Artificial intelligence (AI) has moved from a software story to a data center buildout. In 2026, hyperscaler capital expenditure is increasingly flowing into the physical infrastructure needed to support AI workloads, including cloud capacity, AI servers, power systems, cooling, networking, and data center operations. As demand for AI compute continues to exceed available capacity, the companies that build, operate, and supply data center infrastructure have become some of the most direct public-market plays on the AI infrastructure cycle.

This guide focuses on the key stocks behind the AI data center theme, including cloud and hyperscale platforms, data center operators, AI server vendors, power and cooling infrastructure providers, and networking equipment companies. Instead of focusing on chip designers, the article looks at the businesses supporting the physical expansion of artificial intelligence (AI) capacity and explains how global investors can trade selected names on BingX TradFi through USDT-margined perpetual contracts.

AI Data Center Market Overview in 2026: Why Capacity Defines the Cycle

The 2026 artificial intelligence (AI) data center cycle is defined less by weak demand than by the difficulty of bringing enough capacity online. Cloud providers, server vendors, power infrastructure companies, networking suppliers, and data center operators are all being pulled into the same buildout. Four structural realities explain where value is flowing across the AI data center stack.

1. Hyperscaler Capex Has Reached Industrial Scale

AI infrastructure spending has entered a new phase. Amazon, Microsoft, Alphabet, and Meta are expected to spend hundreds of billions of dollars on capital expenditure in 2026, with a large share directed toward AI data centers, servers, networking, power systems, and cooling infrastructure. This matters because hyperscaler capex is no longer just a cloud software story. It is now an industrial-scale buildout that benefits companies across the physical data center ecosystem.

2. Cloud Backlogs Are Larger Than Available Capacity

Demand for AI cloud services continues to exceed available infrastructure. Microsoft, Google Cloud, and Oracle have all reported large cloud or infrastructure backlogs, showing that customers are committing to future AI capacity before it is fully available. This shifts the market’s focus from near-term cloud margins to capacity visibility. For AI data center stocks, the key question is how quickly companies can turn contracted demand into operational compute capacity.

3. Power, Cooling, and Land Have Become the Binding Constraints

AI data centers require massive electricity, advanced cooling, grid access, and physical land. In many regions, power availability and interconnection timelines are now slowing expansion more than capital availability. This creates opportunities for power equipment providers, cooling specialists, grid contractors, and data center operators with secured land and power access. In 2026, capacity rights and energy access have become strategic advantages.

4. AI Servers and Data Center Infrastructure Are Becoming More Specialized

AI workloads require more specialized infrastructure than traditional cloud computing. High-density server racks, advanced cooling, faster networking, and optimized facility layouts are becoming essential for training, inference, and enterprise AI applications. This benefits companies that supply or operate the physical AI infrastructure layer, including AI server vendors, hyperscale cloud providers, data center REITs, power infrastructure companies, and networking equipment suppliers.

What Are the Top AI Data Center Stocks in 2026?

Six names define the 2026 AI data center thesis. NVIDIA supplies the GPUs that power the buildout, AMD provides the alternative compute platform and server CPU franchise, Amazon and Microsoft operate the two largest hyperscale clouds, Oracle is the fastest-growing cloud infrastructure provider through its OCI and Stargate exposure, and Super Micro Computer assembles the rack-scale AI servers that connect everything together.

1. NVIDIA (NVDA)

Core Role: AI GPU compute and CUDA software ecosystem

NVIDIA remains the central compute supplier for AI data centers in 2026. Its GPUs power most frontier training workloads and an increasing share of inference, while CUDA continues to act as the software moat that keeps developers, AI frameworks, and enterprise infrastructure closely tied to NVIDIA hardware.

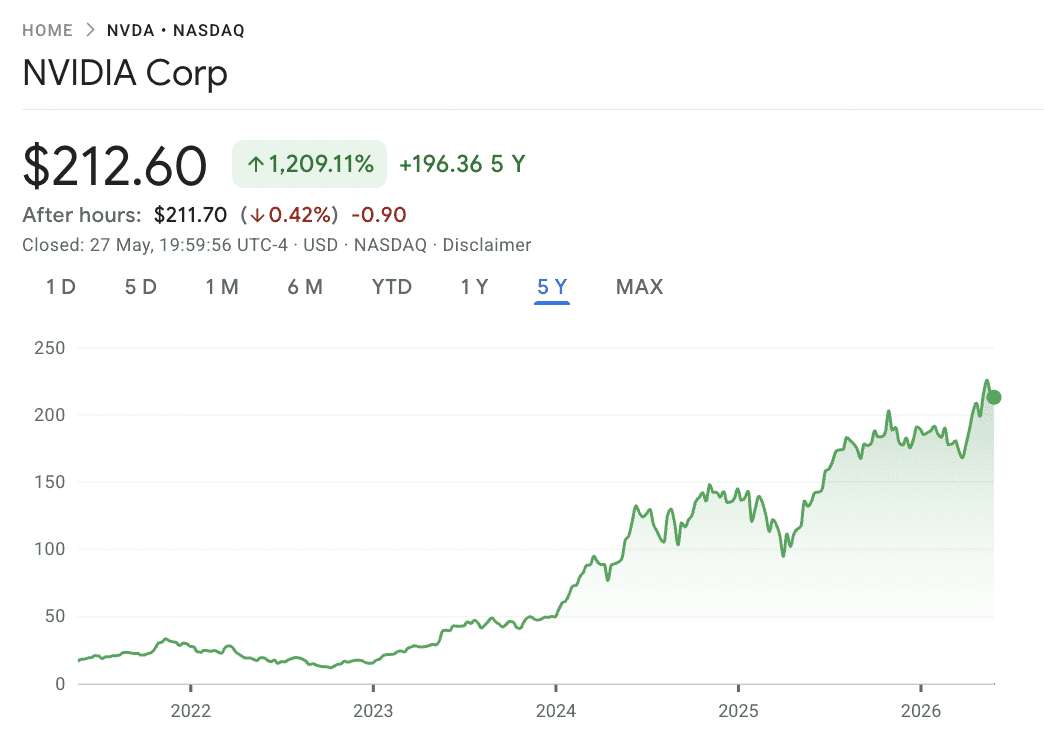

Q1 FY2027 results reinforced that position, with revenue of $81.6 billion and adjusted EPS of $1.87, ahead of consensus. The next major catalyst is the Vera Rubin platform, scheduled for the second half of 2026, which management expects to remain supply-constrained throughout its lifecycle. With a market cap near $5.4 trillion, NVIDIA is still the most direct large-cap exposure to AI compute demand.

The key reason NVIDIA remains difficult to replace is its developer ecosystem. Hyperscaler custom silicon may reduce reliance on GPUs for some inference workloads, but most AI frameworks still optimize for CUDA first. That makes custom chips an incremental competitive pressure rather than a full replacement for NVIDIA’s role in AI data centers.

Read More: Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

NVDA Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$15.06 |

$4.83 |

1.2192 |

Pandemic-era gaming and data center demand |

|

2021 |

$33.36 |

$11.50 |

1.2539 |

Crypto mining peak; data center momentum |

|

2022 |

$30.04 |

$10.81 |

−50.27% |

Crypto bust; mining card glut; Fed rate hikes |

|

2023 |

$50.41 |

$14.10 |

2.3902 |

ChatGPT moment; Hopper ramp; AI rally begins |

|

2024 |

$152.89 |

$45.95 |

1.712 |

Blackwell launch; market cap surpasses $3 trillion |

|

2025 |

$190.95 |

$86.62 |

0.2579 |

Consolidation year; Blackwell shipments scale |

|

2026 YTD |

~$220 (May) |

~$140 (Jan) |

+45% YTD (est.) |

Q1 FY27 beat; Rubin ramp positioning; $5.4T market cap |

2. Amazon (AMZN)

Core Role: AWS and hyperscale AI cloud infrastructure

Amazon remains one of the most important AI data center stocks through Amazon Web Services (AWS), the largest hyperscale cloud platform by absolute scale. In 2026, AWS is aggressively expanding AI capacity as enterprise demand for cloud compute, training infrastructure, and inference workloads continues to accelerate.

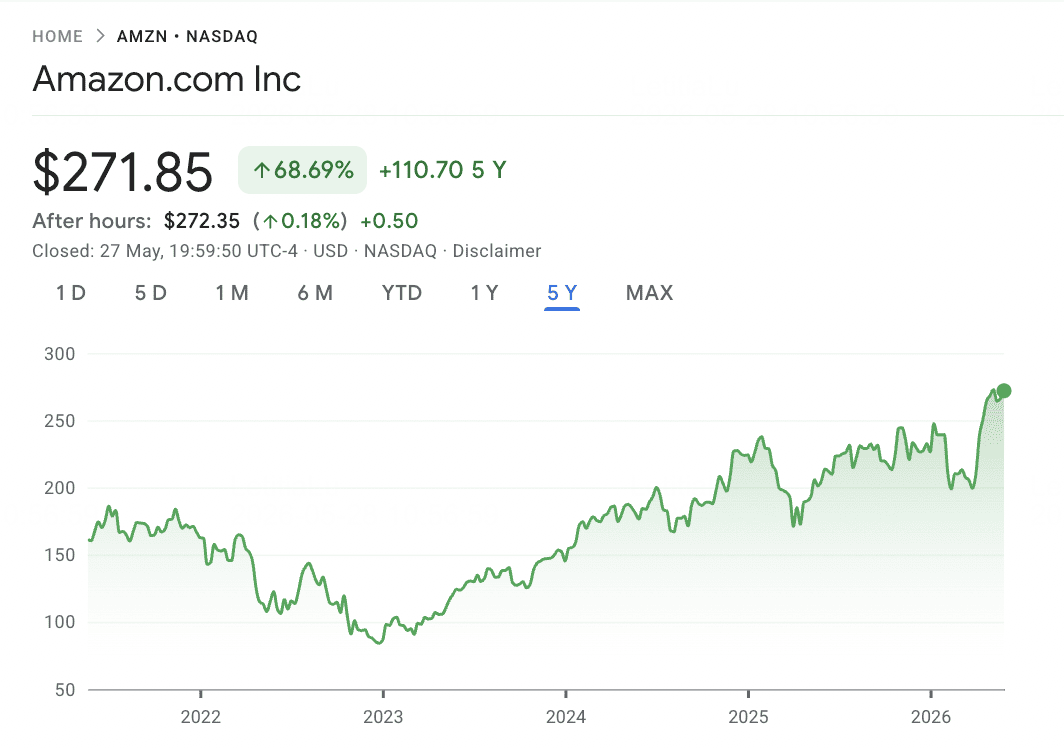

Q1 FY2026 revenue reached $181.5 billion, up 17% year over year, while AWS revenue grew 28% to $37.6 billion, its fastest pace in fifteen quarters. Amazon’s Q1 capex reached $43.2 billion, putting the company on track for roughly $200 billion in full-year spending as it reinvests heavily into data center capacity, AI infrastructure, and custom silicon.

The key thesis is that Amazon is monetizing AI infrastructure quickly as new capacity comes online. AWS reached an annualized revenue run rate of $142 billion, while AWS AI revenue now runs at roughly $15 billion annually, up from about $5 billion entering 2025. Trainium 2 and Inferentia 3 also give Amazon a vertically integrated custom silicon roadmap, helping reduce dependence on external GPU supply over time.

Read More: Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

AMZN Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$176.57 |

$83.83 |

0.7626 |

Pandemic e-commerce surge; AWS demand acceleration |

|

2021 |

$186.57 |

$147.60 |

0.0238 |

Post-pandemic consolidation; mixed retail signals |

|

2022 |

$170.41 |

$81.82 |

−49.62% |

Tech sell-off; AWS margin compression; layoffs begin |

|

2023 |

$154.07 |

$83.12 |

0.8088 |

AI narrative; AWS reacceleration; cost discipline |

|

2024 |

$232.93 |

$144.57 |

0.4439 |

AWS growth resumes above 19%; Anthropic stake expands |

|

2025 |

$242.06 |

$167.32 |

−2.82% |

Capex visibility concerns; consolidation phase |

|

2026 YTD |

$278.56 (52-wk) |

$196.00 (52-wk) |

+~22% YTD |

$200B capex committed; AWS +28%, $142B run rate; market cap $2.56T |

3. Microsoft (MSFT)

Core Role: Azure cloud and OpenAI partnership infrastructure

Microsoft is one of the most important AI data center stocks because Azure sits directly behind much of the frontier AI workload growth. Its partnership with OpenAI gives Microsoft unique exposure to large-scale model training, inference demand, and enterprise AI adoption through products like ChatGPT, Copilot, and GitHub Copilot.

Azure has continued growing above 35% in 2026, but the main constraint is capacity rather than demand. Management has cited more than $80 billion in unfulfilled Azure orders, with power availability acting as a major bottleneck. Microsoft has also set 2026 calendar-year capex at roughly $190 billion, above prior expectations, with part of the increase tied to rising memory and component costs.

Microsoft’s advantage is breadth across the AI stack. The company combines Azure infrastructure, OpenAI model access, Copilot applications, developer tools, and its own custom silicon roadmap through Cobalt CPUs and Maia AI accelerators. The risk is that investors are still digesting the scale of the capex commitment, even as demand remains supply-constrained.

Read More: Microsoft (MSFT) Stock Outlook for 2026: Can Azure AI and Copilot Growth Drive MSFT Stock to $550+?

MSFT Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$222.48 |

$129.38 |

0.4253 |

Pandemic-era cloud demand acceleration |

|

2021 |

$333.16 |

$204.38 |

0.5248 |

Azure growth above 50%; productivity software strength |

|

2022 |

$325.04 |

$209.39 |

−28.02% |

Tech sell-off; Azure decel; layoffs begin |

|

2023 |

$378.41 |

$217.88 |

0.5819 |

OpenAI partnership expands; Copilot launch; AI re-rating |

|

2024 |

$464.00 |

$363.62 |

0.1293 |

Azure AI capacity sold out; capex visibility scrutiny |

|

2025 |

$555.45 |

$352.67 |

0.1558 |

July 2025 all-time high; capex doubt drives pullback |

|

2026 YTD |

$483.47 |

$393.67 |

−16.42% YTD (Feb) |

$190B 2026 capex set; Azure +39%, supply-constrained; current ~$418 |

4. Advanced Micro Devices (AMD)

Core Role: Alternative AI GPU compute and data center CPU platform

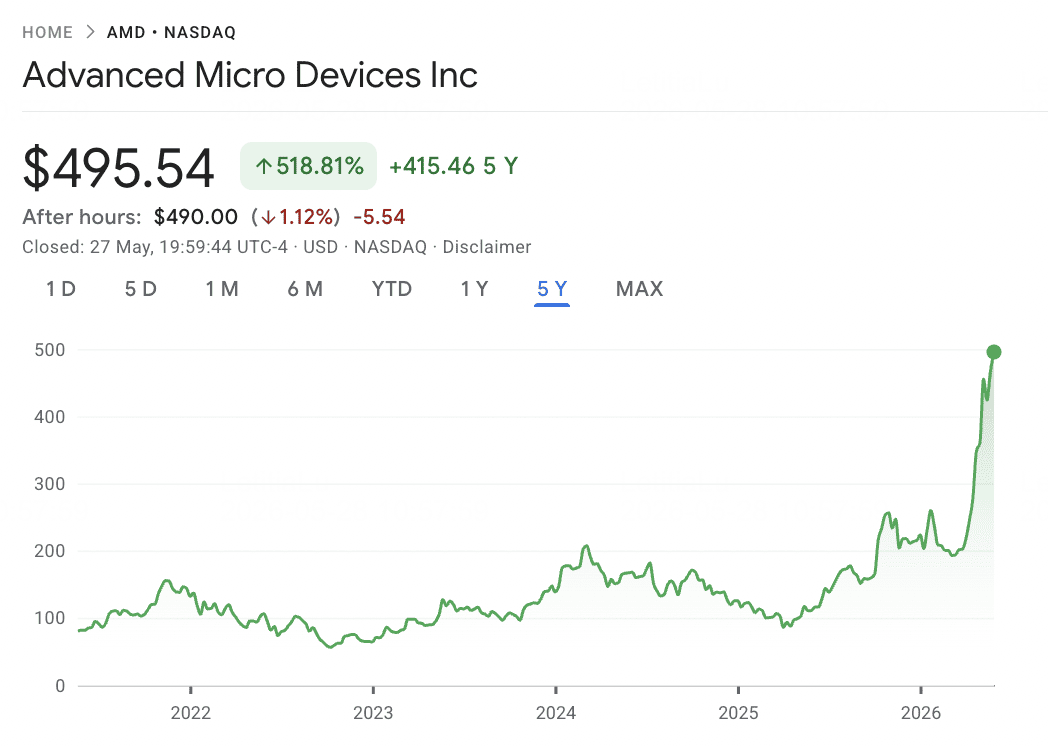

AMD s the primary commercial alternative to NVIDIA in AI accelerators, while its EPYC server CPU franchise gives it a strong position inside data center infrastructure. The MI300 series built momentum through 2025, and the upcoming MI450 platform is central to a multi-year Meta agreement to deploy up to 6 gigawatts of AMD Instinct GPUs across its AI infrastructure.

Q1 2026 revenue reached $10.3 billion, up 38% year over year, while Data Center revenue rose 57% to $5.8 billion. Management guided Q2 revenue to roughly $11.2 billion, above consensus, reflecting strong demand for both AI accelerators and server CPUs.

The underappreciated part of AMD’s thesis is the CPU side. Agentic AI workloads increase CPU requirements for every accelerator deployed, supporting AMD’s expectation for server CPU revenue to grow more than 70% in 2026. Shares are up roughly 66% year to date, with investor focus now on MI450 execution and continued EPYC share gains.

Read More: AMD Price Prediction 2026: $525 AI Sovereignty or $300 Valuation Trap?

AMD Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$97.98 |

$36.75 |

0.9998 |

Pandemic gaming and data center surge |

|

2021 |

$164.46 |

$72.50 |

0.5691 |

EPYC share gains; data center growth |

|

2022 |

$155.42 |

$54.57 |

−54.95% |

Tech sell-off; PC market weakness |

|

2023 |

$151.05 |

$60.05 |

1.2759 |

AI rally; MI300 launch expectations |

|

2024 |

$227.30 |

$116.37 |

−18.20% |

MI300 shipments begin but margin disappoints |

|

2025 |

$215.00 |

$78.21 |

0.22 |

Stabilization; Meta GPU deal speculation |

|

2026 YTD |

~$352 (Apr) |

~$210 (Jan) |

+66% YTD |

Meta 6 GW deal confirmed; Q1 rev +38%; Data Center +57% |

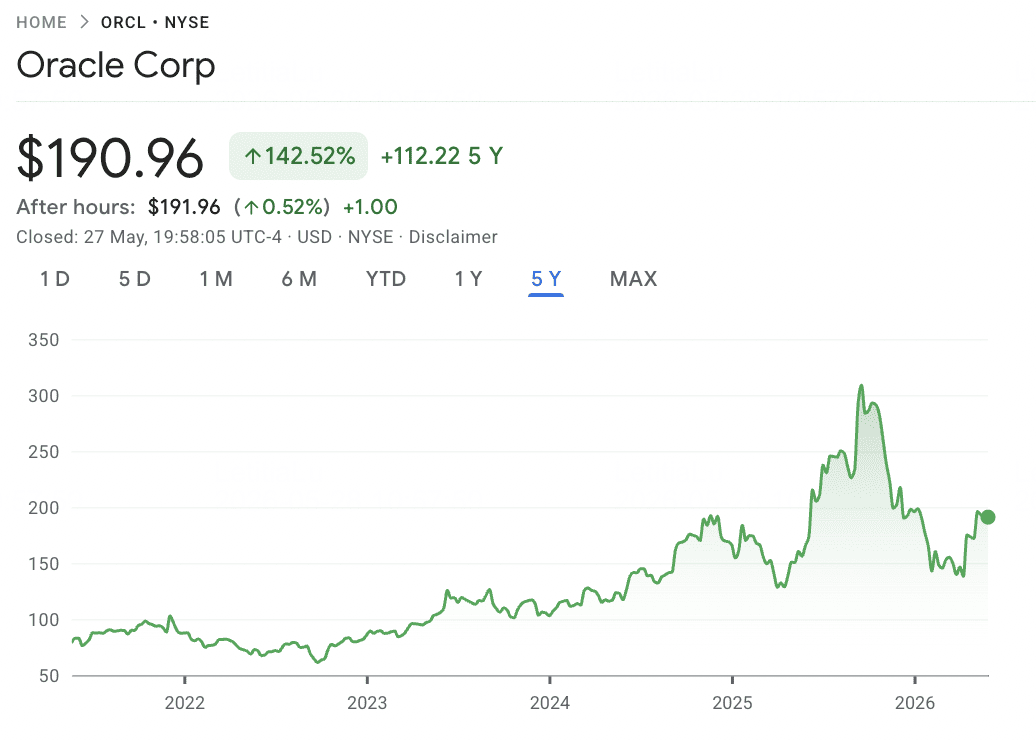

5. Oracle (ORCL)

Core Role: OCI cloud infrastructure and Stargate AI buildout partner

Oracle has become one of the fastest-growing AI cloud infrastructure names through Oracle Cloud Infrastructure (OCI) and its Stargate partnership with OpenAI. Once known primarily for enterprise databases, Oracle is now building large-scale AI data center capacity to support frontier model training and inference workloads.

Q3 FY2026 results showed how quickly the business is shifting. Total revenue reached $17.2 billion, up 22% year over year, while cloud services revenue grew 44% to $8.9 billion. OCI revenue surged 84% to $4.9 billion, AI-specific infrastructure revenue jumped 243%, and contracted backlog increased 325% to $553 billion.

The main opportunity is the Stargate buildout, with Oracle constructing AI data center capacity across Texas, New Mexico, Wisconsin, and Michigan. The main risk is cash flow pressure: fiscal 2026 capex is expected to reach roughly $50.6 billion, pushing free cash flow deeply negative as Oracle invests ahead of revenue conversion.

Read More: Oracle (ORCL) Stock Price Outlook for 2026: Can AI Cloud Infrastructure Take ORCL Back to Its Highs?

ORCL Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

$61.00 |

$36.70 |

0.2425 |

Pandemic recovery; cloud transition early phase |

|

2021 |

$98.32 |

$56.60 |

0.3689 |

Cerner acquisition; OCI buildout accelerates |

|

2022 |

$85.01 |

$58.63 |

−4.65% |

Tech sell-off; Cerner integration overhang |

|

2023 |

$123.69 |

$80.38 |

0.3095 |

AI narrative emerges; OCI growth accelerates |

|

2024 |

$190.84 |

$100.39 |

0.5999 |

OpenAI Stargate partnership announced |

|

2025 |

$345.72 |

$122.56 |

0.4542 |

Stargate ramp; September peak; capex visibility concerns |

|

2026 YTD |

~$210 (May) |

$134.57 (Feb) |

+~15% YTD (est.) |

$553B RPO backlog; OCI +84%; Q3 FY26 beats; partial recovery from Feb low |

6. Super Micro Computer (SMCI)

Core Role: Rack-scale AI servers and liquid cooling systems

Super Micro Computer is one of the most direct AI server infrastructure plays on U.S. exchanges. The company builds complete rack-scale AI systems that integrate GPUs, CPUs, networking, memory, and liquid cooling. Its direct liquid cooling position is especially important as high-density AI data centers increasingly require more efficient thermal management.

Growth remains strong, but volatility is high. Trailing twelve-month revenue reached $33.7 billion through March 2026, up 56% year over year, and management maintained FY2026 revenue guidance of $36 billion to $40 billion. However, Q3 FY2026 included a $2.25 billion revenue miss versus consensus, mainly due to timing delays in data center orders, even though margins showed improvement.

The main risk is execution and governance. SMCI has faced delayed filings, auditor changes, accounting concerns, and headline risk, which have weighed heavily on the stock. Shares now trade around $35, far below the March 2024 high of $118.81. For investors, SMCI is a high-beta AI server stock with meaningful upside if rack-scale AI infrastructure demand accelerates, but also significant downside risk if execution problems continue.

SMCI Price Trend (2020–2026 YTD)

|

Year |

Yearly High |

Yearly Low |

Annual Return |

Market Conditions |

|

2020 |

~$8 |

~$3 |

0.45 |

Pandemic recovery; server demand modest |

|

2021 |

~$15 |

~$6 |

0.39 |

Data center hardware cycle begins |

|

2022 |

~$25 |

~$7 |

0.87 |

AI server early demand; GPU shortages |

|

2023 |

~$70 |

~$12 |

2.46 |

ChatGPT moment; AI server orders explode |

|

2024 |

$118.81 |

~$30 |

0.07 |

March 2024 ATH; 10-K delay, auditor change, governance issues |

|

2025 |

~$62 |

~$20 |

−~15% (est.) |

Auditor resolution; co-founder allegations; volatility extreme |

|

2026 YTD |

$62.36 (52-wk) |

$19.48 (52-wk) |

~flat YTD |

Q3 FY26 revenue miss; $36-40B FY26 guidance maintained; $21B market cap |

2026 AI Data Center Stocks Comparison by Supply Chain Role

AI data center stocks span the infrastructure stack, from hyperscale cloud platforms and AI servers to data center power, cooling, and networking. This comparison shows how each company captures a different part of the 2026 AI data center buildout.

|

Ticker |

Primary Role |

Core Advantage |

2026 Catalyst |

|

NVDA |

AI compute platform |

CUDA ecosystem and Vera Rubin GPU roadmap |

Q1 FY2027 beat; Rubin ramp in H2 2026 |

|

AMZN |

Hyperscale cloud infrastructure |

AWS scale, Trainium 2, and AI cloud monetization |

~$200B 2026 capex plan; AWS revenue growth reaccelerates |

|

MSFT |

Azure cloud and AI applications |

OpenAI partnership, Azure backlog, and Copilot ecosystem |

~$190B 2026 capex plan; $80B+ unfulfilled Azure demand |

|

AMD |

Alternative AI compute and server CPU |

MI450 accelerator roadmap and EPYC data center CPU franchise |

Q1 revenue +38%; Data Center revenue +57%; Meta 6GW deal |

|

ORCL |

OCI cloud and AI capacity buildout |

Stargate partnership and rapidly expanding cloud backlog |

OCI revenue +84%; RPO reaches $553B |

|

SMCI |

Rack-scale AI servers |

High-density AI server integration and liquid cooling systems |

FY2026 revenue guidance of $36–40B; margin recovery focus |

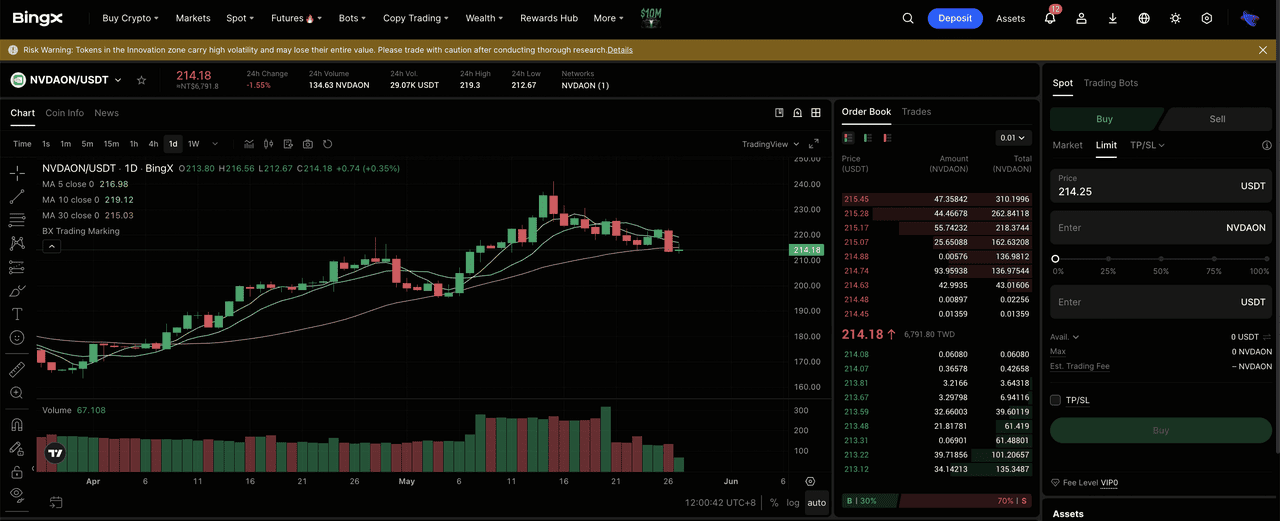

How to Trade AI Data Center Stocks on BingX

BingX offers two crypto-native ways to gain exposure to leading AI data center stocks without using a traditional brokerage account. Tokenized stocks on the BingX Spot market provide direct, non-leveraged price exposure for selected names such as NVDA, AMZN, and MSFT, while USDT-margined perpetual contracts on BingX TradFi allow active traders to go long or short on a broader set of AI data center stocks around earnings, capex announcements, and AI cycle headlines.

Trade AI Data Center Tokenized Stocks on BingX Spot

For long-term investors seeking direct equity price exposure without leverage, the BingX Spot market offers access to selected tokenized stocks that track underlying U.S. equities on a 1:1 economic basis through regulated asset frameworks such as Backed Finance and Ondo Finance. For the AI data center theme, available tokenized stock exposure may include names such as NVIDIA, Amazon, and Microsoft.

Step 1: Account setup and security. Sign up and log into your BingX account, complete the identity verification (KYC) in your region, and enable two-factor authentication.

Step 2: Fund your spot wallet. Deposit USDT using your preferred network, such as TRC-20, ERC-20, or Arbitrum. Check minimum deposit requirements and network fees before transferring.

Step 3: Navigate to the spot market. Search for available AI data center tokenized stock pairs, such as NVDAON/USDT, NVDAX/USDT, AMZNON/USDT, or MSFTON/USDT for fully backed, non-leveraged exposure.

Step 4: Use the BingX AI Analyst. The embedded BingX AI tool can surface support and resistance levels, moving averages, and volatility indicators directly on the chart.

Step 5: Execute and settle. Choose a market or limit order, enter your USDT amount, and confirm. Once filled, the tokenized stock balance appears in your spot wallet.

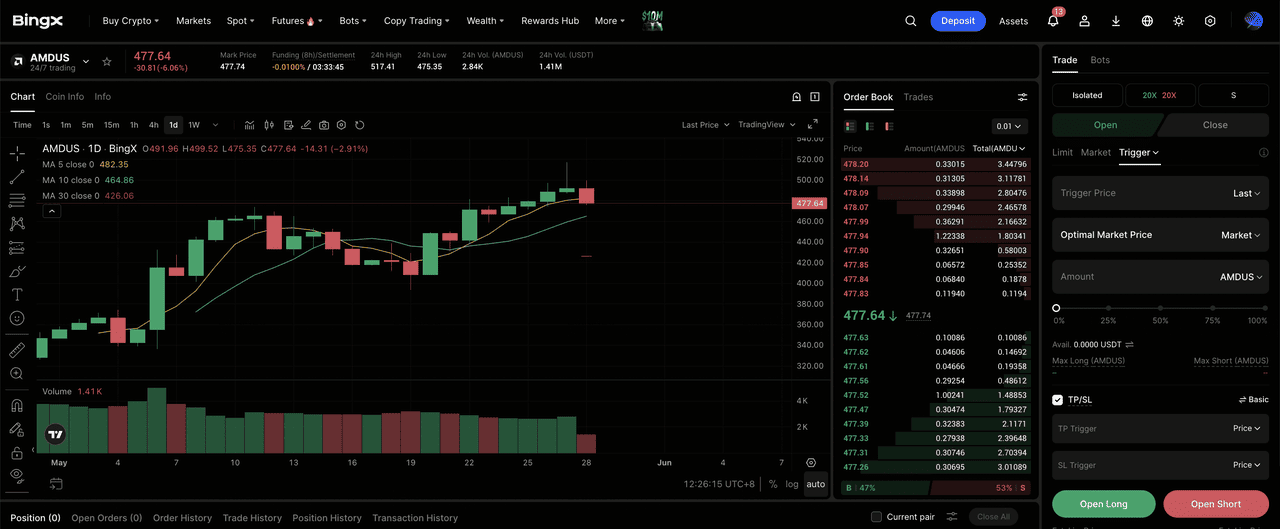

Trade AI Data Center Stock Futures with USDT on BingX TradFi

For active traders looking to capture short-term momentum or hedge exposure to the data center cycle, BingX TradFi allows users to trade GPU compute, hyperscale cloud, and AI server stock futures with USDT. These USDT-settled perpetual contracts mirror the price movements of underlying equities, offering flexible long and short exposure without requiring users to hold the physical stock.

Step 1: Account setup and security. Sign up and log into your BingX account, complete the identity verification required in your region, and enable two-factor authentication.

Step 2: Allocate trading capital. Transfer USDT from your spot wallet into your futures account, where it will serve as collateral.

Step 3: Select your contract. Navigate to the TradFi markets page or the futures trading section. Choose data center stock perpetuals such as NVDA-USDT, AMZN-USDT, MSFT-USDT, AMDUS-USDT, ORCL-USDT, or SMCI-USDT.

Step 4: Set direction and leverage. Open long if you expect the stock price to rise, or open short if you expect a pullback. Choose leverage based on your risk plan.

Step 5: Execute and manage risk. Set stop-loss and take-profit orders before submitting the trade. PnL settles dynamically in USDT.

Risks and Core Considerations When Trading Data Center Stocks

AI data center stocks offer exposure to one of the largest infrastructure cycles in technology, but they also carry risks tied to capital intensity, custom silicon competition, backlog conversion, power availability, and high short-term volatility.

- Hyperscaler capex execution risk: Amazon, Microsoft, and Oracle are spending record amounts on AI infrastructure. If AI revenue growth fails to keep pace with rising capex, free cash flow pressure could trigger rapid multiple compression.

- Custom silicon risk for NVIDIA: AWS Trainium, Google TPU, Microsoft Maia, and Meta MTIA are all designed to reduce long-term reliance on third-party GPUs. If hyperscaler custom chips gain inference share faster than expected, NVIDIA’s pricing power and margins could face pressure.

- Oracle backlog conversion risk: Oracle’s large RPO is closely tied to AI infrastructure and Stargate-related demand. Any delay in data center construction, power availability, or customer capacity commitments could push out revenue recognition and worsen free cash flow pressure.

- SMCI execution and governance risk: Super Micro has one of the highest-beta profiles in the AI data center group. Auditor scrutiny, compliance concerns, customer concentration, order timing delays, or margin pressure can create sharp earnings-related volatility.

- Power and grid bottlenecks: AI data center expansion is increasingly constrained by electricity access, cooling capacity, and grid interconnection timelines. Delays in power availability can push out capacity deployment for cloud and data center operators.

- Leverage and liquidation risk: Data center stocks can move sharply on earnings, capex updates, AI demand commentary, or policy headlines. Traders using USDT-margined futures should manage position size carefully and use stop-loss orders.

Final Thoughts: Should You Add AI Data Center Stocks to Your 2026 Portfolio?

The six names above offer different ways to participate in the 2026 AI data center buildout. NVIDIA captures the GPU compute layer, AMD provides exposure to both AI accelerators and server CPUs, Amazon and Microsoft anchor the hyperscale cloud thesis, Oracle offers high-growth cloud infrastructure exposure through OCI and Stargate-related demand, and Super Micro Computer provides direct exposure to rack-scale AI server deployment. Together, they cover the key parts of the AI data center stack, from compute and cloud capacity to server infrastructure.

The trade-off is that each stock carries a different risk profile. NVIDIA faces long-term custom silicon competition, Amazon and Microsoft face capex execution scrutiny, AMD faces MI450 ramp risk, Oracle faces backlog conversion and free cash flow pressure, and Super Micro Computer faces execution and governance risk. For traders using BingX TradFi, conservative position sizing, leverage control, and stop-loss orders are essential when trading AI data center stock futures through USDT-margined perpetual contracts.

Related Reading

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top AI Memory Stocks to Buy in 2026: DRAM, HBM, and AI Storage Demand Explained

- Top AI Chip Manufacturing Stocks to Buy in 2026: TSMC, ASML, and Advanced Chipmaking

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon