In April 2026, SLB (NYSE: SLB) finds itself at a critical strategic crossroads. While the company has long been the gold standard for traditional oilfield services, its Q1 2026 earnings reveal a business undergoing a profound transformation. Year-to-date, SLB has battled significant headwinds from operational shutdowns in Qatar and Iraq, yet its Digital and AI-driven segments are growing at a double-digit clip. With management reiterating a $1 billion run-rate exit for its data center business by the end of the year, SLB is no longer just a drill bit play but is also becoming a cornerstone of energy-tech infrastructure.

However, the investment thesis is currently bifurcated. Bulls highlight the massive 145% increase in automated footage drilled and the Strong Buy consensus from 45% of analysts. Conversely, bears point to a 346-basis-point drop in adjusted EBITDA margins and a slightly negative free cash flow of $23 million in Q1. This guide analyzes the SLB stock price prediction for 2026 using data from GuruFocus, Seeking Alpha, MarketBeat, and Simply Wall St.

You can also explore how to trade SLB stock futures with USDT on BingX TradFi.

Top 5 Things for SLB Investors to Know in 2026

- The NVIDIA AI Factory Partnership: SLB has been selected as the modular design partner for NVIDIA DSX AI factories, positioning the company to benefit directly from the global AI infrastructure build-out.

- $1 Billion Data Center Goal: Management remains on track to exit 2026 with a $1 billion run rate for its Data Center Solutions business, a segment that grew 45% year-on-year in Q1.

- Middle East Sensitivity: Conflict in the Middle East remains the primary risk, with operational disruptions in Qatar and Iraq causing a $200 million revenue miss in the first quarter alone.

- ChampionX Synergies: The 23% revenue growth in Production Systems was driven by the successful integration of ChampionX, which continues to provide accretive growth and cross-selling opportunities.

- Aggressive Capital Returns: Despite Q1 challenges, SLB repurchased $451 million in stock during the quarter and is committed to a minimum of $2.4 billion in buybacks for the full year 2026.

What Is SLB (Schlumberger)?

SLB is a global technology company that drives energy innovation. Traditionally known as the world's largest oilfield services provider, SLB provides the hardware, software, and data analytics required to locate, drill, and manage hydrocarbon reservoirs.

In 2026, the company has successfully rebranded its focus into four key pillars: Digital & Integration, Reservoir Performance, Well Construction, and Production Systems. By acquiring ChampionX and partnering with tech giants like NVIDIA and S&P Global, SLB is pivoting toward Asset-Light revenue streams. This shift aims to insulate the company from the extreme volatility of WTI crude prices by increasing its Annual Recurring Revenue (ARR) through petrotechnical software and autonomous drilling solutions.

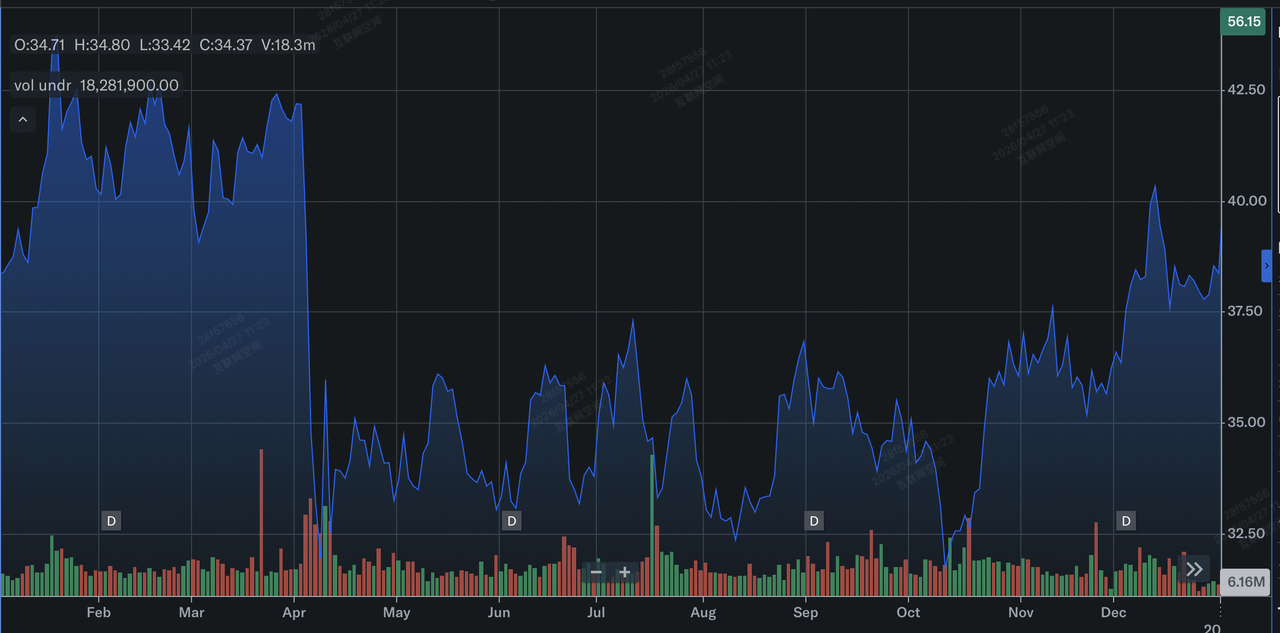

SLB Stock Performance in 2025: A Review

SLB stock's performance in 2025 | Source: Yahoo Finance

2025 was defined by a late-year surge that rescued an otherwise sluggish performance, with SLB delivering a 3.28% total return for the year. While full-year revenue dipped 2% to $35.71 billion and GAAP EPS fell 24% to $2.35 due to persistent Middle East instability, the fourth quarter marked a massive operational pivot. Q4 revenue hit $9.75 billion, a 9% sequential jump driven by the ChampionX acquisition, which injected $1.46 billion in high-margin production revenue. This year-end momentum was underscored by a robust $2.29 billion in Q4 free cash flow, providing the liquidity for the board to hike dividends by 3.5% and signal a massive $4 billion shareholder return target for 2026.

Strategically, SLB successfully transitioned from a volume-based driller to a high-value digital partner in 2025. The company’s Digital Revenue acted as a critical stabilizer, growing between 3% and 11% quarterly as the Agentic Web and AI-driven autonomous workflows began managing complex on-chain energy data. By reaching a $3 billion digital revenue milestone by year-end, SLB effectively offset the decline in North American land drilling. This shift toward Asset-Light recurring revenue streams, paired with a dominant position in international offshore markets, allowed SLB to enter 2026 with a consensus Buy rating and a fortified balance sheet capable of weathering the geopolitical shocks that emerged in the new year.

Key Strategic Priorities for SLB in 2026

|

Objective |

2026 Target / Status |

|

Data Center Run Rate |

$1 Billion exit rate (reconfirmed Q1 2026) |

|

Shareholder Returns |

>$4 Billion via dividends and buybacks |

|

Digital EBITDA Margin |

35% target for the full year |

|

S&P Global Deal Close |

Expected H2 2026 or early 2027 |

SLB 2026 Strategic Targets at a Glance

- Industrializing AI with NVIDIA: Moving beyond cooling to serve as the modular design partner for NVIDIA DSX AI factories. Management is specifically targeting an AI Factory for Energy, a reference environment that combines generative and industrial-scale agentic AI to help operators process massive subsurface datasets.

- Autonomous Drilling at Scale: Doubling down on autonomous solutions as automated footage drilled surged 145% year-on-year in Q1. This remains the core mechanical lever to protect margins in the Well Construction division amidst rising global labor costs.

- Targeted Subsurface Digital Expansion: Finalizing the acquisition of S&P Global’s upstream petrotechnical software suite - Kingdom, Petra, Harmony. This move specifically aims to capture the U.S. onshore unconventional market and integrate these technical workflows into SLB’s cloud-based AI platforms.

- Production Systems & ChampionX Synergies: Accelerating the integration of ChampionX to drive the Production Systems segment, which grew 23% year-on-year. The priority is capturing capital-efficient barrels by combining artificial lift and production chemistry with digital performance monitoring.

- Geographic Pivot & Energy Security: Offsetting Middle East disruptions by capturing a strengthening $100 billion FID (Final Investment Decision) pipeline. The strategic focus has shifted toward offshore and deepwater markets in Africa, Asia, and Latin America, where energy security concerns are driving long-cycle infrastructure investment.

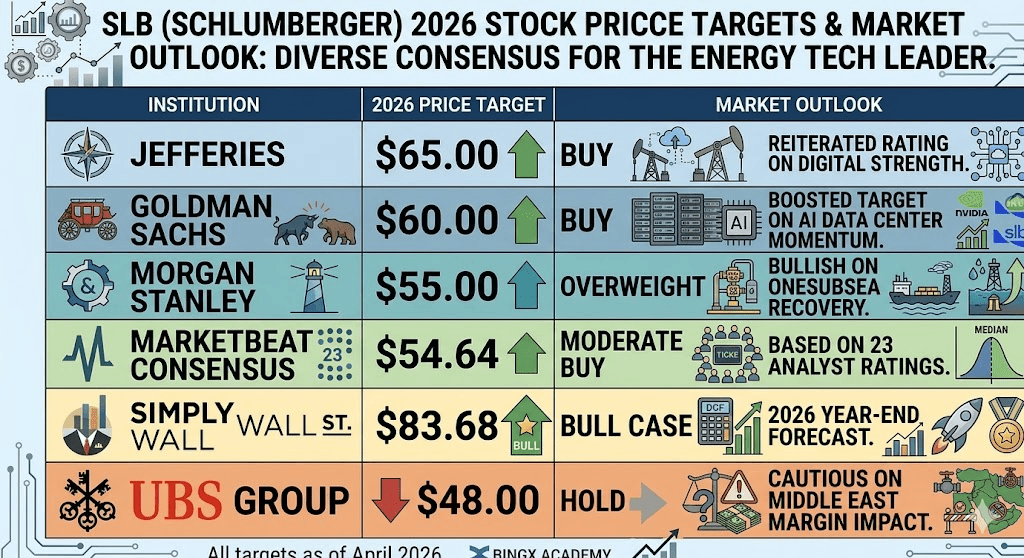

SLB Stock Forecast 2026: $83 Alpha vs. $48 Mean Reversion

SLB stock predictions for 2026 by various Wall Street analysts

The 2026 outlook for SLB is a high-stakes tug-of-war between its traditional role as a geopolitical proxy and its emerging identity as a premier energy-tech infrastructure provider.

The Bull Case: The $83.68 Digital Tech Re-Rating

The bullish narrative centers on a fundamental valuation shift, where SLB successfully decouples from commodity cycles to trade as a high-margin technology firm. This scenario is anchored by the company hitting its $1 billion run-rate exit for Data Center Solutions and achieving a 35% EBITDA margin for its Digital division. If the partnership with NVIDIA for DSX AI factories scales as projected and the 145% growth in automated footage drilled continues to slash operational overhead, SLB could transition from a cyclical service provider to an essential AI-for-Energy platform.

Data-driven bulls point to a Peace Dividend in H2 2026 as the primary catalyst. Under this scenario, the resumption of stalled projects in Qatar and Iraq would allow SLB to book deferred revenue while simultaneously capturing the $100 billion FID pipeline in offshore and deepwater markets. With a high-end price target of $83.68, as projected by Simply Wall St and supported by Argus Research, the stock would benefit from a significant multiple expansion, reflecting its new status as a leader in the tokenization of energy workflows and industrial AI.

The Base Case: $55–$60 Fair Value Consolidation

The base case assumes a muddle-through geopolitical environment where Middle East disruptions persist but are strategically offset by mid-to-high single-digit revenue growth in the Americas and Africa. In this scenario, the stock anchors near the Wall Street consensus target of $55.26. The 23% growth in Production Systems seen in Q1, fueled by the ChampionX integration, becomes the primary engine for steady earnings. By balancing $510 million in quarterly capital investments against a massive $2.4 billion annual stock repurchase program, SLB creates a robust valuation floor for investors.

Practically, this scenario relies on SLB’s ability to activate inflation pass-through clauses to neutralize rising logistics and transportation costs. While adjusted EBITDA margins might face temporary pressure, the 2.1% dividend yield and the company’s excellent insulation from commodity swings, evidenced by a low 6.4 FCF-to-WTI volatility ratio, position the stock as a defensive tech-energy hybrid. Investors can expect a disciplined buy the dip range as the market waits for the S&P Global software suite integration to fully materialize in the balance sheet.

The Bear Case: $48.84 Geopolitical Mean Reversion

The bear case is defined by a contagion of disruption across the Middle East, leading to prolonged operational shutdowns in key markets like Iraq and Qatar. Under this scenario, SLB’s high capital intensity becomes a liability, as revenue falls faster than the cost base can be adjusted. Analysts at Goldman Sachs warn that persistent conflict could trigger $0.06 to $0.08 in incremental EPS erosion per quarter. If the year-on-year adjusted EBITDA margin, which already dropped 346 basis points in Q1, fails to normalize, the stock risks a sharp rotation back toward its $48.84 support level.

From a risk management perspective, the bear case highlights the danger of high decrementals, where the loss of top-tier, high-margin international revenue cannot be offset by lower-margin North American land drilling. If free cash flow remains slightly negative or suppressed by seasonal working capital increases, the ambitious $4 billion shareholder return target could be scaled back. For BingX traders, this scenario would be characterized by a break below the 200-day moving average, as the Tariff Headwinds and OPEC+ production hikes cited by bears take center stage over the AI narrative.

SLB Investment Outlook and Stock Forecast 2026 by Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Jefferies |

$65.00 |

Buy: Reiterated rating on digital strength. |

|

Goldman Sachs |

$60.00 |

Buy: Boosted target on AI data center momentum. |

|

Morgan Stanley |

$55.00 |

Overweight: Bullish on OneSubsea recovery. |

|

MarketBeat Consensus |

$54.64 |

Moderate Buy: Based on 23 analyst ratings. |

|

Simply Wall St |

$83.68 |

Bull Case: 2026 year-end forecast. |

|

UBS Group |

$48.00 |

Hold: Cautious on Middle East margin impact. |

How to Trade SLB Stock Futures on BingX TradFi

Navigate the volatility of SLB using BingX TradFi tools and the power of BingX AI insights. Whether you are hedging against Middle East instability or betting on the NVIDIA AI partnership, BingX offers high-performance trading for the modern analyst.

SLB/USDT perpetual contract on BingX futures market

Long or Short SLB Stock Futures on BingX

- Access TradFi: Visit the BingX TradFi section and select Stock Futures.

- Find SLB: Search for the SLB/USDT perpetual contract.

- Leverage: Apply 2x–10x leverage depending on your risk appetite.

- Set Protection: Set Stop-Loss levels to protect your position from sudden geopolitical headlines or OPEC+ policy shifts.

Final Thoughts: Is SLB Stock a Good Buy in 2026?

SLB enters the second half of 2026 as a high-upside play on the Agentic Web and energy transition. While the Q1 reset was painful, the underlying 9% growth in Digital Operations and 45% growth in Data Center Solutions suggests the company's long-term strategy is intact.

For the professional analyst, SLB offers a unique Alpha opportunity: it provides exposure to AI infrastructure at a fraction of the P/E multiple of pure-play tech stocks. If you believe in the $1 billion data center run rate and the resilience of offshore deepwater investments, SLB at sub-$60 levels represents a compelling entry point. However, keep a close eye on WTI crude volatility and Middle East security conditions; until the geopolitical trap is cleared, the stock remains a high-beta asset requiring active risk management.

Risk Reminder: Trading and investing in SLB involves substantial risk. The stock is highly sensitive to geopolitical developments and global energy demand. Perform independent due diligence before allocating capital to high-volatility energy-tech assets.

Related Reading

- Occidental Petroleum (OXY) Price Prediction 2026: $115 Net-Zero Alpha or $55 Commodity Trap?

- XOP S&P Oil & Gas ETF Prediction 2026: $210 Geopolitical Moonshot or $130 Hedge Trap?

- Energy Select Sector XLE ETF Prediction 2026: $65 Energy Supercycle or $40 Hormuz Hedge Exit?

- Exxon Mobil (XOM) Price Prediction 2026: $180 Energy Alpha or Geopolitical Value Trap?

- Cheniere Energy (LNG) Price Prediction 2026: $330 Sovereign Boom or $210 Infrastructure Trap?

- Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?