As the number ofBitcoin (BTC) investors in Taiwan continues to grow, tax reporting has gradually become a topic of increasing concern. Many investors often get stuck on several issues when actually facing tax filing: whether they need to report, how to calculate trading gains and losses, and what impact the differences between various calculation methods will have. Since Taiwan has not yet established special laws for cryptocurrencies, relevant regulations are mainly extended applications of existing income tax systems, requiring many people to spend time understanding and organizing on their own.

As of 2026, according to the Ministry of Finance's interpretation, profits from Bitcoin trading are mostly regarded as property transaction income and included in individual comprehensive income tax calculations. With market development and the popularization of trading tools, investors' trading patterns have become more complex, extending from simple buying and selling to long-term holding, batch entry and exit, and even cross-platform trading, all of which affect the final calculation method of gains and losses. Therefore, compared to simply understanding the rules, how to organize trading records and establish a clear calculation method has become more practical and important.

This article will start from the actual usage scenarios of Taiwan BTC investors, explain the basic application methods of current tax regulations, and compare the differences between three common profit and loss calculation methods: FIFO, LIFO, and average cost. It will also demonstrate how to export trading records from BingX and organize gains and losses, introduce common tax tools, and organize practical problems and handling methods commonly encountered, helping you understand the overall reporting process more systematically.

Key Takeaways

- Taiwan BTC trading profits are currently mostly reported as property transaction income, calculated as "selling price - purchase cost - related fees." The difference is the income to be reported, which must be reported during the annual May tax season (the 2025 tax year reporting deadline is May 31, 2026).

- Withdrawals through Taiwan exchanges (such as MAX, BitoPro) and conversion to TWD usually constitute domestic income, subject to comprehensive income tax progressive rates; withdrawals through overseas exchanges (such as BingX) after currency exchange and remittance to Taiwan may constitute overseas income, with annual amounts under NT$1 million typically not needing to be included in basic income.

- Cost calculation methods (FIFO, LIFO, average cost) directly affect the final reported profit and loss amounts. Taiwan currently does not clearly specify which method must be used, but once selected, it is recommended to maintain consistency and keep complete trading records as evidence.

- Transaction history exported from BingX (including time, price, quantity, and fees) is the most important raw data for calculating gains and losses and reporting. It is recommended to download and organize regularly to avoid omissions or errors from one-time processing before tax season.

- If BTC trading shows losses, they can be reported as property transaction losses and qualify for special deductions; portions that cannot be fully deducted in the current year can be carried forward for use within the next 3 years, but relevant trading records must be attached as evidence.

Do You Need to Pay Tax on BTC in Taiwan? Rules and Legal Classification

Taiwan has not yet established special laws for cryptocurrencies, and Bitcoin (BTC) is considered virtual currency in regulatory terms. In tax practice, the Ministry of Finance's interpretation is that profits generated by individuals through buying and selling BTC are usually recognized as property transaction income under current income tax law and included in comprehensive income tax calculations. This means that cryptocurrency taxation is not an independent system but an extension of existing tax law applications.

In practice, whether reporting is required is usually related to whether trading generates realized gains. When BTC is sold and converted to fiat currency (such as TWD or foreign currency), it is easier to correspond to income calculations; if completed through Taiwan exchanges, it is usually regarded as domestic income; if involving overseas exchanges, it may further involve overseas income determination. Different trading and capital flow scenarios affect the final reporting method and applicable rules.

In understanding, there are some common concepts that need clarification. For example, "no need to report under NT$500,000" actually refers to the threshold for bank reporting mechanisms, which is different from tax reporting obligations; regarding whether holding or crypto-to-crypto trading generates tax obligations, there is still room for discussion in different scenarios. Overall, as trading records and capital flows become clearer, establishing consistent recording and calculation methods will be an important foundation for understanding and handling related tax issues.

How to Calculate BTC Gains and Losses: FIFO, LIFO, and Average Cost Compared

When calculating BTC trading gains and losses, if you bought multiple BTCs at different times and prices, when selling part of them, you need to decide "which batch of purchased BTC was sold." This matching method is the cost calculation method. Different methods will calculate different cost bases, thereby affecting the reported profit and loss amounts. Taiwan has not yet clearly specified which method must be used for cryptocurrencies, so in practice, choosing a consistent and explainable calculation method is a more important principle.

- FIFO (First In, First Out): Assumes that the earliest purchased BTC is sold first. If you established early positions when prices were lower, FIFO will prioritize matching these lower-cost positions, usually calculating higher profit amounts when prices rise. The advantage of this method is its intuitive logic, consistent with actual trading time sequence, making it easier to understand and explain when organizing trading records or reconciling accounts.

- LIFO (Last In, Last Out): Assumes that the most recently purchased BTC is sold first. If recent purchase prices are higher, LIFO will prioritize matching higher-cost positions, making the calculated profit amounts relatively lower. This method is closer to current market costs in some scenarios, but requires more precise record matching in accounting, with relatively fewer practical usage scenarios and requiring more attention to consistency.

- Average Cost Method: Adds up all purchase costs, divides by total holdings to get the average cost per BTC, and uses this as the calculation basis when selling. This method is simple to calculate and suitable for long-term batch purchasing scenarios, without needing to track sources individually, but the disadvantage is lack of flexibility and inability to reflect cost differences at different time points.

To illustrate the differences between the three methods with specific numbers: suppose you bought 0.1 BTC at three time points with costs of NT$500,000, NT$700,000, and NT$900,000 respectively (total 0.3 BTC, total cost NT$2.1 million), and now sell 0.1 BTC for NT$1 million. Under FIFO, the cost is NT$500,000 with a profit of NT$500,000; under LIFO, the cost is NT$900,000 with a profit of NT$100,000; under average cost method, each BTC costs NT$700,000 (NT$2.1 million ÷ 3) with a profit of NT$300,000. The taxable income differences between the three methods are significant. In BTC's long-term uptrend, LIFO or average cost method are usually more favorable for investors, but when using them, you should confirm Taiwan tax authorities' acceptance and consistently use the same method throughout the year.

|

Calculation Method |

Logic |

Taxable Profit in Rising Markets |

Calculation Difficulty |

Taiwan Application Recommendation |

Trading Scenario (Buy + Sell) |

Cost |

P&L |

|

FIFO (First In, First Out) |

First bought, first sold |

High (Early low costs) |

Low |

Clear records, easy to explain, but tax burden may be higher |

Three BTC purchases 0.1 BTC @ NT$500K 0.1 BTC @ NT$700K 0.1 BTC @ NT$900K (Total 0.3 BTC, total cost NT$2.1M) Sale: 0.1 BTC @ NT$1M |

NT$500K |

+NT$500K |

|

LIFO (Last In, First Out) |

Last bought, first sold |

Low (Recent high costs) |

Medium |

Taiwan recognition unclear, need confirmation before use |

NT$900K |

+NT$100K |

|

|

Average Cost Method |

All costs averaged |

Medium |

Low to Medium |

Suitable for dollar-cost averaging, intuitive calculation |

NT$700K |

+NT$300K |

How to Distinguish Domestic vs. Overseas Income: Based on Withdrawal Method

Bitcoin taxation determination is the same as other cryptocurrencies, classified as domestic or overseas income based on the "withdrawal platform." The tax systems applicable to both differ significantly: domestic income is included in comprehensive income tax under progressive rates, while overseas income applies to the alternative minimum tax system with relatively lenient exemptions. For BTC investors, choosing withdrawal channels is essentially part of tax planning.

1. Domestic Income: Withdraw via Taiwan Exchanges

Using Taiwan compliant exchanges like MAX and BitoPro to convert BTC to TWD and transfer to personal TWD bank accounts, these profits are considered "domestic income" and subject to individual comprehensive income tax regulations. Taiwan compliant exchanges follow real-name systems and anti-money laundering laws with complete trading records, allowing the National Taxation Bureau to access specific individuals' trading data under Article 30 of the Tax Collection Act. Domestic income calculation method:

Domestic Property Transaction Income = BTC Sale Amount − Purchase Cost − Trading Fees

The calculated income is included in annual individual comprehensive income total and taxed at progressive rates (5% to 40%). For BTC investors with smaller profit amounts, the lower-end tax rate thresholds for domestic income are relatively favorable; however, for high-income groups, the 40% progressive rate ceiling is significantly higher than the minimum tax system for overseas income.

2. Overseas Income: Transfer Funds Back to Taiwan from Foreign Platforms

If using overseas exchanges to trade BTC and converting profits to USD or stablecoins before wire transferring to Taiwan foreign currency bank accounts, this income is considered "overseas income." Overseas income is not included in comprehensive income tax but applies to the Income Basic Tax Act. When remitting funds, banks will require specifying remittance nature; it's recommended to declare "268 Sale of Foreign Virtual Assets" for easy classification as overseas income during tax filing.

Overseas income exemptions are relatively lenient. Annual overseas income totaling less than NT$1 million is exempt from reporting; over NT$1 million requires reporting alternative minimum tax. Basic income amount minus NT$7.5 million (applicable for 2026) is calculated at 20% as basic tax amount. If basic tax amount exceeds comprehensive income tax amount, the difference must be paid; if comprehensive tax amount is greater than or equal to basic tax amount, no basic tax is payable. Note that basic income amount includes not only overseas income but also specific insurance benefits, securities transaction income, etc., which should be considered together when calculating exemption space.

Extended Reading:Complete Comparison of Taiwan Cryptocurrency Fiat On-Ramps and Off-Ramps: Which Platform Has Cheapest Deposits and Fastest Withdrawals? (2026)

How to Choose a BTC Tax Tool for Taiwan Users

For Taiwan BTC investors with more frequent transactions or operations across multiple platforms, manually organizing profit and loss data usually involves considerable workload. The following tools can help integrate trading records and calculate gains and losses.

Most tools are international services with limited support for Taiwan's tax system, mainly used for calculating profit and loss figures. For actual reporting, you still need to reorganize according to Taiwan's format. Additionally, current mainstream tools are mostly in English interfaces without complete Traditional Chinese support, which may require some adaptation during use.

- Koinly:Supports most mainstream exchanges and wallets, provides API and CSV import methods, can automatically organize trading records and categorize them as trading, transfers, fees, etc., reducing manual organization burden. Supports FIFO, LIFO, and average cost methods, and can generate profit and loss reports and tax summaries, suitable for users with more transactions or cross-platform operations.

- CoinTracker:Focuses on automatic synchronization and portfolio tracking, supports API connections with most exchanges, and can import data via CSV. The system automatically calculates holding costs and realized gains and losses, supports FIFO and LIFO, suitable for users with relatively simple trading records or who want to quickly grasp overall asset status. The free version has transaction count limits, requiring plan upgrades as trading volume increases.

- Blockpit (formerly Accointing):Provides trading record integration, profit and loss calculation, and tax report functions, supports FIFO and average cost methods. The former Accointing has been merged into Blockpit, with continued and integrated functionality, suitable for medium trading volume scenarios. Output is still mainly based on international tax systems, usually requiring reorganization for Taiwan reporting.

- Excel/Google Sheets:Without relying on third-party tools, you can directly import exchange CSVs, create your own fields and calculation logic, and organize data completely according to Taiwan reporting requirements. Suitable for users with fewer transactions or who want to control the complete calculation process, with advantages in format control and flexibility.

For Taiwan general investors with fewer transactions (less than 50 transactions annually), using Excel or Google Sheets for self-organization is usually more practical than paying for third-party tool subscriptions, as you can organize data completely according to Taiwan reporting format requirements without needing to convert tool outputs. Advanced users with high trading volumes or cross-chain operations can consider tools like Koinly to reduce organization workload, but still need to verify calculation results themselves.

BTC Tax Tool Comparison: Taiwan-Friendly Tools with Chinese Interface

|

Tool |

Traditional Chinese Interface |

Taiwan Tax Format |

BingX Import Support |

Supported Calculation Methods |

Cost |

|

Koinly |

No |

Partial Support (Can generate P&L reports) |

Manual CSV upload required |

FIFO, LIFO, Average Cost |

Free basic version, paid plans from ~$49 USD/year |

|

CoinTracker |

No |

Partial Support |

Manual CSV upload required |

FIFO, LIFO |

Free 25 transactions, paid plans from ~$59 USD/year |

|

Blockpit |

No |

Partial Support |

Manual CSV upload required |

FIFO, Average Cost |

Free basic version, paid plans from ~$79 USD/year |

|

Excel/Google Sheets |

Yes |

Full Flexibility (Self-designed) |

Direct CSV import |

Customizable (FIFO, LIFO, Average Cost, etc.) |

Free |

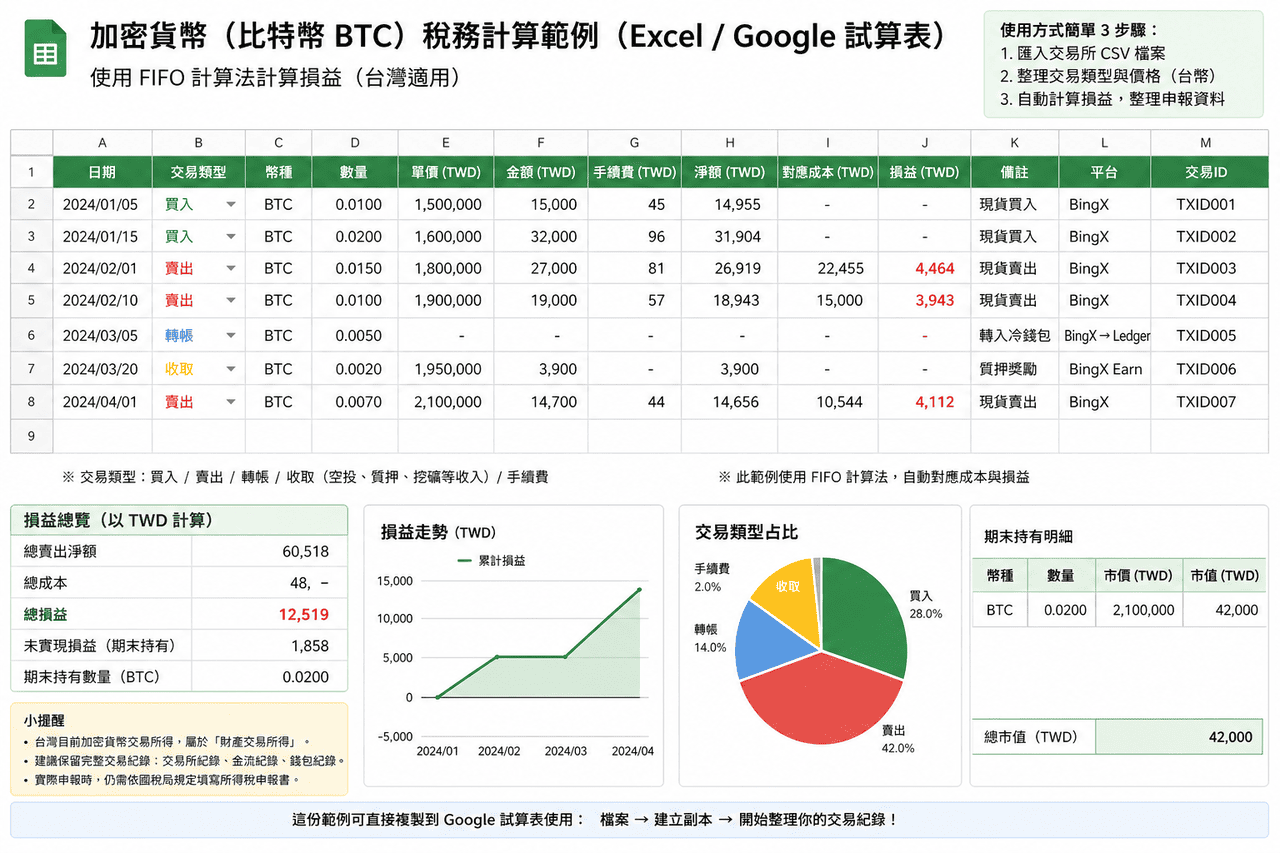

How to Export BTC Trade History from BingX for Tax Filing

For most Taiwan BTC investors, organizing profit and loss statements independently is the most direct reporting method, without needing to rely on third-party tools. As long as you have complete BingX trading records, you can calculate reportable property transaction income following these steps.

Step One: Download Complete Transaction Records from BingX

Log into BingX, go to "Assets" → "Trade History" or "Order History," select the required reporting year range (e.g., January 1, 2025 to December 31, 2025), and export as CSV format. After downloading, confirm records include the following fields: transaction time, trading pair (BTC/USDT), buy/sell direction, filled quantity, average filled price, and fees. If using both spot and futures trading simultaneously, download spot transaction records and futures transaction records separately, as these two types of profit and loss calculations differ slightly and should be organized separately.

Step Two: Convert USDT Quotes to TWD

Taiwan tax reporting requires TWD calculations for gains and losses. If your trading is priced in USDT, you need to find the USDT/TWD exchange rate for each transaction day and convert USDT amounts to TWD. Exchange rates announced daily by Taiwan banks or the Central Bank can serve as conversion basis. It's recommended to use "transaction day" bank spot buying rates for cost conversion and "transaction day" bank spot selling rates for sale income conversion, maintaining consistent conversion standards and recording exchange rates and sources used for each conversion.

Step Three: Organize Profit and Loss Calculation Table

Create a profit and loss calculation table in Excel or Google Sheets, recommended to include the following fields: transaction date, buy or sell, BTC quantity, TWD cost (when buying) or TWD income (when selling), fees (TWD), individual profit and loss. Each "sell" transaction's profit and loss calculation method is: TWD income − corresponding cost − fees = individual profit and loss. Corresponding cost calculation depends on your chosen method (FIFO or average cost).

Using average cost method as example, suppose you performed the following operations in 2025: bought 0.5 BTC in January for NT$1.5 million, bought another 0.3 BTC in June for NT$1.05 million, sold 0.4 BTC in October for NT$1.6 million, with total fees of NT$12,000. Average cost calculation: (NT$1.5M + NT$1.05M) ÷ (0.5 + 0.3) = approximately NT$3.1875M ÷ 0.8 = approximately NT$3.98M per BTC (this example uses simplified proportions). Corresponding cost for 0.4 BTC = NT$3.98M × 0.4 = approximately NT$1.275M. Individual profit and loss = NT$1.6M − NT$1.275M − NT$12K = NT$313K (reportable property transaction income).

Step Four: Sum Annual Profit and Loss and Confirm Reporting Figures

Sum individual profit and loss from all sell transactions throughout the year to get annual BTC property transaction income total (or loss total). If positive, this amount will be included in the current year's individual comprehensive income tax property transaction income field. If negative (loss), you can report property transaction loss special deductions and attach BingX transaction records as supporting documents; losses that cannot be fully deducted in the current year can be carried forward for use within the next 3 years.

Step Five: Enter Profit and Loss into Comprehensive Income Tax Return

Go to the Ministry of Finance's Electronic Filing and Payment Service website (tax.nat.gov.tw) and enter the calculated annual profit and loss figure in the "Property Transaction Income" field of the comprehensive income tax return. If domestic income (withdrawals through MAX, BitoPro), enter directly in the "Property Transaction Income" field. If overseas income (currency exchange through BingX and other overseas platforms then wire transfer to Taiwan), enter in relevant "Overseas Income" fields and confirm whether it exceeds the NT$1 million inclusion threshold. When reporting, it's recommended to prepare BingX transaction record CSVs and TWD conversion calculation processes simultaneously for explanation during National Taxation Bureau audits.

Common BTC Tax Mistakes and Compliance Tips

Based on Taiwan tax practice, the following are several common issues BTC investors encounter when reporting, along with corresponding organization methods:

- Some people assume withdrawals under NT$500,000 don't need reporting. NT$500,000 is actually the bank reporting threshold under anti-money laundering measures, unrelated to tax reporting obligations. As long as trading through real-name exchanges generates transactions and profits, it falls under reportable scope, regardless of amount size affecting reporting obligations.

- Not keeping records related to purchase costs. Taiwan uses "selling price minus cost" to calculate property transaction income; without cost proof, estimation methods may be used, which is disadvantageous for higher-cost investment scenarios. It's recommended to regularly download and save transaction records from BingX, avoiding data gaps from organizing only before tax season.

- Ignoring fee inclusion. Property transaction income allows deduction of directly related transaction fees, such as trading fees or withdrawal fees. If not included in calculations, taxable income will be inflated. When organizing gains and losses, corresponding fees for each transaction should be recorded together.

- Using different cost calculation methods within the same year. If some transactions use FIFO and others use average cost, it increases explanation difficulty and may affect reporting consistency. It's usually recommended to choose one method at the beginning of the year and maintain consistency throughout.

- Not reporting losses in the current year. Some investors don't report in loss years, preventing future use for offsetting gains. Under current regulations, property transaction losses must be reported in the current year to be deductible in future periods.

- Confusion between domestic and overseas income classification. Withdrawals through local exchanges (like MAX, BitoPro) constitute domestic income, while currency exchange through overseas platforms (like BingX) constitutes overseas income, applying different reporting fields and thresholds. If having different sources simultaneously, calculate separately and report in different fields.

Important Notes

- This article's content is organized based on Taiwan Ministry of Finance's current position and tax law framework, for reference only, and does not constitute tax or legal advice. Cryptocurrency-related regulations are still continuously adjusting, with the Virtual Asset Management Special Act draft submitted to the Executive Yuan for review in June 2025. After formal passage, reporting methods may change, so it's recommended to continue monitoring Ministry of Finance announcements.

- Individual tax situations vary based on income structure, withdrawal paths, and holding periods, particularly domestic versus overseas income determination, which still has interpretation space in some scenarios. For larger transaction amounts or more complex structures, consider consulting accountants or lawyers familiar with crypto assets.

- BingX transaction records are important raw data for reporting; it's recommended to regularly (e.g., quarterly) download and backup from the backend rather than organizing everything before tax season, to reduce risks of data omission or inability to access records.

- If using multiple exchanges simultaneously (like BingX with MAX or BitoPro), it's recommended to download trading records from each platform separately and distinguish domestic versus overseas sources in profit and loss statements, avoiding mixed calculations.

- Cryptocurrency taxation in Taiwan operates on a self-reporting system, with related audit mechanisms gradually being established. Whether receiving notifications has no direct relation to reporting obligations; in practice, proactive organization and reporting remain the standard.

Conclusion: A Practical Guide to BTC Tax Filing in Taiwan

Taiwan's BTC tax reporting environment is gradually moving from previously unclear conditions toward clearer regulations. The Ministry of Finance has classified cryptocurrency profits as property transaction income, with related audit mechanisms gradually being established, making reporting importance clearer than before. For investors, the more practical approach is establishing daily record-keeping habits, such as regularly downloading BingX trading records, choosing and maintaining consistent cost calculation methods, completely recording each transaction and fees, and allocating time before tax season to organize data, reducing subsequent processing burden. For larger trading scales or more complex structures, consider seeking professional assistance from those familiar with crypto asset taxation, incorporating related planning into overall investment arrangements rather than concentrating on processing only before tax season.

Related Reading

- Taiwan Bitcoin Short-Term Trading Platform Recommendations: Complete Comparison of Fees and Technical Tools (2026)

- How to Conduct Bitcoin Arbitrage in Taiwan? 4 Strategy Comparisons and Complete BingX Operation Tutorial (2026)

- Which Taiwan Exchange is Best for Large Bitcoin Trading? Complete Platform Fee and Liquidity Comparison Recommendations (2026)

- 2026 Cryptocurrency Exchange Price APIs and Data Tools Recommendations: Top 5 Developer-Preferred Platforms

- Complete Taiwan Cryptocurrency Futures Trading Platform Comparison Recommendations (2026): Fees, Liquidity and Security Comparison

- Complete Comparison of Taiwan Cryptocurrency Fiat On-Ramps and Off-Ramps: Which Platform Has Cheapest Deposits and Fastest Withdrawals? (2026)