip industry. The company manufactures extreme ultraviolet lithography systems, the only tools capable of printing the circuitry required for sub-3nm process nodes. Every leading-edge AI chip, advanced memory product, and high-performance processor ultimately depends on ASML equipment. Low-NA EUV systems sell for roughly €180 million each, while High-NA EUV systems sell for about €380 million, with only limited annual production capacity.

The 2026 financials reflect this pricing power. Q1 revenue reached €8.8 billion at a 53% gross margin, and management raised full-year revenue guidance to €36 billion to €40 billion. ASML also ended 2025 with a €38.8 billion backlog, including €7.4 billion in EUV bookings, giving the company strong multi-year revenue visibility. Longer term, management expects revenue of €44 billion to €60 billion by 2030, with gross margins reaching 56% to 60% as High-NA adoption and recurring services revenue expand.

The main risk is geopolitical. ASML has become deeply exposed to U.S.-China technology restrictions, which prevent EUV sales to China and may limit service access for certain installed systems. These export controls have pressured investor sentiment, but demand from TSMC, Samsung, SK hynix, Intel, and other non-China customers remains strong enough to support the long-term thesis.

Read More: ASML Holding (ASML) Stock Price Forecast 2026: AI Infrastructure King or Geopolitical Target?

ASML Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$469.25 |

$187.01 |

0.6628 |

Pandemic-era chip demand; EUV system shipments accelerate |

|

2021 |

$854.29 |

$469.55 |

0.6414 |

Global chip shortage; record orders, capacity sold out |

|

2022 |

$768.06 |

$368.53 |

−30.52% |

Memory downturn; Fed rate cycle; first U.S. export restrictions |

|

2023 |

$752.30 |

$535.81 |

0.399 |

AI rebound; High-NA EUV milestones; logic customer orders |

|

2024 |

$1,086.22 |

$653.52 |

−7.70% |

Volatility on China export restrictions; July all-time high then pullback |

|

2025 |

$820.94 |

$592.18 |

0.0789 |

Backlog stabilization; Q4 bookings of €13.2B set record |

|

2026 YTD |

$1,344.40 |

$587.80 range |

+95.77% TTM |

2026 guidance raised to €36–40B; UBS €1,900 target |

3. Intel (INTC)

Core Role: U.S.-based foundry challenger and integrated chip manufacturer

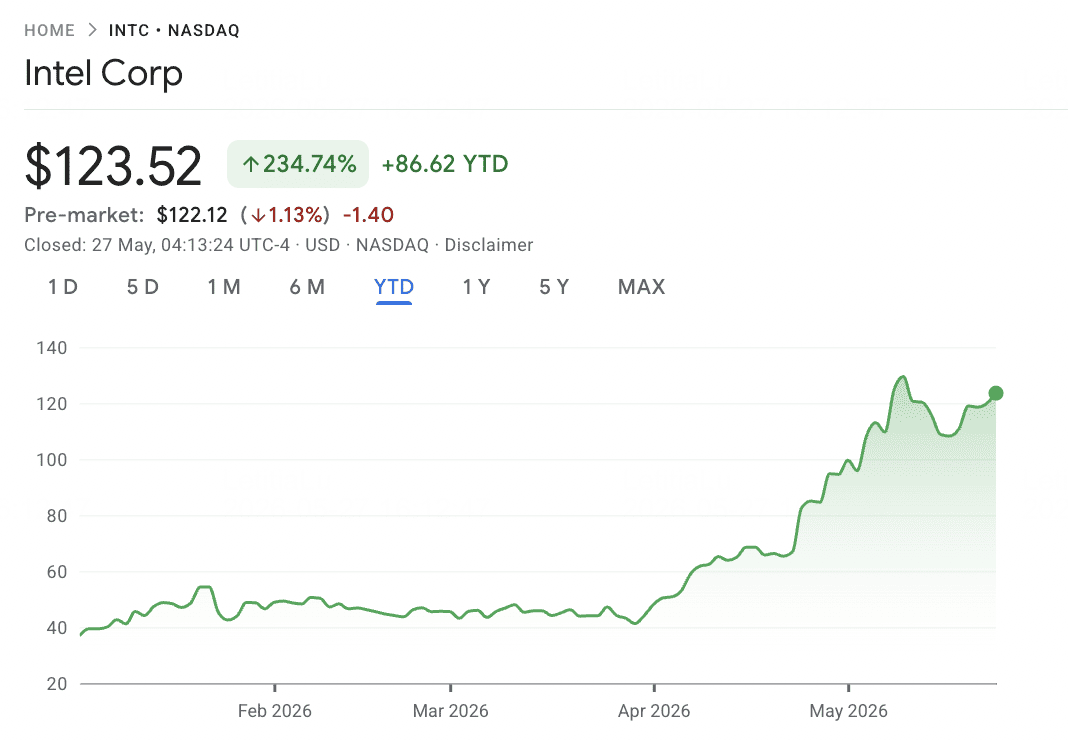

Intel is the most important turnaround story in the AI chip manufacturing layer. Unlike fabless chip designers, Intel owns manufacturing capacity and is trying to rebuild credibility as an advanced foundry through its 18A and future 14A process roadmap. This makes Intel relevant not only as a chip company, but also as a U.S.-based alternative to TSMC in a market increasingly shaped by supply chain security and reshoring.

The strategic case is tied to execution and policy support. Intel benefits from CHIPS Act funding, defense-related demand, and growing interest from customers looking to diversify advanced manufacturing outside Taiwan. If Intel can prove its foundry roadmap works for external AI and custom-chip customers, the upside could be significant.

The risk is that Intel is still a turnaround, not a proven bottleneck like TSMC or ASML. Manufacturing delays, weak external customer adoption, margin pressure, or continued competition from TSMC could limit the thesis. For investors, Intel should be viewed as the higher-risk, higher-upside manufacturing bet within the AI chip supply chain.

Read More: Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

INTC Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$60.40 |

$39.54 |

−14.70% |

Pandemic year; manufacturing delays widen gap vs AMD |

|

2021 |

$62.07 |

$44.09 |

0.0602 |

Pat Gelsinger named CEO; IDM 2.0 foundry strategy announced |

|

2022 |

$51.83 |

$23.82 |

−46.65% |

Process node delays; market share losses accelerate |

|

2023 |

$50.08 |

$24.30 |

0.9464 |

AI narrative emerges; recovery rally, then fades |

|

2024 |

$48.89 |

$18.89 |

−59.56% |

Worst year on record; Gelsinger ousted; massive layoffs |

|

2025 |

$27.39 |

$18.13 |

0.01 |

Lip-Bu Tan named CEO; 52-week low $18.96 (Aug); stabilization phase |

|

2026 YTD |

$132.75 (52-wk) |

~$20 (Jan) |

+194.77% YTD |

18A node in HVM; Q1 blowout April 23 (+25% gap up); TTM return +404.73% |

2026 AI Chip Manufacturing Stocks Comparison by Supply Chain Role

AI chip manufacturing stocks sit in the most supply-constrained part of the semiconductor value chain. This comparison highlights how TSMC, ASML, and Intel each capture a different part of the manufacturing thesis: TSMC through advanced-node foundry and CoWoS packaging leadership, ASML through EUV and High-NA EUV lithography scarcity, and Intel through its U.S.-based foundry turnaround and reshoring opportunity.

|

Ticker |

Primary Role |

Core Advantage |

2026 Catalyst |

|

TSM |

Advanced foundry and packaging |

Leading-edge 3nm/2nm manufacturing and CoWoS packaging leadership |

30%+ revenue growth guidance; $20B Arizona capital injection |

|

ASML |

EUV and High-NA EUV lithography equipment |

Sole global supplier of EUV systems required for advanced-node chip production |

2026 revenue guidance raised to €36–40B; High-NA EUV ramp |

|

INTC |

U.S. foundry challenger |

18A and future 14A roadmap with CHIPS Act and reshoring support |

Foundry turnaround, external customer ramp, and U.S. supply chain diversification |

How to Trade AI Chip Manufacturing Stocks on BingX

BingX offers a crypto-native way to trade leading AI chip manufacturing stocks without using a traditional brokerage account. Since dedicated tokenized spot products for TSMC and ASML may not be available, the main execution path is through USDT-margined perpetual contracts on BingX TradFi, which allow active traders to go long or short and trade around earnings, guidance updates, export-control news, and AI capex cycles.

Trade AI Chip Manufacturing Stock Futures with USDT on BingX TradFi

For active traders looking to capture short-term momentum or hedge exposure to the AI manufacturing cycle, BingX TradFi allows users to trade TSMC and ASML stock futures with USDT. These USDT-settled perpetual contracts mirror the price movements of the underlying equities, offering flexible long and short exposure without requiring users to hold the physical stock.

Step 1: Account setup and security. Sign up and log into your BingX account, complete the identity verification (KYC) required in your region, and enable two-factor authentication.

Step 2: Allocate trading capital. Transfer USDT from your spot wallet into your futures account, where it will serve as collateral.

Step 3: Select your contract. Navigate to the TradFi markets page or the futures trading section. Choose TSMU-USDT, ASML-USDT or or INTC-USDT, the three key manufacturing-layer stock perpetuals.

Step 4: Set direction and leverage. Open long if you expect the stock price to rise, or open short if you expect a pullback. Choose leverage based on your risk plan.

Step 5: Execute and manage risk. Set stop-loss and take-profit orders before submitting the trade. PnL settles dynamically in USDT.

Risks and Core Considerations When Trading AI Chip Manufacturing Stocks

AI chip manufacturing stocks offer exposure to some of the strongest bottlenecks in the semiconductor supply chain, but they also carry risks tied to geopolitics, capex intensity, valuation, and headline-driven volatility.

- Taiwan geopolitical risk: TSMC’s leading-edge manufacturing capacity remains heavily concentrated in Taiwan despite its Arizona expansion. Any escalation in cross-strait tensions or U.S.-China trade conflict can trigger sharp drawdowns in TSM.

- ASML export restriction risk: ASML is exposed to expanding U.S. and Dutch export controls on semiconductor equipment sales and servicing to China. New restrictions can pressure revenue expectations and cause sudden stock declines.

- Capital intensity and margin pressure: Both TSMC and ASML operate in highly capital-intensive parts of the supply chain. TSMC’s Arizona fab buildout may also create margin dilution as overseas manufacturing costs remain higher than Taiwan-based production.

- Premium valuation risk: Both names trade at elevated multiples relative to historical averages because investors are pricing in continued AI capex growth. Any slowdown in hyperscaler spending or weaker guidance could compress valuations quickly.

- Leverage and liquidation risk: Manufacturing stocks can move sharply on policy announcements, export-control headlines, earnings updates, or AI capex news. Traders using USDT-margined futures should manage position size carefully and use stop-loss orders.

- Intel execution risk: Unlike TSMC and ASML, Intel is still proving its advanced foundry turnaround. Delays in 18A or 14A, weak external customer adoption, or margin pressure from aggressive fab investment could weigh on the stock.

Final Thoughts: Should You Add AI Manufacturing Stocks to Your 2026 Portfolio?

TSMC, ASML, and Intel offer three different ways to gain exposure to the 2026 AI chip manufacturing cycle. TSMC controls the most important advanced foundry and packaging capacity, ASML remains the only supplier of EUV and High-NA EUV lithography systems, and Intel adds a U.S.-based foundry turnaround and reshoring angle. Together, they cover the most important manufacturing bottlenecks behind advanced AI chip production.

The trade-off is that each stock carries a different risk profile. TSMC faces Taiwan geopolitical risk, ASML faces export-control risk, and Intel faces execution risk as it works to rebuild foundry credibility. For traders using BingX TradFi, conservative position sizing, leverage control, and stop-loss orders are essential when trading TSMU-USDT, ASML-USDT, or INTC-USDT through USDT-margined perpetual contracts.

Related Reading

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

- ASML Holding (ASML) Stock Price Forecast 2026: AI Infrastructure King or Geopolitical Target?

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom