Artificial intelligence (AI) has completed its transition from software experimentation to massive physical infrastructure deployment. By mid-2026, AI is no longer treated as a speculative investment theme, but rather as the primary driver of global corporate capital expenditure. Leading hyperscalers and technology conglomerates are projected to spend nearly $700 billion in 2026 alone on AI data centers, high-speed networking, advanced cooling systems, and specialized silicon. At the absolute core of this technological supercycle sit the chip design firms, semiconductor equipment manufacturers, and advanced foundries that fabricate the physical backbone of the global AI economy.

Simultaneously, global financial markets are experiencing a structural shift toward efficiency and accessibility. Tokenized stocks, blockchain-based digital assets that track real-world equities 1:1 using stablecoins, are bridging the gap between traditional finance (TradFi) and decentralized finance (DeFi). In addition to tokenized stocks, platforms like BingX TradFi let users can trade leading US stock futures with USDT, so global investors can gain fractional, 24/7 exposure to premier U.S.-listed semiconductor leaders without needing traditional brokerage accounts. This setup allows capital to flow directly into the most critical infrastructure plays of the 2026 AI Inference Pivot using crypto-native rails.

AI Infrastructure Market Overview in 2026: Key Structural Trends

The AI hardware supply chain has evolved rapidly into mid-2026, shifting away from the broad general-purpose GPU shortages of 2024 and 2025 into a highly complex, capital-intensive hardware cycle. Fueled by a colossal $700 billion infrastructure spending wave from cloud hyperscalers this year alone, the semiconductor landscape is defined by four highly localized, data-driven structural trends:

1. The AI Inference Pivot: Shifting to Agentic Architecture

While training frontier large language models (LLMs) remains a foundational capital sink, 2026 marks the official inflection point where inference workloads surpass training workloads in data center capacity. The industry focus has shifted to scaling agentic AI, multi-step reasoning systems, and autonomous enterprise architectures. This creates a fierce demand for hardware that lowers the total cost per token.

NVIDIA’s next-generation Vera Rubin platform shipping H2 2026 highlights this structural shift, promising up to a 10x reduction in inference cost per token and a massive 10x performance-per-watt efficiency gain over the Blackwell series, cementing power-per-watt efficiency as the primary metric for data center operators.

2. The 2026 Memory Crunch: HBM Captures the Value Chain

A logic processor is only as effective as its data-movement architecture. As AI architectures transition into complex autonomous agent systems, the structural bottleneck has moved from raw GPU compute capabilities to high-speed data transfer. High-Bandwidth Memory (HBM) has transitioned from a cyclical commodity into a high-margin, mission-critical technology play.

The Total Addressable Market (TAM) for HBM is projected to expand more than threefold, surging from $35 billion in 2025 to over $100 billion by 2028. This insatiable appetite has left top-tier memory suppliers like Micron with 100% of their HBM production capacity fully pre-sold through the end of 2026, allowing hardware makers to command premium pricing.

3. Advanced Packaging: The Rise of Mainstream Chiplet Moats

The historical reliance on traditional monolithic die shrinks is hitting physical boundaries. In 2026, the industry has widely adopted heterogeneous chiplet-based designs, which enable engineers to mix compute, memory, and I/O components from different process nodes onto a single substrate. Physical packaging is now a bigger competitive differentiator than raw process node shrinks.

Advanced packaging methodologies like CoWoS (Chip-on-Wafer-on-Substrate), 3D stacking, and hybrid bonding have become critical supply bottlenecks. This shift directly benefits dominant fabricators; for instance, TSMC has leveraged its packaging monopoly to upgrade the global semiconductor market forecast to $1.5 trillion by 2030, driven by the sheer volume of chiplet integration.

4. Custom Silicon Acceleration: Hyperscalers Unbundle the GPU

To aggressively rein in massive power budgets and lower dependency on third-party design firms, cloud providers are rapidly scaling custom, in-house application-specific integrated circuits (ASICs). Bypassing general-purpose GPUs for specialized workloads is altering data center deployment ratios.

Custom ASICs tailored to specific workloads are showing distinct cost advantages over flexible GPUs when handling targeted inference algorithms. This paradigm shift underpins Broadcom’s projected custom AI chip business target of $100 billion in sales next year, fueled by hyperscalers optimizing their internal tech stacks to bypass traditional chip supply chain markups.

What Are the 10 Best AI Infrastructure Stocks to Watch in 2026?

The following list highlights the top 10 AI infrastructure chip design, manufacturing, and equipment companies driving the hardware cycle into the second half of 2026. Each company represents a critical layer of the computing stack, available to global markets via traditional equities or tokenized spot and futures pairs.

1. NVIDIA (NVDA)

- 2026 Valuation Benchmark: $5.4 Trillion Market Cap

- Core Role: Dominant Chip Designer & Software Ecosystem Moat

NVIDIA remains the foundational pillar of the global AI infrastructure stack. The company designs the leading-edge graphics processing units (GPUs) that handle the vast majority of enterprise training and inference workloads. Capitalizing on the blowout success of its Hopper and Blackwell platforms, NVIDIA is preparing for the commercial rollout of its next-generation Vera Rubin platform in H2 2026. The Rubin architecture aims to address critical power constraints by delivering a claimed 10x performance-per-watt improvement while lowering inference token costs.

Crucially, NVIDIA’s primary competitive advantage is not merely hardware, but its proprietary CUDA software ecosystem, which millions of developers use globally to optimize AI workloads. Ahead of its Q1 earnings on May 20, 2026, market expectations remain high, supported by an expanding inference backlog and strategic data center energy partnerships.

On-chain investors track this price action directly via fully backed NVIDIA's tokenized stocks like NVDAON (Ondo Finance) and NVDAX Solana-based xStock.

2. Broadcom (AVGO)

- Core Role: Custom Chip Design and High-Speed Data Center Fabrics

Broadcom excels at the intersection of custom silicon and complex networking infrastructure. Rather than competing directly in general-purpose GPUs, Broadcom partners with mega-cap hyperscalers, such as Google and Meta, to co-design bespoke AI accelerators (ASICs). These tailored chips are underperforming relative to GPUs on highly generalized tasks but offer significant cost and power efficiencies when running specialized, repetitive workloads at hyperscale.

Financially, Broadcom started 2026 with strong momentum, posting a 29% year-over-year revenue increase in its Q1 results. Driven by robust enterprise demand for its high-speed networking chips and custom silicon divisions, Wall Street analysts have steadily upgraded their price targets, noting Broadcom's visibility into a potential $100 billion custom AI chip sales runway.

3. Advanced Micro Devices (AMD)

- Core Role: Fabless GPU and CPU Design

AMD serves as the primary market alternative to NVIDIA’s data center dominance. The company designs competitive AI accelerators, led by its MI300 and MI350 series chips, alongside high-performance EPYC data center CPUs. By capturing market share in inference-heavy and cost-sensitive enterprise deployments, AMD delivered a strong Q1 2026 earnings beat that helped spark a broader semiconductor rally. With verified cloud architecture deployments across major entities like OpenAI and Meta, leadership has expressed high confidence in scaling AI-specific revenues into tens of billions by 2027.

4. Micron Technology (MU)

- Core Role: High-Bandwidth Memory (HBM) Production

Micron Technology has transformed from a cyclical commodity provider into a highly strategic bottleneck asset within the AI value chain. Micron manufactures high-speed DRAM, NAND flash, and critical HBM solutions necessary to feed data to advanced AI processors without causing system latency. Due to the severe 2026 Memory Crunch, Micron’s entire HBM production capacity is fully pre-sold through the end of the year. Despite short-term equity price volatility from profit-taking cycles, Wall Street consensus projects massive forward revenue growth fueled by multi-billion-dollar expansions of physical fabrication facilities in the United States.

5. TSMC (TSM)

- 2026 Valuation Benchmark: ~$2.1 Trillion Market Cap

- Core Role: Pure-Play Semiconductor Fabrication

Taiwan Semiconductor Manufacturing Company (TSMC) is the world's largest dedicated contract chip foundry, physically fabricating the advanced silicon designed by NVIDIA, AMD, Apple, and Broadcom. TSMC occupies a near-monopoly position in leading-edge node manufacturing and advanced packaging (CoWoS). Highlighting sustained AI acceleration demand, TSMC raised its full-year 2026 revenue growth outlook to over 30% while projecting the global semiconductor market to hit $1.5 trillion by 2030. To mitigate geopolitical risk and meet U.S. reshoring requirements under the CHIPS Act, TSMC is aggressively executing a massive capital investment strategy to construct up to six advanced fabrication facilities in Arizona.

6. ASML Holding (ASML)

- Core Role: Extreme Ultraviolet (EUV) Equipment Manufacturing

Headquartered in the Netherlands, ASML is the sole global manufacturer of the Extreme Ultraviolet (EUV) and High-NA EUV lithography machines required to print advanced circuitry onto silicon wafers. Without ASML's equipment, modern 3nm, 2nm, and sub-2nm AI processors cannot be manufactured. Driven by global fab build-outs across the U.S., Europe, and Asia, ASML raised its 2026 sales guidance to a robust €36–40 billion range. While navigate-to-watch geopolitical export restrictions to China remain a factor, structural structural demands for localized semiconductor infrastructure provide a clear long-term tailwind.

7. Arm Holdings (ARM)

- Core Role: Energy-Efficient Processor Architecture Licensing

Arm Holdings provides the foundational, ultra-low-power intellectual property (IP) architecture upon which the vast majority of modern global processors are built. As data centers grapple with extreme electricity consumption and thermal limitations, Arm’s energy-efficient architectural designs are increasingly licensed by hyperscalers building custom data center CPUs, such as Amazon’s Graviton or Google’s Axion. Arm posted record results for its most recent fiscal year, driven by higher royalty rates for AI-optimized architectures, comfortably offsetting ongoing regulatory scrutiny over global licensing practices.

8. Intel (INTC)

- Core Role: Integrated Device Manufacturing & Domestic Foundry

Intel operates a distinct Integrated Device Manufacturer (IDM) model, meaning it both designs internal chips and manages physical manufacturing facilities. Under a heavily monitored turnaround plan, Intel is positioning itself as the primary domestic, secure manufacturing alternative to TSMC on U.S. soil. The company's 18A (1.8nm) process node has entered high-volume production, and its next-generation 14A node incorporates High-NA EUV lithography designed explicitly for external custom chip clients. Supported by direct U.S. government defense contracts and billions in CHIPS Act allocations, Intel’s stock has experienced sharp institutional accumulation following a multi-year structural breakout.

9. Marvell Technology (MRVL)

- Core Role: Electro-Optics and Custom Data Center Silicon

Marvell Technology specializes in the high-speed data infrastructure and electro-optics required to connect thousands of individual GPUs into unified data center clusters. As physical distance and copper cabling encounter natural bandwidth constraints, Marvell’s optical interconnect solutions allow rapid data transfer via light vectors, directly minimizing cluster latency. Ahead of its Q1 FY2027 earnings in late May 2026, major investment banks have systematically raised Marvell’s target valuation, citing deep integration into NVIDIA's broader networking ecosystem and expanding electro-optics pipelines.

10. Alphabet (GOOGL)

- Core Role: Hyper-Scale Cloud Provider & Proprietary Silicon Design

Alphabet (Google) represents the intersection of custom chip design and massive cloud infrastructure delivery. As an early pioneer of specialized silicon, Google developed the Tensor Processing Unit (TPU) over a decade ago to accelerate machine learning workloads. Today, Google Cloud's surging growth is heavily supported by the internal deployment of its v5 and v6 TPU clusters alongside NVIDIA’s latest platforms, allowing enterprise customers to scale Gemini model implementations smoothly. Backed by a massive $364 billion cloud infrastructure backlog, Google is executing a projected $180+ billion capital expenditure plan in 2026 to further secure its global AI cloud and data center footprint.

Comparison of Leading AI Infrastructure Players

|

Ticker |

Primary AI Category |

Core Structural Advantage / Product |

2026 Financial Catalysts & Status |

|

NVDA |

Fabless Chip Design |

Hopper/Blackwell/Rubin GPUs; CUDA Platform |

Q1 Earnings May 20; Premium valuation leader |

|

AVGO |

Custom Silicon / ASICs |

Bespoke client processors; high-speed networking |

Q1 Revenue up 29% YoY; Custom business targets $100B |

|

AMD |

Fabless Chip Design |

MI300/MI350 Accelerators; EPYC CPUs |

Q1 Beat; Record stock highs on secular momentum |

|

MU |

Advanced Memory |

High-Bandwidth Memory (HBM4/HBM3e) |

2026 Capacity fully sold out; cyclical pricing tailwind |

|

TSM |

Manufacturing Foundry |

Global leading-edge fabrication monopoly (CoWoS) |

Projected 2026 growth >30%; massive Arizona expansion |

|

ARM |

Semiconductor IP |

Energy-efficient architecture blueprints |

Record fiscal revenue; high royalties from AI server cores |

|

ASML |

Fab Equipment |

Extreme Ultraviolet (EUV) Lithography machines |

Upgraded 2026 sales guidance to €36–40B |

|

INTC |

IDM / Foundry Service |

18A/14A U.S. Fabs; EMIB Advanced Packaging |

Major technical turnaround; extensive CHIPS Act backing |

|

MRVL |

Networking Silicon |

Optical interconnects; electro-optics infrastructure |

Price targets upgraded ahead of late-May earnings |

|

GOOGL |

Hyperscaler Cloud / ASIC |

Tensor Processing Units (TPUs); Google Cloud |

Cloud backlog expanding; aggressive $180B+ CapEx plan |

How to Trade AI Infrastructure Stocks on BingX

BingX provides a streamlined gateway to gain price exposure to the semiconductor and AI hardware ecosystem without traditional cross-border brokerage limitations or the need for a traditional brokerage account. Depending on your trading strategy, risk tolerance, and capital requirements, BingX offers two distinct paths to access these premier tech equities using crypto-native rails.

Trade Tokenized Stocks on BingX Spot

NVDAX/USDT tokenized stock on BingX spot market

For long-term investors looking for direct price tracking without leverage, the BingX Spot market offers fully backed tokenized equities issued via regulated asset frameworks like Backed Finance and Ondo Finance. These digital assets track real-world shares on a 1:1 economic basis using stablecoins.

Step 1: Account Set-Up and Security

Log into your BingX account. Complete the standard identity verification (KYC) required in your region and enable secure two-factor authentication, such as Google 2FA, to protect your assets.

Step 2: Fund Your Spot Wallet

Deposit USDT into your BingX account utilizing your preferred blockchain network, e.g., TRC-20, ERC-20, or Arbitrum. Review the minimum deposit requirements and network fees before confirming the transfer.

Step 3: Navigate to the Spot Market

Go to the BingX Spot trading interface and search for fully backed, non-leveraged tokenized stock pairs such as NVDAON/USDT (NVIDIA) or GOOGLON/USDT (Google).

Step 4: Leverage BingX AI Tools

Prior to order entry, tap the BingX AI Analyst tool embedded in the charting panel. This compiles instant, real-time market data, including automated support/resistance zones, moving averages, and immediate volatility indexes, to help refine your entry.

Step 5: Execute and Settle

Select your order type, e.g., Market Order for instant execution or Limit Order to specify a target price, enter your USDT investment amount, and confirm the trade. Your tokenized stock balances will populate your Spot wallet immediately upon execution.

Trade Stock Futures with USDT on BingX TradFi

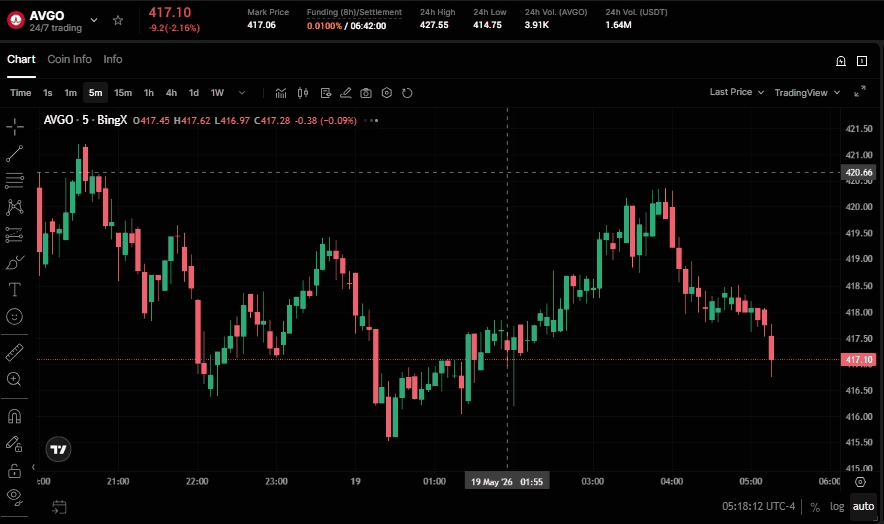

AVGO/USDT perpetual contract on BingX futures market

For active traders looking to capitalize on short-term market momentum, earnings volatility, or hedging strategies, the BingX TradFi platform allows users to trade leading U.S. stock futures with USDT. This setup utilizes USDT-settled perpetual contracts that mirror equity price movements, offering flexible trading mechanics without requiring you to hold the physical or tokenized asset.

Step 1: Access the BingX TradFi Interface

Log into your secure BingX account and navigate directly to the dedicated TradFi markets page or the Futures trading portal.

Step 2: Capital Allocation

Ensure your Futures account is funded by transferring USDT from your main Spot wallet. This capital will serve as your collateral and margin engine.

Step 3: Select Your Stock Futures Contract

Choose from a robust lineup of highly liquid, stock-linked perpetual contracts tracking key AI infrastructure leaders, such as NVDA-USDT, GOOGL-USDT, INTC-USDT, or AMD-USDT.

Step 4: Define Your Direction and Leverage

Unlike spot trading, BingX TradFi enables you to trade both sides of the market. Select Open Long if you project the stock price will rise, or Open Short to profit from downward price movements. Adjust your leverage parameters carefully according to your risk management plan.

Step 5: Execute and Manage Risk

Deploy the BingX AI trading assistant to analyze localized trend strength and liquidity depth. Enter your position size, establish strict Stop-Loss (SL) and Take-Profit (TP) orders to guard against market volatility, and execute your trade. Your open PnL will update in real time, settled dynamically in USDT.

Risks and Core Considerations When Trading AI Infrastructure Stocks

While the physical expansion of AI chips presents a clear secular growth runway, investors must balance their portfolios against specific operational risks:

- Valuation Compression and Hype Premium: Many semiconductor equities trade at high forward price-to-earnings (P/E) multiples due to structural market enthusiasm. Any unexpected reduction or slowdown in data center CapEx by cloud hyperscalers can result in rapid equity drawdowns.

- Structural Cyclicality: Hardware industries are historically subject to supply-and-demand imbalances. If memory or fabrication capacity expansion overcorrects and creates an oversupply, chip pricing power can erode quickly.

- Geopolitical Realities: Advanced chip manufacturing remains geographically concentrated. Export control policies, regional blockades, or friction in East Asia introduce persistent risk profiles to asset classes like TSMC and ASML.

- Lack of Shareholder Governance: Tokenized stocks function strictly as alternative access vehicles. They track economic price performance 1:1 but do not confer corporate voting rights, physical share delivery, or legal ownership privileges.

Final Thoughts: Should You Add AI Infrastructure Stocks to Your 2026 Portfolio?

The mid-2026 macroeconomic landscape underscores a clear division in the technology sector: while consumer-facing software monetization is still maturing, the physical infrastructure builders are generating substantial, verified revenues today. Diversifying capital across distinct layers of the computing stack, such as design pioneers like NVIDIA, advanced packaging monopolies like TSMC, and memory suppliers like Micron, provides a structured approach to capturing this hardware supercycle. Utilizing tokenized spot assets or stock futures via BingX TradFi allows global market participants to execute these macro-driven equity theses efficiently using unified, crypto-native rails.

However, allocating capital to this high-growth sector requires strict risk management. Semiconductor and AI infrastructure assets are inherently highly cyclical, trade at premium valuations, and remain sensitive to sudden shifts in hyperscaler spending, geopolitical supply chain disruptions, and shifting regulatory frameworks. Additionally, trading stock futures via leverage carries significant liquidation risk, while tokenized spot assets do not confer shareholder voting rights or dividend privileges. Market participants should carefully assess their individual risk tolerance, implement rigorous stop-loss parameters, and treat these volatile tech exposures as a specialized component of a broader, well-diversified portfolio.

Related Reading

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Roundhill Memory ETF (DRAM) Forecast 2026: $1.5B AI Supercycle or 'RAMmageddon' Trap?

- Direxion Daily SOXL ETF Forecast 2026: $200 Moonshot or Michael Burry’s Return to Earth Trap?

- S&P 500 Forecast 2026: 7,600 Bull Run or a 6,000 Energy-Driven Crash?

- Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?

- Dow Jones (DJIA) Forecast 2026: The 50,000 Milestone vs. The Hormuz Hedge