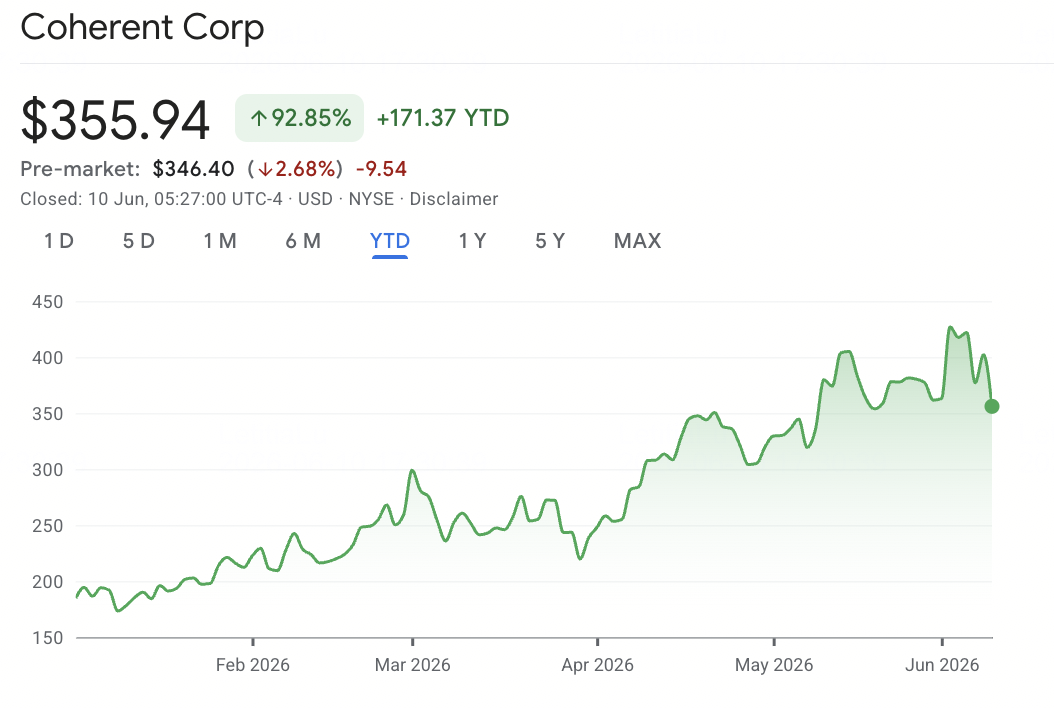

In early June 2026, Coherent Corp. (NYSE: COHR) sits at the center of the AI optical networking boom. Once valued mainly as a diversified photonics and industrial laser company, Coherent has become a key supplier of high-speed optical transceivers, co-packaged optics (CPO), and optical circuit switches (OCS) for AI data centers. Its leadership in 800G and 1.6T transceiver technology, combined with NVIDIA’s $2 billion equity investment and multi-year supply commitment, has pushed the stock to a 52-week high of $440 and lifted year-to-date gains above 108%. The key question is whether the optical networking supercycle still has room to run.

The bull case is built on accelerating revenue growth, improving margins, and a backlog stretching into 2028, with long-term agreements running through the end of the decade. Jensen Huang’s Computex 2026 comments on optical networking as a key AI infrastructure bottleneck reinforced the view that COHR is a critical supplier for next-generation AI racks. The risk is that the stock now trades above the average Wall Street consensus target, while debt from past acquisitions, weakness in industrial demand, and a forward P/E above 49x leave little room for execution mistakes. This guide breaks down the Coherent stock forecast, 2026 price scenarios, key risks, and how to trade COHR stock futures on BingX TradFi with USDT collateral.

Why Is Coherent (COHR) Stock Surging in 2026?

Coherent’s 2026 rally is driven by record AI data center demand, NVIDIA’s strategic investment, S&P 500 inclusion, the 6-inch indium phosphide ramp, and a larger optical circuit switch opportunity.

- Coherent’s Q3 FY2026 beat shows AI data center demand is reshaping the business: Coherent reported Q3 FY2026 revenue of $1.81 billion, up 21% year over year, while non-GAAP EPS rose 55% to $1.41. Data center and Communications revenue grew 41% to $1.36 billion and now accounts for 75% of total revenue, showing that Coherent is increasingly being valued as an AI optical networking supplier.

- NVIDIA’s $2 billion partnership gives Coherent rare demand visibility: NVIDIA’s strategic agreement includes a $2 billion equity investment and a multi-billion-dollar purchase commitment tied to advanced laser and optical networking products. The deal strengthens Coherent’s position as a key optics supplier for future AI infrastructure, especially as data centers move toward co-packaged optics and faster networking.

- S&P 500 inclusion turned COHR into a benchmark AI infrastructure stock: Coherent’s S&P 500 inclusion expanded its institutional investor base and triggered passive index buying. It also shifted market perception from a cyclical photonics and industrial laser company toward a benchmark-relevant AI infrastructure supplier.

- The 6-inch indium phosphide ramp supports the 1.6T and CPO upgrade cycle: Coherent’s 6-inch indium phosphide ramp is a key manufacturing milestone. The company shipped its first transceivers using 6-inch components during Q3, with yields already exceeding older 3-inch lines. This capacity supports future 800G, 1.6T, and co-packaged optics revenue.

- The optical circuit switch market is becoming a larger AI networking opportunity: Coherent raised its optical circuit switch market opportunity to more than $4 billion and is ramping OCS output across two facilities. Together, transceivers, CPO, and OCS give Coherent exposure to several overlapping AI optical hardware markets.

Read More: Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

What Is Coherent (NYSE: COHR)?

Coherent Corp. (NYSE: COHR) is a Saxonburg, Pennsylvania-based photonics company with businesses across optical networking, lasers, precision optics, and engineered materials. Founded in 1971 and expanded through the Finisar and II-VI acquisitions, Coherent now operates through two main segments: data center and Communications, which supplies optical transceivers, laser components, optical circuit switches, and co-packaged optics, and Industrial, which provides laser systems and optical materials for semiconductor, electronics, medical, and scientific applications.

Coherent’s key advantage is vertical integration. Unlike pure-play transceiver vendors, the company controls much of the photonics stack, from indium phosphide and silicon carbide materials to chip fabrication, module assembly, and system-level products. This gives Coherent direct exposure to the AI networking upgrade cycle, including 800G and 1.6T data center transceivers, co-packaged optics, optical circuit switches, AI data center interconnect products, and thermal management solutions for AI chip cooling.

Coherent’s Performance in Early 2026: AI Optics Growth and Operating Leverage

Coherent entered fiscal 2026 with a clearer focus on AI optical infrastructure. After divesting non-core assets, including its aerospace and defense business and Munich operations, the company concentrated more capital on data center demand. For the nine months ended March 31, 2026, revenue reached $5.07 billion, up 19% year over year, while data center and Communications revenue grew 34% to $3.66 billion.

Q3 FY2026 showed that this growth is starting to translate into better profitability. Non-GAAP gross margin expanded to 39.6%, and non-GAAP EPS rose 55% year over year to $1.41. Management guided Q4 FY2026 revenue of $1.91 billion to $2.05 billion, implying an annualized revenue run rate approaching $8 billion. With backlog extending into 2028 and long-term agreements running through the end of the decade, Coherent now has unusually strong revenue visibility for a hardware company in the middle of a technology upgrade cycle.

Read More: Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

Coherent’s 2026 Trading Strategy: Navigating the Optical Infrastructure Supercycle

To trade Coherent’s 2026 rally, investors need to watch three forces: whether COHR can hold its premium valuation, whether CPO revenue begins ramping on schedule, and whether macro sensitivity or industrial weakness offsets data center strength.

1. The $330 to $360 Zone Is the Key Support Floor

Technical analysts see the $330 to $360 range as the main support zone, where the 50-day moving average overlaps with the breakout level after Q3 FY2026 earnings. COHR’s 52-week range of roughly $148 to $440 shows how sensitive the stock is to AI infrastructure sentiment. A decisive break below $300 could shift the market toward more conservative valuation targets and open downside toward $230 to $250, while confirmed support above $350 would strengthen the setup ahead of Q4 FY2026 earnings.

2. The Main Valuation Debate Is AI Infrastructure Premium vs. Optical Commodity Risk

The bullish case values Coherent as an AI infrastructure bottleneck with NVIDIA-backed demand visibility, justifying premium multiples based on future CPO and OCS revenue. The cautious case is that COHR already trades at a rich valuation, leaving limited tolerance for weaker AI capex, slower CPO adoption, or margin disappointment. For swing traders, the key near-term catalyst is the Q4 earnings update and any commentary on CPO revenue contribution in the second half of 2026.

3. Sector Correlation and Industrial Recovery Can Amplify the Trade

COHR often moves with the broader optical networking group, including Lumentum, Applied Optoelectronics, and Corning, so NVIDIA earnings, hyperscaler capex guidance, and data center construction trends can move the stock even without company-specific news. The Industrial segment is another swing factor: continued weakness could weigh on headline growth, while a faster recovery in semiconductor processing, EV laser applications, or industrial photonics could add upside beyond the data center story.

Read More: Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

The Coherent 2026 Forecast: $460+ CPO Upside vs. $230 Industrial Drag Risk

Coherent’s 2026 outlook depends on one central question: can the company turn its record backlog, NVIDIA partnership, and 6-inch indium phosphide ramp into CPO and OCS revenue that justifies its premium valuation? The bull case is built on AI data center optical demand booked through 2028, while the bear case centers on valuation compression if CPO revenue ramps slower than expected or if AI infrastructure spending begins to cool.

The Bull Case: COHR Breaks Above $460 on CPO Revenue Ramp

The bullish scenario depends on CPO revenue beginning to scale in the second half of 2026 and OCS moving toward its $4 billion-plus market opportunity. NVIDIA’s $2 billion investment is the key anchor, acting as a supply commitment, R&D partnership, and public endorsement of Coherent’s role in next-generation AI infrastructure. If CPO contributes meaningfully to FY2027 margins and OCS backlog converts faster than expected, COHR could break above the street-high target near $460 and move toward the $500 range as analysts raise addressable market and margin assumptions.

The Base Case: COHR Consolidates Between $330 and $420

The base case is valuation digestion. data center and Communications revenue continues growing, the 6-inch indium phosphide ramp supports incremental margin improvement, and CPO begins contributing revenue without yet dominating the mix. Under this scenario, COHR trades between $330 and $420 as investors wait for Q4 FY2026 earnings to confirm whether guidance can convert into the EPS and cash-flow trajectory needed to support the current multiple.

The Bear Case: COHR Falls Toward $230 if Optical Spending Slows

The bearish scenario is driven by either a delayed CPO ramp or weaker hyperscaler AI capex momentum. At COHR’s current valuation, even one quarter of disappointing margin progress or softer guidance could trigger a sharp pullback toward the $230 to $250 range, where more conservative targets and cash-flow-based valuations converge. Continued industrial weakness and recent insider selling add caution, especially if AI optical networking sentiment starts to cool.

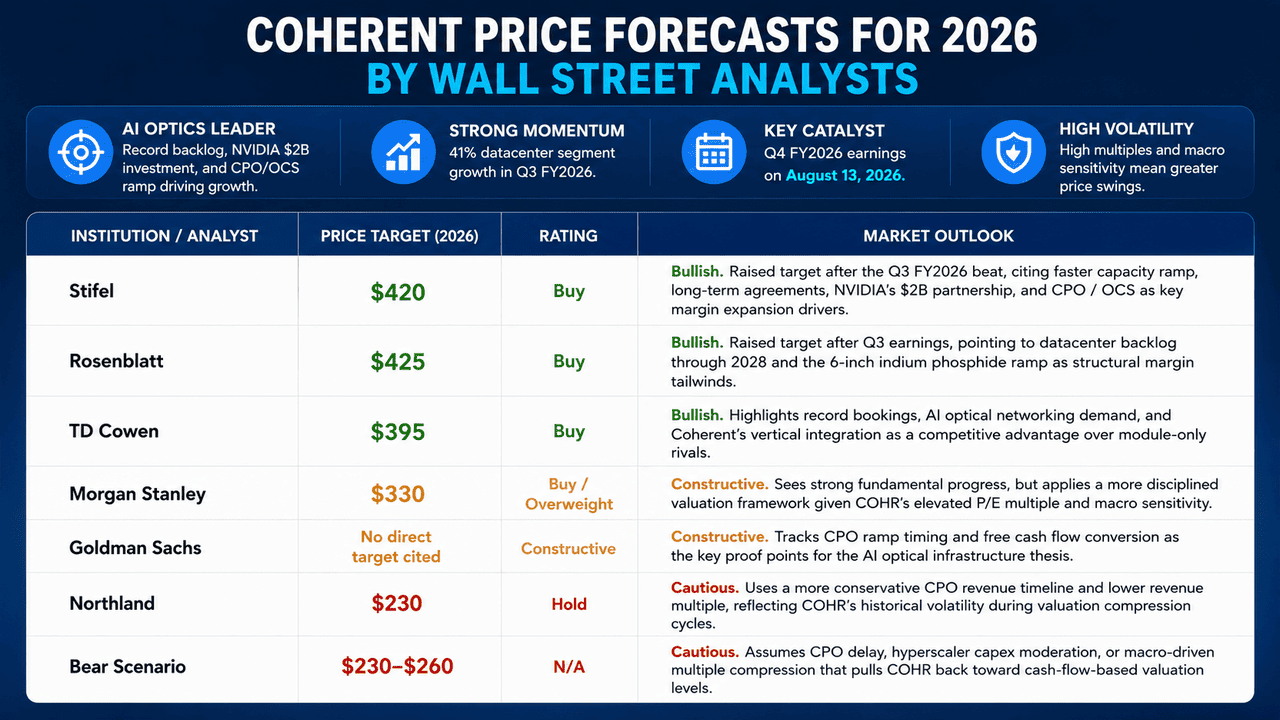

Coherent Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Analyst |

Price Target |

Rating |

Market Outlook |

|

Stifel |

$420 |

Buy |

Bullish. Raised target after the Q3 FY2026 beat, citing faster capacity ramp, long-term agreements, NVIDIA’s $2B partnership, and CPO / OCS as key margin expansion drivers. |

|

Rosenblatt |

$425 |

Buy |

Bullish. Raised target after Q3 earnings, pointing to data center backlog through 2028 and the 6-inch indium phosphide ramp as structural margin tailwinds. |

|

TD Cowen |

$395 |

Buy |

Bullish. Highlights record bookings, AI optical networking demand, and Coherent’s vertical integration as a competitive advantage over module-only rivals. |

|

Morgan Stanley |

$330 |

Buy / Overweight |

Constructive. Sees strong fundamental progress, but applies a more disciplined valuation framework given COHR’s elevated P/E multiple and macro sensitivity. |

|

Goldman Sachs |

No direct target cited |

Constructive |

Constructive. Tracks CPO ramp timing and free cash flow conversion as the key proof points for the AI optical infrastructure thesis. |

|

Northland |

$230 |

Hold |

Cautious. Uses a more conservative CPO revenue timeline and lower revenue multiple, reflecting COHR’s historical volatility during valuation compression cycles. |

|

Bear Scenario |

$230-$260 |

N/A |

Cautious. Assumes CPO delay, hyperscaler capex moderation, or macro-driven multiple compression that pulls COHR back toward cash-flow-based valuation levels. |

How to Trade Coherent (COHR) Stock Futures on BingX TradFi

As Coherent navigates a once-in-a-generation transition from pluggable to co-packaged optics alongside near-term headline risk from valuation digestion and quarterly earnings volatility, tactical traders can capitalize on its sharp bidirectional moves through the BingX TradFi platform.

- Access BingX TradFi: ign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

- Select Coherent (COHR): Search for and select the COHR-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the CPO revenue ramp, NVIDIA partnership, 6-inch indium phosphide capacity expansion, and OCS market growth will drive the stock toward street-high targets above $460. Select Open Short to capitalize on potential valuation compression ahead of August earnings, industrial segment underperformance, or any moderation in hyperscaler AI infrastructure spending guidance.

- Select Leverage and Margin Mode: Apply your preferred Isolated or Cross-Margin parameters alongside disciplined leverage ratios to maximize capital efficiency while controlling liquidation risk.

- Execute Strict Risk Protocols: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in gains and protect capital from sharp overnight moves tied to NVIDIA earnings updates, hyperscaler capex guidance revisions, or Jensen Huang keynote comments that routinely move the optical networking sector by double digits in a single session.

Top 5 Risks to Consider Before Investing in Coherent Stock

Coherent’s AI optics leadership is one of the strongest hardware infrastructure stories of 2026, but COHR also carries risks tied to CPO timing, valuation, competition, debt, and industrial demand.

- CPO revenue delay risk: Co-packaged optics is central to Coherent’s valuation premium, but meaningful revenue is still expected to ramp in the second half of 2026. Any delay from customer qualification, 6-inch wafer yield issues, or NVIDIA platform timing could push CPO revenue assumptions out by several quarters and trigger a de-rating.

- High valuation and macro sensitivity: COHR trades at a rich multiple, with a price-to-sales ratio above 12x and forward P/E above 49x. Its high beta and history of sharp drawdowns during market corrections mean any rate shock, AI capex slowdown, or risk-off rotation could pressure the stock quickly.

- Competition from integrated rivals: Intel, Broadcom, and Marvell are investing in optical integration and silicon photonics. Coherent’s vertical integration and NVIDIA partnership provide a strong near-term moat, but competing CPO architectures could limit pricing power or market share after 2027.

- Debt from legacy acquisitions: Coherent still carries significant debt from the II-VI and Finisar acquisitions. If AI optical revenue growth slows or free cash flow falls short, debt service could limit strategic flexibility and investment capacity.

- Industrial segment weakness: Industrial revenue declined in Q3 FY2026, partly due to divestitures and softer demand across semiconductor processing, consumer electronics, and medical markets. Continued weakness could weigh on headline revenue, margins, and the operating leverage expected by investors.

Final Thoughts: Is Coherent Stock a Buy in 2026?

As of June 2026, Coherent (COHR) is one of the clearest public-market plays on AI optical infrastructure. Record Q3 FY2026 revenue, 41% data center segment growth, NVIDIA’s $2 billion strategic investment, OCS backlog extending into 2028, and the expected CPO revenue ramp all point to a company that has moved beyond cyclical photonics and become a key supplier in the AI hardware stack.

The risk is that much of this optimism is already priced in. COHR now trades above the average analyst consensus target, so future upside depends on continued earnings upgrades, CPO revenue progress, margin expansion, and stronger free cash flow. For active traders, COHR futures on BingX TradFi offer a high-volatility way to trade both directions around these catalysts; for longer-term investors, the core question is whether CPO and OCS revenue can grow fast enough to justify a valuation that is already ambitious by AI infrastructure standards.

Related Reading

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Lumentum Stock Forecast 2026: Can AI Optics Boom, AI Data Center Supercycle Drive LITE Above $1,200?