In late June 2026, Pfizer Inc. (NYSE: PFE) sits at a critical crossroads, balancing a rock-bottom equity valuation and mouth-watering dividend against steep structural headwinds. Trading near $23.67, the stock has shed over 55% of its value since its 2021 pandemic peak, presenting a classic value-versus-growth debate for macro traders.

While long-term investors have felt the pain of a multi-year bear cycle driven by cratering COVID-19 product sales, the structural landscape for the second half of 2026 is rapidly evolving. Active market participants are currently weighing a highly resilient Q1 report, which delivered top-line and bottom-line beats, against major corporate shifts, including an impending CFO transition and high-stakes clinical trials.

The fundamental case for a Pfizer stabilization is heavily backed by the company's aggressive pivot toward premium oncology treatments and a major legal win that extended exclusivity for a key blockbuster drug. However, an looming patent cliff window between 2026 and 2030 means that newer pipeline developments must scale rapidly to defend the company's long-term earnings capability.

This guide breaks down the Pfizer stock forecast and price prediction for the remainder of 2026, drawing on data from RBC Capital, BMO Capital, Guggenheim, consensus Wall Street price targets, and official corporate guidance.

You will also discover how to trade Pfizer Inc. (PFE) stock futures on BingX TradFi using USDT collateral.

Top 5 Things for Pfizer (PFE) Traders to Know in 2026

As Pfizer navigates an intense period of operational rebalancing, active traders should keep a close eye on these five market-moving catalysts:

- The Vyndamax Patent Settlement Shield: In a game-changing intellectual property victory, Pfizer settled patent disputes with generic manufacturers over its blockbusting heart drug, Vyndamax. The settlement extends market exclusivity through mid-2031, preserving billions in high-margin cash flow past the heavily feared 2028 baseline.

- The SigVie-002 Phase 3 Mixed Data: On June 22, 2026, Pfizer revealed that its Phase 3 trial for sigvotatug vedotin, an antibody-drug conjugate targeting non-small cell lung cancer, missed its primary endpoint for overall survival in the broad population. However, strong positive survival trends in a large single-prior-therapy subgroup have kept long-term commercial optimization hopes alive.

- CFO Leadership Transition: CFO Dave Denton announced his departure effective August 15, 2026, to transition into the consumer goods sector. Cecile Guegan has been installed as Interim CFO while a global search is underway. Pfizer aggressively reaffirmed its full-year 2026 financial guidance alongside the announcement to project operational stability.

- The 351st Consecutive Quarterly Dividend: Solidifying its status as an elite income play, Pfizer declared its Q3 2026 cash dividend of $0.43 per share, payable on September 1, 2026. This elevates the trailing dividend yield to an exceptional 7.27%, establishing a powerful floor for value buyers.

- Reaffirmed Full-Year Guidance Midpoint: Management continues to confidently target full-year 2026 revenues of $59.5 billion to $62.5 billion and adjusted diluted EPS of $2.80 to $3.00, confirming that the post-pandemic bottom is likely locked in.

What Is Pfizer Inc. (PFE)?

Pfizer Inc. (NYSE: PFE) is a premier global biopharmaceutical enterprise engaged in the discovery, development, manufacturing, and distribution of prescription medicines and innovative vaccines. Founded in 1849, the New York-headquartered giant operates a massive international commercial infrastructure, leaning heavily into high-barrier therapeutic fields such as internal medicine, vaccines, immunology, and specialized rare diseases.

In modern financial markets, Pfizer is viewed as a high-yield value restructuring play. Under the direction of CEO Dr. Albert Bourla, the firm is aggressively redeploying its historic pandemic windfall to reshape its portfolio. Following the $43 billion acquisition of Seagen, Pfizer has transformed its internal profile to center around oncology, utilizing next-generation antibody-drug conjugates (ADCs) to replace aging legacied products and create a sustainable, long-term growth engine.

Pfizer's Performance in Early 2026: Pipeline Wins vs. Revenue Cliffs

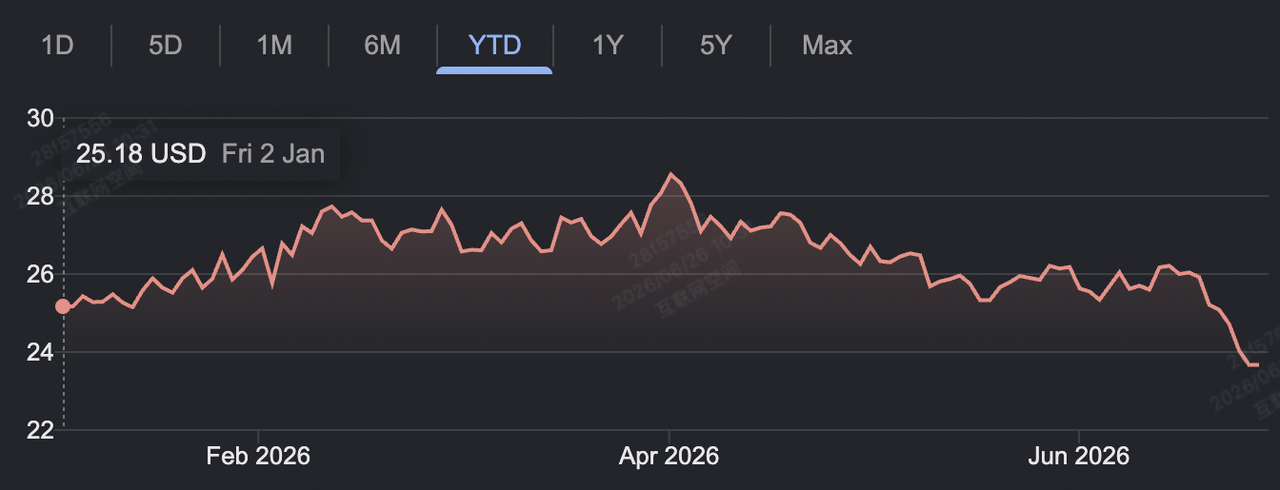

Pfizer YTD stock performance as of June 2026 | Source: Google Finance

Pfizer kicked off 2026 by demonstrating robust operational resilience. On May 5, 2026, the company handed down its Q1 financial results, delivering an absolute top-line revenue of $14.45 billion, outperforming Wall Street's consensus expectation of $13.80 billion. Adjusted diluted EPS trickled in at $0.75, beating the $0.72 forecast, anchored by a blistering $2.17 billion quarterly print from its premier blood thinner, Eliquis.

Despite this operational execution, structural headwinds continue to cap macro market momentum. Revenue from its COVID-19 vaccine franchise, Comirnaty, fell 59% year-over-year to $232 million for the quarter, highlighting a permanent structural shift. Concurrently, the company is managing an upcoming cluster of loss-of-exclusivity (LOE) events for legacy blockbusters like Ibrance and Xeljanz, which management estimates will trigger a direct $1.5 billion top-line drag across 2026.

To defend its corporate margins, Pfizer is executing a massive manufacturing optimization and efficiency campaign, aiming for $7.2 billion in net structural savings by the close of 2026. This intensive cost discipline has stabilized gross margins in the mid-70s percentage range, enabling the firm to reliably generate free cash flow and support its extensive pipeline investments while fully servicing its high-yield dividend commitments.

Pfizer's 2026 Trading Strategy: Navigating the PFE Value Accumulation Zone

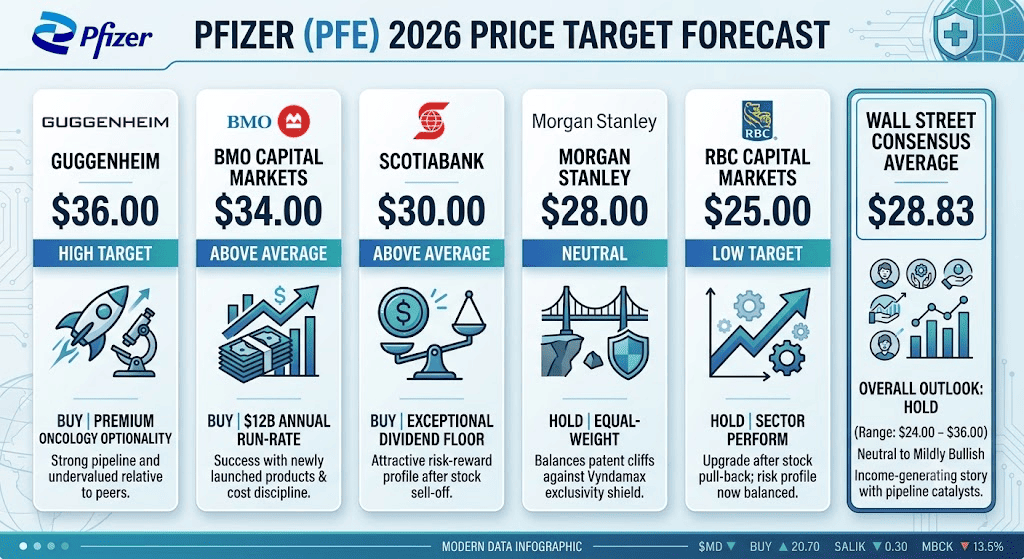

Price predictions for Pfizer stock in 2026 by Wall Street analysts

Trading a large-cap pharmaceutical value asset during a core portfolio transition requires abandoning momentum chasing and focusing on long-term accumulation zones, valuation multiples, and technical supports:

The $23.00 – $24.00 Macro Support Floor

Technical analysts highlight the current $23.11 to $24.00 range as a multi-year structural accumulation zone. With the Relative Strength Index (RSI) hovering near oversold territory at 33.3 and the stock trading at a rock-bottom forward P/E multiple of 9.0x, the downside risk appears structurally insulated by the company's 7.2% dividend yield, making pullbacks into this range attractive for spot swing traders.

Capitalizing on Volatile Pipeline Readout Catalysts

Biopharma equities are heavily driven by binary clinical data releases. Pfizer’s options market saw its put/call ratio swing defensively to 1.02 following the recent lung cancer trial miss, reflecting near-term open-market hedging. Traders can position around upcoming late-stage clinical readouts, such as mevrometostat in prostate cancer in late 2026, by trading directional breakouts on the futures market or utilizing range-bound mean reversion strategies.

Tracking the Sector Valuation Discount Gap

Pfizer is trading at a steep historical discount compared to its large-cap pharmaceutical peers. PFE's enterprise value-to-EBITDA (EV/EBITDA) multiple sits at a modest 8.1x, matching distressed peers like Bristol-Myers Squibb (8.1x) while trading far below asset expansion stories like Eli Lilly (23.3x) and AstraZeneca (13.7x). This valuation discount offers an asymmetric risk-reward profile if Pfizer's oncology or metabolic pipeline registers an unexpected regulatory win.

Pfizer Stock Forecast 2026: $36.00 Institutional Peak vs. $24.00 Structural Floor

Evaluating Pfizer's target trajectories for the rest of 2026 requires balancing cost-saving initiatives and pipeline additions against severe post-pandemic revenue cliffs.

Pfizer's Bull Case: The $30.00 – $36.00 Oncology Expansion and Re-Rating Rally

The bullish framework relies on the accelerating commercial scaling of recently acquired oncology assets. Supported by top-tier institutional price targets pointing toward $34.00 (BMO Capital, Jefferies) and an absolute peak target of $36.00 (Guggenheim), this scenario assumes that the newly expanded Seagen portfolio sustains its high-velocity operational revenue growth of 20% year-over-year.

As high-margin cancer products like Padcev expand into broader treatment indicators, Pfizer's massive operational leverage takes hold. If the company pair its $7.2 billion efficiency program with positive clinical updates from its early-stage oral obesity program, the market will aggressively re-rate PFE away from its value-trap valuation. This multiple expansion could easily push the stock out of its accumulation channel to test its 52-week high of $28.74, eventually hitting peak targets north of $30.00.

The Base Case for PFE Stock: $26.00 – $29.00 Range-Bound Consolidation

The base case envisions a steady consolidation phase where Wall Street systematically balances Pfizer's underlying value profile against near-term top-line stagnation. Under this framework, full-year 2026 revenues are projected to land near the $61 billion midpoint of official guidance, reflecting flat year-over-year operational expansion.

Because the broader market wants to see sustained revenue replacement before paying a premium multiple, near-term price updates will likely remain tightly controlled. Wall Street's consensus average price target settles between $28.00 and $29.50. For market participants, this establishes a reliable, range-bound trading channel between $25.00 and $28.00, where incremental pipeline progress is offset by legacy drug pricing pressures.

Pfizer's Bear Case: The $21.00 – $23.00 Patent Cliff and Pipeline Delay Trap

The bearish outlook focuses on accelerated legacy asset erosion and development timeline slips. If generic copycats erode pricing power on core legacy drugs faster than the oncology pipeline can scale, top-line revenues will drift toward the lower bound of guidance at $59.5 billion.

This headwind would be worsened if upcoming oncology and vaccine trials hit unexpected regulatory delays, or if the permanent CFO selection process introduces execution uncertainty. Under this scenario, institutional investors would demand a larger safety margin to offset the tight dividend coverage. A sustained break below the critical $23.11 support baseline would trigger an open-market liquidation trend, pushing the stock down to test historical floors in the low $21.00s.

Pfizer (PFE) Price Predictions for 2026 by Wall Street Analysts

|

Institution / Source |

2026 Price Target (Low/Avg/High) |

Overall Market Outlook & Rating Consensus |

|

Guggenheim |

$36.00 |

Buy: Highlights premium oncology optionality and deep structural undervaluation relative to large-cap peers. |

|

BMO Capital Markets |

$34.00 |

Buy: Points to the $12B annualized run-rate of newly launched products and strong cost discipline. |

|

Scotiabank |

$30.00 |

Buy: Views the underlying dividend floor as exceptional; notes risk-reward skews highly positive post-selloff. |

|

Morgan Stanley |

$28.00 |

Hold / Equal-Weight: Neutral stance; balances clear upcoming patent cliffs against the multi-year Vyndamax exclusivity shield. |

|

RBC Capital Markets |

$25.00 |

Hold / Sector Perform: Upgraded from Underperform; notes the stock pull-back has balanced the near-term risk profile. |

|

Wall Street Consensus Average |

$28.83 (Range: $24.00 – $36.00) |

Hold: Core consensus remains neutral-to-mildly-bullish; stock is widely categorized as an income-generating catalyst story. |

How to Trade Pfizer (PFE) Stock Futures on BingX TradFi

PFE/USDT perpetual contract on BingX TradFi

As Pfizer enters this high-stakes period of long-term asset transition and key technical price discovery, tactical traders can capitalize on its daily price swings via the BingX ecosystem.

- Access BingX TradFi: Head over to the specialized TradFi terminal on the main BingX exchange dashboard.

- Select Pfizer Inc. (PFE): Use the asset search tool to locate and select the PFE-USDT perpetual contract.

- Establish Your Market Position: Choose Open Long if you anticipate that the multi-billion dollar Vyndamax settlement and structural cost savings will lift the stock toward its $34.00 bull target. Select Open Short if you believe patent cliff pressures and leadership changes will pull the price back toward the $23.00 accumulation floor.

- Configure Leverage and Margin Parameters: Apply your preferred Isolated or Cross-Margin parameters alongside conservative leverage to safely optimize capital efficiency.

- Implement Risk Mitigations: Use advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to lock in short-term trading gains and insulate your capital account from unexpected clinical headline gaps.

Top 5 Risks to Consider Before Trading Pfizer Stock

While Pfizer's depressed valuation offers a highly liquid environment for tactical traders, navigating the asset demands a clear assessment of its underlying corporate structural risks:

- Imminent Loss of Exclusivity (LOE) Pressure: Blockbuster treatments like Eliquis and Ibrance face major patent protection cliffs between 2026 and 2030, threatening a significant long-term top-line revenue drag.

- High Binary Clinical Trial Risk: The biopharmaceutical sector is intensely exposed to trial outcomes; unexpected clinical misses can instantly erase billions in perceived pipeline value.

- Tight Dividend Payout Coverage: With projected 2026 adjusted EPS guided between $2.80 and $3.00, the annualized $1.72 dividend payout consumes a massive portion of earnings, leaving thin coverage margins if operations contract unexpectedly.

- Execution Risk in Executive Leadership: Transitioning away from long-time financial leadership amid an active global CFO search introduces strategic execution risk for the firm's cost-containment initiatives.

- Post-COVID Revenue Normalization Slump: Comirnaty and Paxlovid sales remain highly volatile and tied to unpredictable global infection waves, presenting an ongoing forecasting challenge for Wall Street analysts.

Final Thoughts: Is Pfizer Stock a Buy in 2026?

In late June 2026, Pfizer operates as an elite, income-generating volatility vehicle rather than an aggressive, short-term momentum play. Fundamentally, management’s ability to defend its full-year guidance and preserve cash via the Vyndamax patent extension confirms the pharmaceutical core is generating strong cash flow.

However, trading a mega-cap stock navigating a long-term pipeline transition requires precise execution discipline. For active short-term traders, Pfizer provides an ideal environment for capturing predictable percentage swings via BingX futures contracts. Conversely, market participants looking for long-term capital stability should carefully time entries around key support baselines, ensuring that any exposure is backed by clear risk boundaries.

Risk Reminder: Trading highly regulated, pipeline-dependent healthcare equities carries high capital risk due to structural operational leverage, regulatory shifts, and binary clinical trial data releases. Always enforce disciplined risk protocols, realistic position sizes, and non-negotiable stop-losses.

Related Reading

- Corbus Pharmaceuticals Stock Price Prediction 2026: $54 Street-High Oncology Surge or Binary Obesity

- AMC Stock Price Prediction 2026: Fundamental Turnaround or Massive Dilution Trap?

- Ford Stock Price Prediction 2026: $20 Data Center Battery Boom or Legacy Recall Trap?

- S&P 500 Forecast 2026: 7,600 Bull Run or a 6,000 Energy-Driven Crash?

- Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?