Alphabet (GOOGL) has entered 2026 at a historic inflection point, trading near $307 as it solidifies its position as a leading artificial intelligence (AI) and cloud powerhouse. Google is one of the world’s leading Big Tech firms, alongside companies like Apple, Microsoft, Amazon, Meta Platforms, and NVIDIA, Alphabet Inc. continues to dominate global technology markets. With Gemini reaching over 750 million monthly active users and Google Cloud surging to an annual run rate exceeding $70 billion, Alphabet is transitioning from an advertising-dominated giant to a full-stack AI leader. Explore the institutional price targets, the AI roadmap, and whether GOOGL is a buy in 2026. In early 2026, Alphabet (GOOGL) decoupled from traditional digital advertising cycles. While Search and YouTube remain foundational, the Gemini rollout and Google Cloud acceleration have fueled unprecedented growth in AI-driven segments. As of March 2026, the narrative centers on AI infrastructure scale, Gemini adoption, and enterprise cloud demand.

Alphabet enters 2026 with massive structural tailwinds. CEO Sundar Pichai has emphasized Gemini's role in transforming products and services, projecting continued AI momentum. With 2026 capital expenditure (CapEx) guidance of $175 billion to $185 billion to expand compute capacity, 2026 shapes up as a pivotal year. This guide breaks down the Alphabet stock price prediction for 2026 using data from analysts and consensus estimates. You will also discover how to gain exposure to Alphabet (GOOGL) stock futures through BingX TradFi and via Alphabet tokenized stocks GOOGLx and GOOGLON on the BingX spot market.

Read more: What Is Alphabet Google Tokenized Stock GOOGLX and GOOGLON, and How to Buy?

Key Highlights: Top 5 Things for Alphabet Investors to Know in 2026

1. Gemini Acceleration: The Gemini App has grown to over 750 million monthly active users, with first-party models processing over 10 billion tokens per minute via direct API use.

2. Cloud Supercycle: Google Cloud reached an annual run rate of over $70 billion, with Q4 2025 revenue up 48% to $17.7 billion.

3. Revenue Momentum: Total revenue hit $402.8 billion in 2025, up 15%, with Q4 at $113.8 billion, up 18%.

4. Polarized Targets: Analyst forecasts for 2026 range from bearish lows around $220 to bullish highs of $420 to $450.

5. Valuation Debate: Forward multiples reflect AI premium, but margin strength and CapEx support re-rating as profitability scales.

Read more: Strategy (MSTR) Stock Outlook 2026: Can MSTR Cross $700 on Bitcoin Treasury Strategy?

What Is Alphabet (GOOGL)?

Alphabet is a leading technology company specializing in search, advertising, cloud computing, and artificial intelligence. Globally recognized by Google Search, YouTube, and Android, in 2026 it is increasingly viewed as an AI and cloud leader. Its core value lies in Gemini models and Google Cloud infrastructure, enabling rapid AI deployment across consumer and enterprise applications. Unlike traditional tech firms, Alphabet's ecosystem includes custom TPUs, massive data centers, and integrated services serving billions of users and enterprises.

Alphabet's Strategic Evolution (1998-2026): From Search Pioneer to AI Leader

Founded in 1998, Alphabet's history features transformative milestones. The Google Search launch (1998) revolutionized information access, followed by YouTube acquisition (2006) and Android dominance. The 2015 restructuring created Alphabet, enabling moonshots. Gemini's 2023 launch ignited AI growth, pushing cloud and consumer adoption. From search roots to AI dominance, Alphabet has consistently delivered innovation at scale.

Alphabet's Key Growth Phases Over the Years: From Search to AI Dominance

Alphabet's journey spans distinct eras:

• The Search Phase (1998-2015): Building dominant advertising and consumer platforms.

• The Diversification Era (2015-2023): Expanding cloud, hardware, and moonshots post-restructuring.

• The AI Dominance Era (2024+): Gemini fueling hyper-growth in cloud and products.

Alphabet (GOOGL) 2025 Performance Overview: The AI Acceleration Year

In 2025, Alphabet accelerated dramatically as AI adoption surged across consumer and enterprise markets. While Search and YouTube provided consistent advertising stability, Google Cloud and Gemini-powered products delivered explosive growth, pushing the company to new revenue highs and reinforcing its position as a full-stack AI leader. Massive investments in computer infrastructure and model development fueled momentum, with Gemini reaching unprecedented user scale and Cloud achieving record profitability milestones. This blend of core advertising strength and rapid AI diversification drove robust financial results, though elevated capital expenditures introduced some margin pressure in the transition year.

1. GOOGL Stock Performance, Market Cap Stability

Alphabet's stock demonstrated strong resilience and upward momentum throughout 2025, benefiting from broad AI enthusiasm and diversified growth drivers. Shares experienced periodic volatility tied to macro concerns and regulatory headlines but delivered solid gains overall, with the market capitalization consistently exceeding $3.7 trillion and reaching peaks near $3.8 trillion during strong quarters. The stock traded at forward multiples reflecting investor confidence in Alphabet's AI leadership, maintaining stability relative to more speculative AI names while outperforming broader market benchmarks in key periods.

2. Financial Performance: Revenue Hits $402.8B, Up 15% YoY

Alphabet posted impressive top-line growth, with full-year revenue climbing 15% year-over-year to $402.836 billion, marking the first full year surpassing the $400 billion threshold. Fourth-quarter revenue reached $113.82 billion, up 18% year-over-year, driven by strength across all major segments. Net income surged 32% to $132.17 billion for the year, with diluted EPS rising 34.45% to $10.81. Operating margin held strong at approximately 32%, supported by operational efficiencies and Cloud profitability gains, even as heavy AI-related CapEx weighed on free cash flow conversion in certain quarters.

3. Google Cloud Surge: Growth Exceeds 40%

Google Cloud emerged as the standout growth engine, with revenues surging 48% in Q4 to $17.7 billion and achieving an annual run rate exceeding $70 billion by year-end. Full-year cloud growth remained above 40%, fueled by explosive demand for AI infrastructure, generative AI tools, and enterprise workloads. Operating income from Cloud more than doubled in several quarters, reflecting improved gross margins and scale efficiencies. The segment's momentum underscored Alphabet's successful pivot toward high-growth cloud and AI services, with enterprise customers increasingly adopting Gemini-integrated solutions.

4. Strategic Milestones: Gemini Drives AI Expansion

The Gemini family of models achieved massive adoption, with the Gemini App growing to over 750 million monthly active users by late 2025 and higher engagement following the Gemini 3 launch. First-party models processed more than 10 billion tokens per minute via direct API usage, demonstrating real-world scale. Alphabet announced 2026 CapEx guidance of $175 billion to $185 billion to aggressively expand AI computers, data centers, networking, and custom TPUs. Additional milestones included deeper Gemini integration across Search, Workspace, Android, and YouTube, plus new enterprise offerings that accelerated Cloud customer wins and revenue per user.

Read more: Ondo Global Markets vs. xStocks: Which Tokenized Stock Platform Is Better in 2025?

The Alphabet Thesis for 2026: 5 Pillars of $GOOGL Stock Valuation

While advertising continues to provide reliable cash flow, Alphabet’s valuation in 2026 increasingly reflects its emergence as a dominant AI and cloud platform, with Gemini adoption and infrastructure scale driving the majority of incremental growth and upside potential.

1. Gemini and AI Adoption: The AI Layer

Gemini powers multimodal AI across Alphabet's ecosystem, enabling rapid deployment in Search, Workspace, Android, and consumer apps. With over 750 million monthly active users and more than 10 billion tokens processed per minute via APIs, Gemini is delivering measurable value and gaining share in generative AI. Analysts expect sustained double-digit growth as enterprise licensing, premium subscriptions, and ad enhancements accelerate monetization.

2. Google Cloud Supercycle: The Growth Layer

Google Cloud is on track for continued 40%+ annual expansion, with a $70 billion+ run rate and growing backlog of AI workloads. Demand for custom TPUs, generative AI tools, and enterprise solutions positions Alphabet to capture significant share in the cloud market, transforming Cloud from a growth segment into a major profitability driver.

3. Search and Advertising Stability: The Foundation Layer

Core Search dominance and YouTube's massive user base provide strong revenue visibility and cash generation, supporting heavy AI investments without compromising financial flexibility. Digital advertising demand remains resilient, acting as a defensive foundation amid macroeconomic uncertainty.

4. Margin Leverage: The Profitability Layer

AI scale, operational efficiencies, and Cloud margin expansion create significant operating leverage. As infrastructure investments mature and Gemini monetization ramps, gross and operating margins are expected to improve, supporting premium valuation multiples and robust free cash flow generation.

5. Infrastructure Moat: The Defensive Layer

Alphabet's custom TPUs, vast global data center footprint, and proprietary networking create formidable competitive barriers. These assets deliver cost advantages, performance leadership, and high stickiness for AI workloads, ensuring long-term platform value as demand for computers continues to grow exponentially.

Alphabet Price Forecasts for 2026: Bull vs. Bear Outlook

Institutional views on Alphabet stock remain divided, balancing powerful AI momentum from Gemini and Google Cloud against concerns over valuation, regulatory risks, and execution on massive CapEx.

| Institution / Analyst | 2026 Price Target | Market Outlook |

| Various Bullish (e.g., Canaccord, Evercore ISI, Needham, Goldman Sachs) | $400 to $420+ | Super-Bullish: Gemini adoption (750M+ users), Cloud acceleration (40%+ growth), and $175B+ CapEx drive strong upside and market share gains. |

| Bank of America (Justin Post) | $370 | Bullish: Reiterates Buy on strong Cloud and AI execution, with lifted forecasts. |

| Market Consensus (aggregated from MarketBeat, TipRanks, Zacks) | $367 to $379 | Moderate Buy: Balanced view on AI investments, Cloud momentum, and diversified revenue streams. |

| JPMorgan (Doug Anmuth) | $395 | Bullish: Maintains Buy, emphasizing AI leadership and growth potential. |

| Bearish Outlooks (various, including low-end estimates) | $220 to $300 | Pessimistic: Premium compression, high CapEx ROI uncertainty, antitrust risks, and macro ad weakness. |

Source: Aggregated from MarketBeat, Investing.com, Yahoo Finance, and analyst notes as of early March 2026

The wide range from bullish targets above $420 to bearish calls below $300 captures the market's uncertainty around Alphabet's ability to monetize Gemini at scale, deliver returns on $175 billion+ CapEx, and navigate regulatory headwinds while sustaining Cloud and advertising growth.

Read More: What Are Coinbase Tokenized Stocks COINX and COINON and How to Buy Them?

The Bull Case: The AI Surge Drives GOOGL Stock Price Above $420

Bulls focus on Gemini's massive adoption (over 750 million monthly active users) and Google Cloud's momentum (40%+ growth, $70 billion+ run rate). If Alphabet sustains AI leadership, successfully deploys $175 billion to $185 billion in infrastructure (TPUs, data centers), and accelerates monetization through enterprise licensing, premium features, and ad enhancements, the company could achieve significant margin expansion and market share gains in cloud and generative AI. This positions Alphabet as the core full-stack AI platform across consumer and enterprise, supporting targets of $400 to $420 or higher by year-end 2026 from analysts like Goldman Sachs, Evercore ISI, and Needham.

The Bear Case: The Fundamental Correction to $300 or Lower

Bears highlight elevated CapEx requirements and potential delays in ROI, alongside ongoing antitrust scrutiny (DOJ cases, EU probes) that could force divestitures or fines. If AI monetization lags, cloud growth slows below 30-40%, or macro weakness hits advertising (still >75% of revenue), multiples could compress toward historical norms. Competitive pressures from Microsoft/Azure, AWS, and others, combined with execution risks, leave limited margins for error, driving the share price lower with some targets in the $220 to $300 range.

Read More: How to Buy Nvidia (NVDA) Stock in 2025: Complete Guide for Beginners

How to Trade Alphabet (GOOGL) on BingX

You can buy and trade Alphabet tokenized stocks on the BingX spot market, which supports tokenized equities alongside spot and derivatives markets.

Buy, Sell, or HODL Alphabet Tokenized Stocks GOOGLX, GOOGLON on the Spot Market

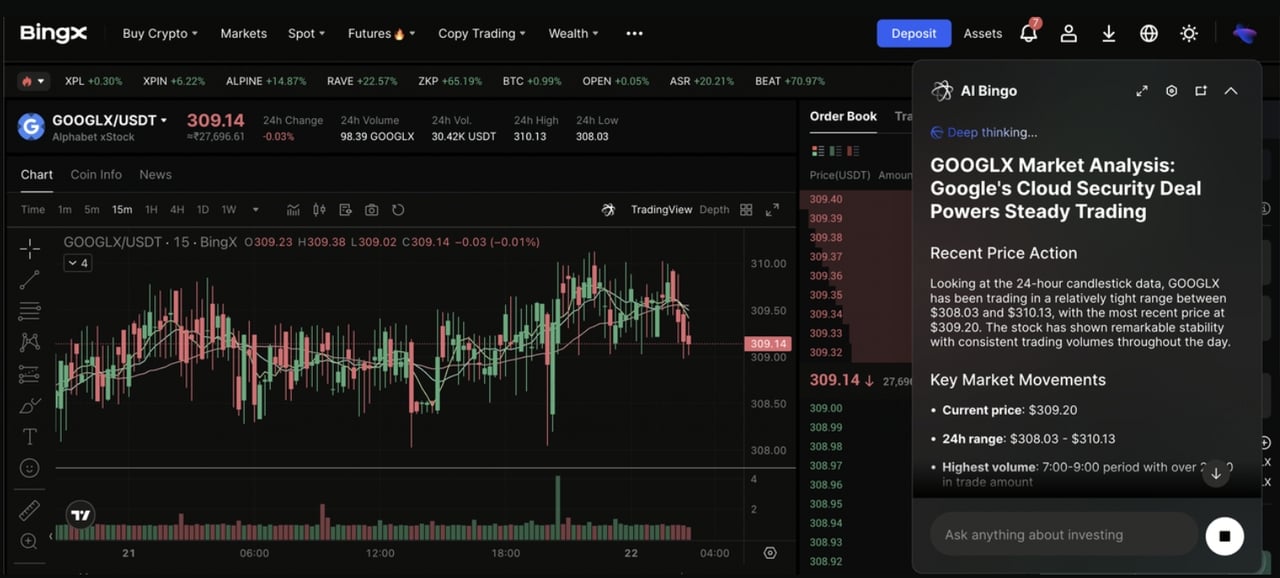

GOOGLX/USDT trading pair on the spot market powered by BingX AI insights

1. Log in to your BingX account.

2. Go to Spot Trading and search for GOOGLX or GOOGLON.

3. Select the GOOGLX/USDT or GOOGLON/USDT trading pair.

4. Choose a Market or Limit order.

5. Enter the amount and confirm your trade.

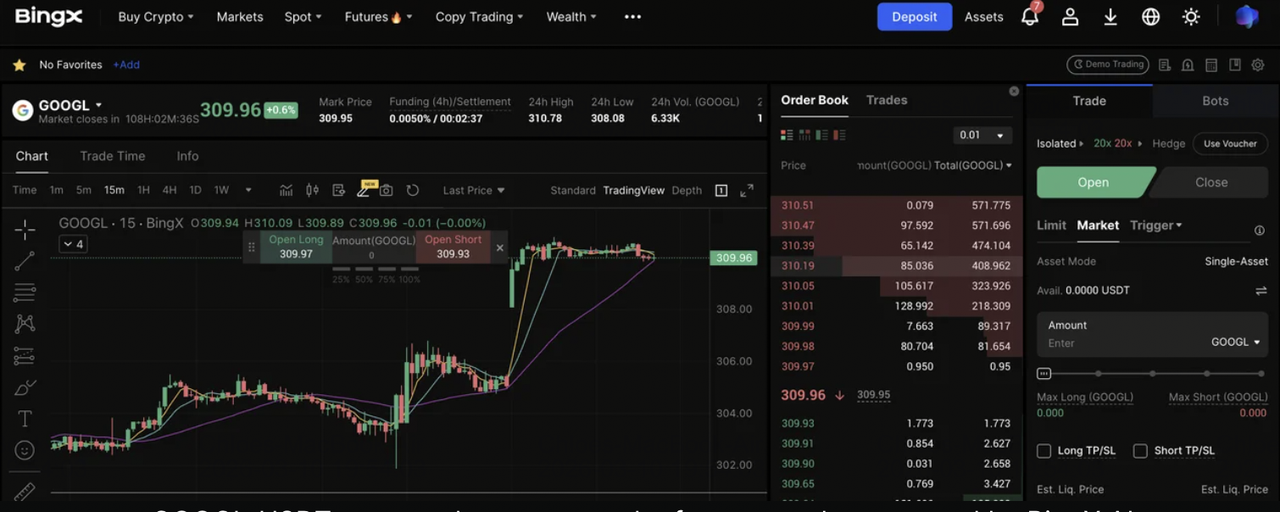

Trade Alphabet (GOOGL) Exposure With Leverage on BingX Futures

GOOGL-USDT perpetual contract on the futures market powered by BingX AI

Beyond Google's tokenized shares, BingX also offers GOOGL perpetual futures, allowing traders to go long or short Alphabet’s price movements using leverage.

1. Log in to BingX and open the Futures trading page.

2. In the search bar, type GOOGL and select the GOOGL/USDT perpetual contract.

3. Choose your margin mode (Isolated or Cross) and set your leverage based on your risk level.

4. Pick your direction: Long (Buy) if you expect GOOGL to rise, or Short (Sell) if you expect it to fall.

5. Select an order type (Market or Limit), enter your position size, and confirm the trade.

6. Set Take-Profit (TP) and Stop-Loss (SL) to manage downside and lock gains automatically.

7. Review market signals, volatility, and trend context before adding, reducing, or closing your position.

Read more: How to Buy Google Stock in 2026: A Guide for TradFi and Crypto Investors

5 Critical Risks to Watch for Alphabet (GOOGL) Traders in 2026

While the Gemini and Google Cloud AI acceleration offers substantial upside through scaled infrastructure and enterprise adoption, investors must navigate a complex landscape of regulatory scrutiny, competitive pressures, execution challenges, and macroeconomic headwinds.

1. Regulatory and Antitrust Headwinds

Alphabet faces ongoing and intensifying regulatory pressure from U.S. Department of Justice antitrust cases, European Commission investigations, and global privacy regulators. Adverse rulings, such as forced divestitures of Android, Chrome, or parts of the ad tech stack, or significant fines (potentially in the billions) could disrupt core revenue streams, limit strategic flexibility, or force structural changes that compress margins and growth.

2. Intensifying Competition in AI and Cloud

Competitors including Microsoft (Azure/OpenAI), Amazon (AWS), Meta (Llama), and emerging players like Anthropic and xAI are rapidly advancing generative AI and cloud offerings. If Alphabet loses share in enterprise AI workloads, Gemini adoption slows, or Google Cloud growth falls below 30 to 40%, the massive $175 billion to $185 billion CapEx in 2026 could deliver lower-than-expected returns, pressuring operating margins and valuation.

3. Massive CapEx Execution and ROI Uncertainty

Alphabet has committed $175 billion to $185 billion in capital expenditures for 2026, primarily to expand AI compute, data centers, and TPUs. Delays in deployment, supply chain constraints for GPUs/TPUs, higher energy costs, or slower monetization of AI infrastructure could lead to prolonged cash burn, margin compression, and investor skepticism about the return on this historic investment level.

4. Macroeconomic and Advertising Sensitivity

Core advertising revenue (Search and YouTube) remains highly sensitive to economic cycles. A slowdown in consumer spending, corporate budgets, or digital ad demand in 2026 could cause flat or declining ad growth, offsetting gains from Cloud and AI. With advertising still representing over 75% of total revenue, any macro weakness would expose the stock to meaningful downside despite diversification efforts.

5. AI Monetization and Product Integration Risks

Gemini has reached over 750 million monthly active users, but sustained monetization through premium subscriptions, enterprise licensing, or ad enhancements remains unproven at scale. Execution missteps, such as integration challenges across products, slower user engagement growth, privacy concerns leading to regulatory pushback, or failure to convert free users to paid, could limit revenue upside and undermine confidence in Alphabet's AI leadership narrative.

Read more: Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

Conclusion: Should You Invest in Alphabet (GOOGL) Stock in 2026?

Deciding whether to invest in Alphabet in 2026 requires viewing it as a high-conviction play on AI infrastructure and cloud leadership rather than a pure advertising company. For growth-oriented investors with tolerance for regulatory and CapEx risk, Gemini's scale (750 million+ MAUs), Google Cloud's $70 billion+ run rate, and $175 billion+ infrastructure build-out support premium valuation if execution delivers market share gains and margin expansion. Successful AI monetization could drive significant long-term returns.

For conservative or value-focused investors, the combination of antitrust exposure, massive CapEx requirements, advertising cyclicality, and competitive intensity presents substantial risks. The stock’s performance now ties to multiple binary outcomes: either AI and cloud accelerate to justify the investment, or regulatory/commercial headwinds trigger compression toward more normalized multiples. Closely monitor quarterly Cloud revenue growth, Gemini user metrics, CapEx deployment updates, and antitrust case developments as the clearest indicators of whether Alphabet can realize its full-stack AI vision at scale.

Risk Reminder: Trading and investing in equities like GOOGL involves substantial risk of capital loss. Alphabet’s high valuation, regulatory exposure, massive CapEx commitments, and dependence on AI execution make it a high-risk asset. Investors should conduct thorough independent research and consider professional financial advice before allocating capital.

Related Reading

1. Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

2. Oracle (ORCL) Stock Price Outlook for 2026: Can AI Cloud Infrastructure Take ORCL Back to Its Highs?

3. Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

4. Reddit (RDDT) Price Outlook for 2026: Can AI Data Licensing Drive RDDT Back to $200?

5. Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?