In April 2026, Occidental Petroleum (OXY) has emerged as the energy sector’s most aggressive pure play on crude oil volatility. While diversified giants like ExxonMobil offer a buffer through downstream refining, OXY’s streamlined portfolio, freshly shorn of its OxyChem division, is weaponized to capture maximum alpha from the current $100 WTI environment. Year-to-date, the stock has rocketed nearly 38%, fueled by a geopolitical war premium and the Warren Buffett effect, as Berkshire Hathaway maintains its massive 26.7% stake.

However, the road ahead is bifurcated. Bulls eye a $115 intrinsic value based on a Net-Zero Oil narrative and the Q2 commissioning of the STRATOS Direct Air Capture (DAC) facility. Conversely, skeptics point to a high 46x trailing P/E and the looming risk of a Middle East de-escalation that could send OXY back to its $55 support level. This guide analyzes the OXY stock price prediction for 2026 using data from Zacks Research, WallStreetZen, Simply Wall St, and Stephens.

You can also explore how to trade Occidental Petroleum (OXY) stock futures with USDT on BingX TradFi.

Top 5 Things for OXY Investors to Know in 2026

- The $15B Debt Milestone: Following the $9.7 billion sale of OxyChem to Berkshire Hathaway in January, OXY has successfully hit its long-term debt target, saving around $365 million in annual interest.

- STRATOS Launch in Q2 2026: The world’s largest DAC plant enters its operational phase in Texas this quarter. Success here could trigger a tech-like valuation re-rating for OXY’s Low Carbon Ventures.

- Permian Concentration: With the integration of CrownRock, OXY is now a concentrated bet on U.S. shale, producing around 1.48 Moebd (million barrels of oil equivalent per day).

- The CEO Transition: With Vicki Hollub retiring, incoming CEO Richard Jackson and former COO is expected to pivot from big swing acquisitions toward surgical operational efficiency.

- Oil Price Sensitivity: OXY prints massive cash at $100/bbl, but its high leverage relative to peers means a drop below its $60/bbl breakeven would be disproportionately painful.

What Is Occidental Petroleum (OXY)?

Occidental Petroleum is a leading U.S.-based upstream energy company with a market capitalization of approximately $56 billion. Unlike its integrated peers, OXY has focused its 2026 strategy on two pillars: High-margin shale extraction across Permian, DJ Basin, Gulf of Mexico basins and Carbon Management.

By divesting its chemicals business in early 2026, OXY has transitioned into a leaner organization. Its subsidiary, 1PointFive, is currently the industry leader in Direct Air Capture, aiming to produce the world's first Net-Zero Barrel by offsetting extraction emissions with atmospheric CO2 removal. This unique ESG-plus-Alpha profile is what originally attracted Warren Buffett’s Berkshire Hathaway to build a dominant stake.

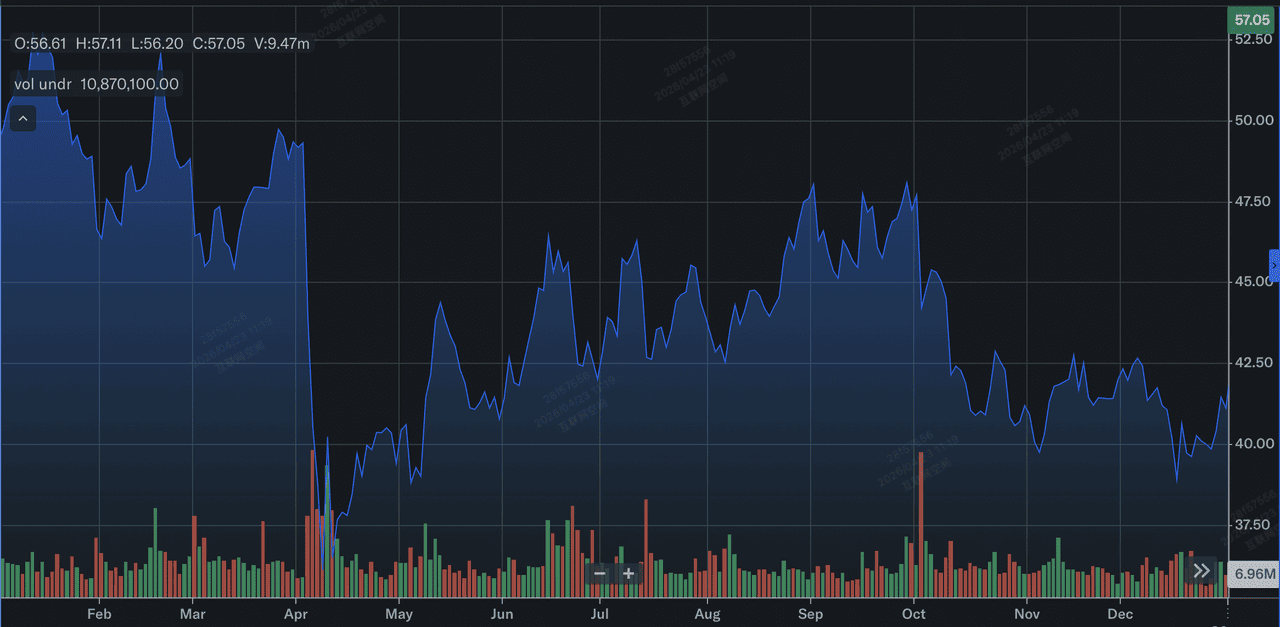

OXY Stock Performance in 2025: A Review

Occidental Petroleum (OXY) stock performance in 2025 | Source: Yahoo Finance

2025 was a year of The Great Repair for Occidental Petroleum. After a lackluster 2024 where the stock declined 31%, OXY spent 2025 integrating the $12 billion CrownRock acquisition. This move boosted Permian production by 8% year-over-year, providing the volume needed to offset fluctuating crude prices.

Financially, OXY generated $4.3 billion in free cash flow before working capital in 2025. While GAAP earnings faced pressure from lower year-over-year commodity prices, the company used its cash to aggressively retire high-interest debt. By the end of Q4 2025, OXY had lowered its domestic operating costs by 17% since 2023, setting the stage for the massive breakout seen in the first quarter of 2026.

Key Strategic Priorities for Occidental Petroleum in 2026

In 2026, Occidental Petroleum is pivoting from a period of aggressive consolidation and debt reduction toward a high-margin, dual-track strategy focused on U.S. shale dominance and the commercialization of its carbon-management technology.

- Operational Integration of CrownRock: Maximizing synergies from the $12 billion acquisition to push Permian Basin production toward a sustained target of 1.5 million barrels of oil equivalent per day.

- STRATOS Commercialization: Completing the commissioning of the world’s largest Direct Air Capture (DAC) facility in the Permian Basin to prove the financial viability of Carbon-as-a-Service and net-zero oil production.

- Balance Sheet Optimization: Utilizing the $9.7 billion in proceeds from the OxyChem sale to maintain a target debt floor of $15 billion, thereby improving the company’s credit rating and lowering future cost of capital.

- Enhanced Shareholder Distributions: Leveraging high free cash flow from $100+ oil prices to accelerate share buybacks and sustain the 8% quarterly dividend increase announced in early 2026.

- Leadership Transition Stability: Executing a seamless handover from long-time CEO Vicki Hollub to Richard Jackson, with a strategic focus on shifting from big swing M&A toward surgical cost-efficiency and technical innovation.

Read more: Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?

Occidental (OXY) Stock Forecast 2026: $115 Alpha vs. $55 Mean Reversion

Predictions for Occidental (OXY) stock in 2026 by various Wall Street analysts

The 2026 outlook for Occidental Petroleum (OXY) stock is a high-stakes tug-of-war between record-breaking Permian production volumes and the sustainability of a geopolitical war premium currently baked into crude prices.

The Bull Case: Occidental's $115 Carbon Tech Alpha

The bullish narrative centers on a valuation re-rating where OXY evolves from a cyclical driller into a premier climate-tech leader. If the STRATOS DAC facility hits its 500,000-metric-ton operational target this quarter, OXY will prove the commercial viability of Carbon-as-a-Service, potentially attracting ESG-mandated capital that has historically avoided the sector.

Data-driven bulls point to a massive gap between OXY’s current price and its $115.62 DCF intrinsic value. With WTI crude holding above $100 due to persistent Middle East supply risks, OXY's leaner balance sheet, now capped at $15 billion in debt, is positioned to funnel record free cash flow into aggressive share buybacks, effectively weaponizing its 1.48 Moebd production capacity to drive a tech-like earnings multiple expansion.

The Base Case: $70 Fair Value Consolidation for OXY Stock

The base case assumes a soft landing for energy markets where crude stabilizes in a healthy $80–$90 corridor. In this scenario, the stock oscillates near the analyst consensus target of $70, supported by the Buffett floor. With Berkshire Hathaway holding a 26.7% stake and OXY recently increasing its quarterly dividend by 8%, the stock becomes a premier yield-plus-growth anchor for energy-weighted portfolios.

Practically, this scenario relies on OXY hitting its $5.5–$5.9 billion capital expenditure efficiency targets. By integrating CrownRock assets without further major M&A, OXY maintains a steady 11.2% Return on Equity (ROE). This allows the company to balance $1.2 billion in operational efficiency gains against moderate commodity price cooling, keeping the stock in a disciplined 'buy the dip' range for long-term income investors.

The Bear Case: Occidental Stock's $55 Geopolitical Mean Reversion

The bear case is defined by a sudden peace dividend and the resulting evaporation of the $20/bbl risk premium. If diplomatic breakthroughs in the Middle East reopen the Strait of Hormuz, oil could rapidly mean-revert to its $60 breakeven floor. At $57, OXY’s current trailing P/E of 46x would appear dangerously overextended compared to an industry average of 15x, triggering a sharp rotation out of high-beta energy plays.

From a risk management perspective, the bear case highlights OXY’s vulnerability to its high capital intensity. If free cash flow is squeezed by $70 oil while debt remains at $15 billion, the pace of buybacks could stall, forcing a revaluation toward the $55 level. Analysts at Goldman Sachs and Evercore ISI warn that without the tailwind of triple-digit crude, OXY’s U.S.-centric concentration becomes a liability rather than a strength, leading to a potential 15%–20% valuation haircut.

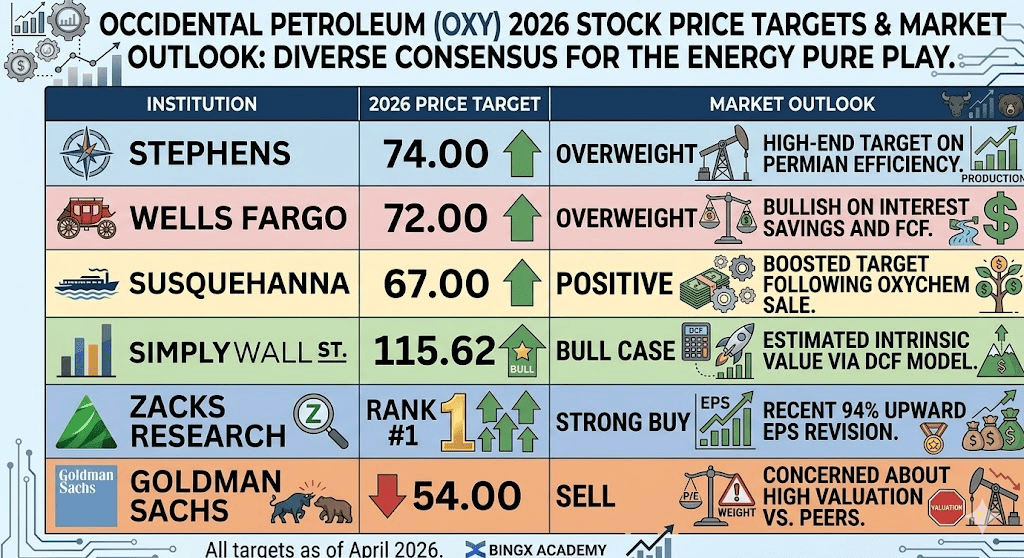

Occidental (OXY) Investment Outlook and Prediction 2026 by Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Stephens |

$74.00 |

Overweight: High-end target on Permian efficiency. |

|

Wells Fargo |

$72.00 |

Overweight: Bullish on interest savings and FCF. |

|

Susquehanna |

$67.00 |

Positive: Boosted target following OxyChem sale. |

|

Simply Wall St |

$115.62 |

Bull Case: Estimated intrinsic value via DCF model. |

|

Zacks Research |

Rank #1 |

Strong Buy: Recent 94% upward EPS revision. |

|

Goldman Sachs |

$54.00 |

Sell: Concerned about high valuation vs. peers. |

How to Trade Occidental Petroleum (OXY) on BingX

Navigate the high-beta volatility of OXY using BingX TradFi tools. Whether you’re betting on the STRATOS rollout or hedging against an oil price crash, BingX offers 24/7 liquidity powered by automated insights from BingX AI.

OXYUS/USDT perpetual contract on the BingX futures market

Long or Short OXY Stock Futures on BingX

- Access TradFi: Go to the BingX TradFi section and select Stock Futures.

- Find OXY: Search for the OXYUS/USDT perpetual contract.

- Leverage Up: Apply 2x–5x leverage. Use Open Long if you believe the $100 oil narrative or Open Short to hedge against a geopolitical cooldown.

- Set Protection: Always apply Stop-Loss (SL) to protect against sudden OPEC+ policy shifts.

Final Thoughts: Is Occidental Premium (OXY) a Good Buy in 2026?

Occidental Petroleum enters the second quarter of 2026 as a high-conviction, high-beta play on both energy markets and industrial decarbonization. With a consensus Zacks Rank #1 and recent EPS revisions trending 94% higher, the technical setup suggests strong momentum heading into the May 5 earnings call. For investors, the decision rests on whether they view OXY as a traditional oil driller, where its 46x trailing P/E appears overextended, or as a pioneering Carbon-as-a-Service firm whose intrinsic value, supported by the STRATOS facility and a $115 DCF fair value, has yet to be fully realized by the broader market.

Practically, the Buffett floor provided by Berkshire Hathaway’s 26.7% stake offers a unique layer of downside protection that most mid-cap energy peers lack. While the stock has already rallied 38% year-to-date, the shift under new leadership toward operational efficiency and aggressive debt reduction makes it a robust vehicle for capturing energy alpha. Investors should monitor WTI crude levels closely; as long as oil remains above the $60/bbl breakeven, OXY’s leaner balance sheet and record Permian production levels position it as a top-tier candidate for both income and growth portfolios through 2026.

Risk Reminder: Trading and investing in Occidental Petroleum (OXY) involves substantial risk. The stock is highly sensitive to geopolitical developments in the Middle East and global crude oil price fluctuations. A sudden de-escalation in regional conflicts or a drop in oil prices below $60 could lead to rapid capital depreciation. Always perform independent due diligence and consider your risk tolerance before allocating capital to high-volatility energy assets.

Related Reading

- Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?

- Exxon Mobil (XOM) Price Prediction 2026: $180 Energy Alpha or Geopolitical Value Trap?

- Cheniere Energy (LNG) Price Prediction 2026: $330 Sovereign Boom or $210 Infrastructure Trap?

- How to Trade Commodities With Crypto in 2026 as Oil, Gold, Silver, and TradFi Go On-Chain