In early June 2026, Qualcomm Corp. (Nasdaq: QCOM) is facing a key valuation test. Once seen mainly as a mobile modem and Snapdragon chip leader, Qualcomm is now trying to prove it can expand into edge AI, automotive, IoT, and data center custom silicon. The company reported record automotive revenue of $1.33 billion in Q2 FY2026, confirmed a hyperscaler custom silicon engagement for calendar Q4 2026, and introduced Dragonfly, its new AI data center brand for CPUs, AI accelerators, and ASIC products. Still, after a 50% rally from its March low to a 52-week high of $247.90, QCOM fell about 11% on June 5 after NVIDIA unveiled its RTX Spark AI PC chip, raising questions about whether Qualcomm’s edge AI premium is already priced in.

The bull case is that Qualcomm is becoming a broader AI infrastructure and edge computing platform. The risk is that NVIDIA’s AI PC push, Apple’s modem insourcing, China handset weakness, and limited near-term data center revenue are all hitting at once. With Q3 FY2026 guidance falling to $9.2 billion to $10 billion from Q2’s $10.6 billion, investors are watching Qualcomm’s June 24 Investor Day to see whether data center and physical AI can reset expectations higher. This guide breaks down the QCOM stock forecast, 2026 price scenarios, key risks, and how to trade QCOM stock futures on BingX TradFi with USDT collateral.

Why Is Qualcomm (QCOM) Stock Surging in 2026?

Qualcomm’s 2026 story is driven by five forces: automotive and IoT growth, the Dragonfly data center push, Alphawave Semi integration, the NVIDIA AI PC overhang, and aggressive capital returns.

- Q2 FY2026 earnings showed diversification is working: Qualcomm reported Q2 FY2026 revenue of $10.6 billion, beating consensus for the fourth straight quarter, with non-GAAP EPS of $2.65 at the high end of guidance. Automotive revenue reached a record $1.33 billion, up 38% year over year, and management guided for an automotive exit run rate above $6 billion by the end of fiscal 2026. IoT revenue grew 9%, while combined Automotive and IoT revenue reached $3.05 billion, showing that Qualcomm’s growth story is no longer only about handsets.

- Dragonfly marks a full-scale move into AI infrastructure: At Computex 2026, CEO Cristiano Amon introduced Dragonfly, Qualcomm’s data center AI brand covering server CPUs, AI accelerators, and custom ASIC products. The roadmap includes a supply agreement with Saudi AI firm Humain and a ByteDance ASIC project. CFO Akash Palkhiwala also confirmed that initial shipments for a custom silicon engagement with a leading hyperscaler remain on track for later in calendar 2026, describing it as a multi-generation engagement. Qualcomm’s June 24 Investor Day on Data Center and Physical AI is expected to give investors clearer revenue targets.

- Alphawave Semi expands Qualcomm’s data center addressable market: Qualcomm completed its Alphawave Semi acquisition in Q1 FY2026, adding high-speed connectivity IP for data center interconnects. This strengthens Qualcomm’s custom silicon stack and positions the company to compete across more of the AI data center supply chain, not just AI inference accelerators.

- NVIDIA’s RTX Spark created a sharp AI PC sell-off, but the threat is still debated: QCOM fell about 11% on June 5 after NVIDIA unveiled RTX Spark at Computex, a high-performance AI PC chip developed with Microsoft for local AI agents. The concern is that NVIDIA could weaken Qualcomm’s Snapdragon design-win pipeline for Windows AI PCs. Bulls argue Qualcomm still has advantages in power efficiency, integrated modems, and thin-and-light laptop design, while NVIDIA’s GPU-centric approach may face thermal and battery constraints.

- Capital returns support the stock while new AI revenue scales: Qualcomm authorized a $20 billion share repurchase program and returned $2.8 billion to shareholders in Q2 FY2026 through buybacks and dividends. Its quarterly dividend stands at $0.89, with a yield of roughly 2% at current prices, while total FY2025 capital return reached $12.6 billion. For a company trading below 20x forward earnings while investing in data center and physical AI, this capital return profile gives QCOM a stronger valuation floor.

Read More: Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

What Is Qualcomm (Nasdaq: QCOM)?

Qualcomm Incorporated (Nasdaq: QCOM) is a San Diego-based semiconductor and wireless technology company best known for Snapdragon processors, mobile modems, and wireless patent licensing. Its business is split mainly between QCT, which designs chips for smartphones, automotive, IoT, AI PCs, and custom silicon, and QTL, which licenses Qualcomm’s wireless technology patents to device manufacturers. This gives Qualcomm both product revenue from chips and high-margin licensing revenue from its wireless IP portfolio.

In 2026, Qualcomm is increasingly viewed as an edge AI and custom silicon company, not just a smartphone chip supplier. Its Snapdragon platforms support on-device AI across smartphones, Windows AI PCs, connected vehicles, and IoT devices, where power efficiency, local inference, and wireless connectivity matter. At the same time, Qualcomm’s Dragonfly data center push, Alphawave acquisition, and confirmed hyperscaler custom silicon engagement give it a path into AI infrastructure. The key investor question is whether Qualcomm can turn its mobile and wireless leadership into a broader AI platform spanning edge devices, automotive systems, AI PCs, and data center custom silicon.

Read More: Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

Qualcomm’s Performance in Early 2026: Automotive Record, Handset Headwinds, and AI Expansion

Qualcomm entered fiscal 2026 with a split performance. Its handset business weakened as Chinese OEMs cut orders due to memory supply constraints and inventory digestion, causing QCT handset revenue to fall 13% sequentially in Q2. At the same time, automotive and IoT delivered record results, showing that Qualcomm’s edge AI strategy is gaining traction beyond smartphones. Automotive chips, IoT platforms, AI PCs, and connected devices are becoming more important as AI workloads move closer to users instead of staying only in the cloud.

Q2 FY2026 also showed improving operating leverage despite handset softness. Non-GAAP EPS reached $2.65, beating consensus and landing at the high end of guidance, while Qualcomm’s $20 billion buyback authorization signaled confidence in free cash flow. The company also pushed deeper into AI infrastructure through the Dragonfly data center brand, the Alphawave acquisition, and a confirmed hyperscaler custom silicon engagement expected to begin shipments later in calendar 2026. Management guided Q3 FY2026 revenue of $9.2 billion to $10 billion and non-GAAP EPS of $2.10 to $2.30, reflecting near-term handset weakness before a potential Q4 recovery tied to China inventory normalization and early custom silicon shipments.

Qualcomm’s 2026 Trading Strategy: The Diversification Re-Rating Debate

To trade Qualcomm’s 2026 setup, investors need to watch three forces: whether the June 24 Investor Day on Data Center and Physical AI gives the market a clearer data center revenue roadmap, whether China handset weakness bottoms in Q3 as guided, and whether NVIDIA’s RTX Spark creates lasting pressure on Snapdragon AI PC design wins or only short-term sentiment weakness.

1. The $195 to $215 zone is the key support floor

After the 11% Computex-driven sell-off in early June 2026, QCOM pulled back from its $247.90 intraday peak toward the $195 to $215 support zone, where the post-Q2 breakout level overlaps with the 50-day moving average. A decisive break below $190 could revive downside pressure toward the $175 consensus target area. A confirmed hold above $215 before the June 24 Investor Day would strengthen the case for a move toward $260 if Qualcomm provides stronger-than-expected data center revenue guidance.

2. The main valuation debate is diversification premium vs. handset discount

Bulls argue Qualcomm should be valued as a multi-platform AI and custom silicon company across edge devices, automotive, IoT, AI PCs, and data centers. At roughly 16x to 19x forward earnings, they see QCOM as undervaluing Dragonfly and the hyperscaler ASIC opportunity. Bears argue the stock still deserves a handset discount because of slower smartphone replacement cycles, Apple modem insourcing risk, and NVIDIA’s new AI PC competition. For swing traders, the key catalyst is whether CEO Cristiano Amon can attach hard fiscal 2027 revenue numbers to the Dragonfly roadmap.

3. Automotive growth and China recovery can set the floor and ceiling

Automotive is Qualcomm’s clearest execution proof point. Q2 automotive revenue reached a record $1.33 billion, up 38% year over year, with management guiding for an exit run rate above $6 billion by fiscal year-end. Multi-year design wins with Stellantis, BMW, Mercedes-Benz, and Chinese NEV manufacturers are now converting into revenue. China handset recovery is the other swing factor. If Android OEM inventory normalizes and orders resume in Q3 and Q4 as guided, handset revenue could stabilize and reduce the drag on QCT results.

Qualcomm 2026 Forecast: $260+ Investor Day Upside vs. $175 Handset Drag Risk

Qualcomm’s 2026 outlook depends on one central question: can the June 24 Investor Day give investors credible data center revenue targets for Dragonfly and its hyperscaler custom silicon business? The bull case is that Qualcomm’s diversification revenue is real but not yet fully reflected in consensus models. The bear case is that the stock has already priced in too much upside before data center revenue reaches scale.

The Bull Case: QCOM Breaks Above $260 on Strong Data Center Guidance

The bullish scenario requires Qualcomm to prove that Dragonfly can become a real AI data center revenue driver, not just a long-term concept. If the June 24 Investor Day gives clear fiscal 2027 targets for AI inference, custom silicon, and hyperscaler deployments, investors could start valuing QCOM as an AI infrastructure and edge AI platform rather than a handset chip stock. This upside would be supported by Q4 2026 hyperscaler shipments, automotive exiting fiscal 2026 above a $6 billion run rate, Snapdragon’s role in on-device AI, and the $20 billion buyback supporting EPS. If these pieces come together, QCOM could break into the $260 to $280 range, with a stronger upside case reaching $279 to $330 within 12 months.

The Base Case: QCOM Consolidates Between $200 and $250

The base case is steady execution without a major valuation reset. Qualcomm’s Investor Day provides a directional data center roadmap, but not enough hard fiscal 2027 revenue detail to trigger large consensus upgrades. Q3 handset revenue bottoms as guided, automotive continues to grow, and the first hyperscaler custom silicon shipments begin in Q4 without yet becoming a major revenue contributor. Under this scenario, QCOM likely trades between $200 and $250 while investors wait for Q4 FY2026 results and fiscal 2027 guidance to confirm whether Dragonfly can scale.

The Bear Case: QCOM Falls Toward $175 if Dragonfly Disappoints

The bearish scenario would be driven by an underwhelming Investor Day. If Qualcomm fails to quantify data center revenue, or if the hyperscaler engagement appears smaller or slower than expected, the stock’s premium to the $175 to $180 Street consensus target could lose support. In that case, QCOM could retrace toward $175, where handset-cycle valuation and cash-flow-based valuation converge. NVIDIA’s RTX Spark pressuring Snapdragon AI PC design wins, deeper China handset weakness, or faster Apple modem insourcing would add further downside risk.

Read More: Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

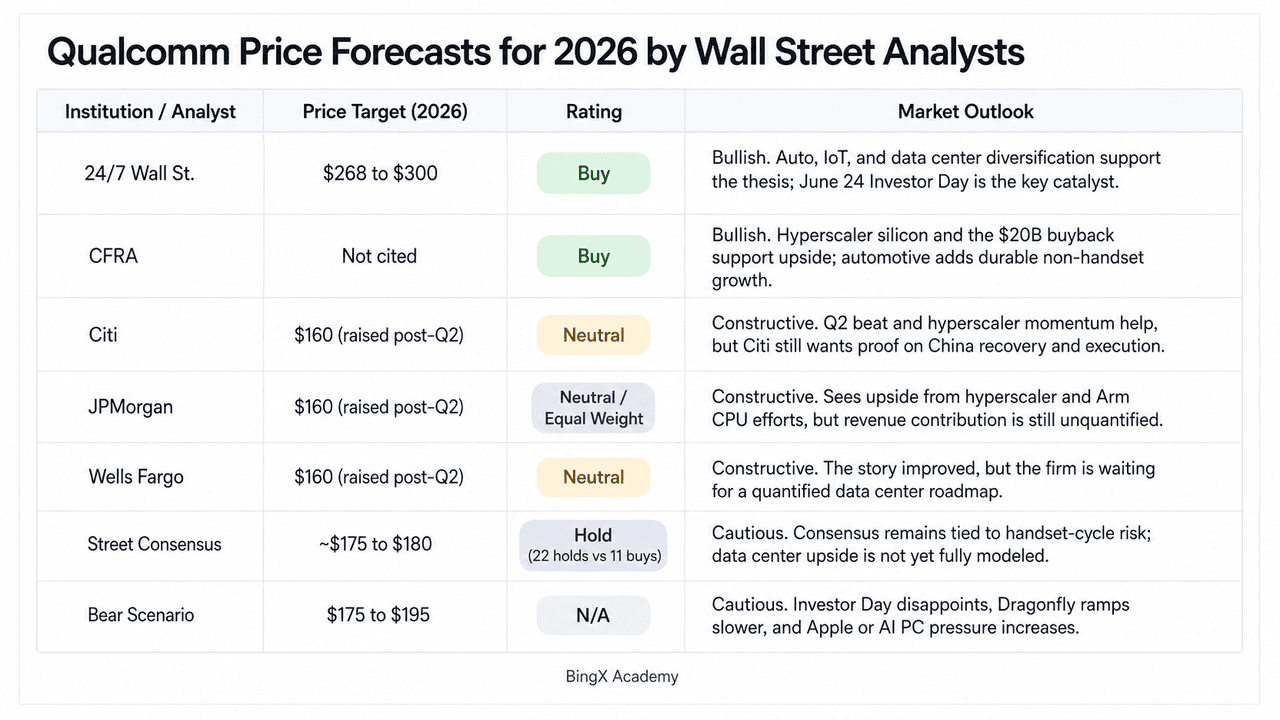

Qualcomm Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Analyst |

Price Target (2026) |

Rating |

Market Outlook |

|

24/7 Wall St. |

$268 to $300 |

Buy |

Bullish. Diversification to automotive, IoT, and data center custom silicon is real; Dragonfly and hyperscaler ASIC engagement not yet in consensus models. June 24 Investor Day is the re-rating catalyst. |

|

CFRA |

Not cited |

Buy |

Bullish. Confirmed multi-generation hyperscaler silicon engagement and $20 billion buyback authorization support the thesis. Automotive at $6B+ run rate provides durable non-handset revenue anchor. |

|

Citi |

$160 (raised post-Q2) |

Neutral |

Constructive. Raised target after Q2 beat citing hyperscaler ASIC ramp and expected China handset trough in Q3 2026, but wants execution proof before turning outright bullish. |

|

JPMorgan |

$160 (raised post-Q2) |

Neutral / Equal Weight |

Constructive. Cited hyperscaler ramp and Arm-based CPU pipeline as meaningful but unquantified upside. Downgraded earlier in 2026 on handset weakness before raising the target post-Q2. |

|

Wells Fargo |

$160 (raised post-Q2) |

Neutral |

Constructive. Results "positively overshadowed" by hyperscaler ASIC announcement. Waiting for June 24 Investor Day to provide quantified data center roadmap before upgrading rating. |

|

Street Consensus |

~$175 to $180 |

Hold (22 holds vs 11 buys) |

Cautious. Consensus remains anchored to handset cycle risk, Apple modem insourcing, and China concentration. Data center revenue has not yet been quantified in models. Wide gap vs current price. |

|

Bear Scenario |

$175 to $195 |

N/A |

Cautious. Assumes Investor Day underwhelms, Dragonfly commercial ramp delays into fiscal 2028, NVIDIA erodes Snapdragon X PC share, and Apple modem insourcing accelerates timeline. |

How to Trade Qualcomm (QCOM) Stock Futures on BingX TradFi

Qualcomm is entering a high-stakes product cycle shaped by China handset weakness, record automotive growth, and a still-underpriced data center AI opportunity. For tactical traders, QCOM’s sharp two-way volatility creates potential trading opportunities through BingX TradFi.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select Qualcomm (QCOM). Search for the QCOM-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect Qualcomm’s Investor Day, data center roadmap, hyperscaler custom silicon shipments, automotive growth, and buyback program to support further upside. Open Short if you expect valuation pressure from a weaker Investor Day, deeper China handset weakness, or stronger NVIDIA competition in AI PCs.

Step 4: Set leverage and margin mode. Apply your preferred Isolated or Cross-Margin parameters alongside disciplined leverage ratios to maximize capital efficiency while controlling liquidation risk.

Step 5: Use TP/SL risk controls. Set Take-Profit and Stop-Loss (TP/SL) orders before entering the trade. QCOM’s 2026 setup includes both upside catalysts and downside risks, so disciplined exits are essential when trading stock futures with leverage.

Top 5 Risks to Consider Before Investing in Qualcomm Stock

Qualcomm’s AI and diversification story is compelling, but QCOM still faces risks tied to Apple, China, NVIDIA, data center timing, and valuation.

- Apple modem insourcing risk: Apple has been developing its own 5G modem and reducing reliance on Qualcomm components. If Apple eventually phases out Qualcomm modems across the iPhone lineup, QCOM could lose both QCT chip revenue and part of its high-margin QTL licensing income. The timing is still uncertain, but this remains one of Qualcomm’s biggest long-term risks.

- China handset weakness: Qualcomm depends heavily on Chinese Android OEMs such as Xiaomi, OPPO, vivo, and Honor. In 2026, memory supply constraints and inventory drawdowns have already pressured handset orders. If China demand stays weak or U.S.-China trade restrictions intensify, Qualcomm’s handset recovery could be slower than expected.

- NVIDIA AI PC competition: NVIDIA’s RTX Spark adds new competition to Qualcomm’s Snapdragon platform in Windows AI PCs. Qualcomm still has advantages in power efficiency, integrated connectivity, and thin-and-light laptop design, but NVIDIA’s AI software ecosystem and developer mindshare could influence future OEM design wins.

- Data center revenue timing risk: Qualcomm’s Dragonfly data center strategy and hyperscaler custom silicon engagement are promising, but revenue is still not fully quantified. Initial shipments are expected later in 2026, yet early shipments may not immediately translate into large revenue. If Investor Day does not provide clear fiscal 2027 targets, the AI re-rating could lose momentum.

- Valuation gap vs. consensus: QCOM’s recent $200 to $250 trading range sits well above the Street consensus target of roughly $175 to $180. That gap reflects optimism around AI, automotive, custom silicon, and buybacks, but it also raises downside risk. A weak Investor Day, deeper handset pressure, or Q3 miss could trigger a sharp valuation reset.

Final Thoughts: Is Qualcomm Stock a Buy in 2026?

As of June 2026, Qualcomm (QCOM) is one of the more interesting semiconductor setups because its story is no longer only about smartphones. Record Q2 FY2026 revenue of $10.6 billion, automotive moving toward a $6 billion-plus annual run rate, a confirmed hyperscaler custom silicon engagement, the Dragonfly data center push, and a $20 billion buyback authorization all point to a company making real progress beyond mobile modems. The 50% rally from the March trough to $247.90 reflected that optimism, while the 11% pullback after NVIDIA’s AI PC announcement showed how fragile the edge AI premium remains before data center revenue scales.

The June 24 Investor Day is now the key catalyst. With Street consensus still near $175 to $180 and analyst ratings split between Hold and Buy, Qualcomm needs to show that Dragonfly, automotive AI, and custom silicon can grow fast enough to offset Apple modem risk and China handset weakness. For active traders, QCOM futures on BingX TradFi offer a way to trade both sides of this high-volatility setup. For longer-term investors, the diversification thesis is real, but whether QCOM is fairly valued at current levels depends on how much revenue visibility Cristiano Amon can provide on June 24.

Related Reading

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?