In early June 2026, Netflix (NFLX) finds itself positioned at a critical crossroads between capital efficiency and shifting competitive dynamics. Following a punishing eight-session losing streak, its longest since November 2022, the Los Gatos-headquartered streaming pioneer is currently trading near $82.64, nursing a 13% loss year-to-date and sitting roughly 39% below its mid-2025 all-time high of $134.12.

While the broader equity market has marched higher, Netflix has been weighed down by post-earnings multi-quarter repricings. Investors are aggressively evaluating an incredibly robust free cash flow profile against a notable macro rotation where market participants are shunning traditional growth narratives in favor of explicit artificial intelligence infrastructure plays.

As the global entertainment ecosystem shifts from aggressive subscriber acquisition to optimized monetization, Netflix's pivot into ad-supported tiers and live events has transformed the company into an operational cash machine. However, heavy competitive pressures from tech-adjacent ecosystems have capped multiple expansion.

This guide breaks down the Netflix stock forecast and price prediction for the remainder of 2026, utilizing data from KeyBanc Capital Markets, Bernstein, Simply Wall St, LSEG consensus estimates, and official regulatory disclosures.

You will also discover how to trade Netflix (NFLX) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Netflix (NFLX) Traders to Know in 2026

As Netflix navigates a high-stakes transition from an unhedged content spender into an ad-monetized utility, traders must closely monitor these five market-moving factors:

- The $3 Billion Ad-Revenue Scaling Target: Netflix’s ad-supported tier is growing rapidly, accounting for over 60% of first-quarter sign-ups in active ad markets. Management projects 2026 ad revenue will reach approximately $3 billion, doubling the $1.5 billion generated in 2025, supported by an ad-client base that has expanded 70% year-over-year to 4,000+ brands.

- The $2.8 Billion Warner Bros. Breakup Fee: After walking away from an expensive and legally precarious bid to acquire assets from Warner Bros. Discovery (WBD), Netflix pocketed a massive $2.8 billion buyout termination fee. This cash windfall supercharged Q1 free cash flow to $5.094 billion and prompted management to raise full-year 2026 FCF guidance to an impressive $12.5 billion.

- The YouTube and Amazon Engagement Squeeze: KeyBanc Capital Markets has flagged structural risks to long-term pricing power and user engagement. YouTube has actively captured peak screen time, averaging 99.1 daily viewing minutes across major markets versus Netflix’s 93.4 minutes, while Amazon Prime Video continues to leverage its bundled e-commerce ecosystem and superior ad-tech infrastructure.

- The Jay Hoag Chairman Ascension: Following the annual shareholder meeting on June 4, 2026, co-founder and streaming pioneer Reed Hastings officially stepped off the board to focus on philanthropy. Jay Hoag, a partner at TCV and a board member since 1999, has assumed the Chairman role, completing a generational leadership transition alongside co-CEOs Ted Sarandos and Greg Peters.

- Aggressive Share Buyback Execution: Bolstered by structural cash generation, the Netflix capital-return machine has restarted aggressively. The company enters the second half of 2026 with $6.8 million remaining on its current multi-billion-dollar share repurchase authorization, providing a robust corporate safety net below the equity during macro drawdowns.

What Is Netflix (NFLX)?

Netflix Inc. (NFLX) is the world's leading premium subscription streaming entertainment service, operating a global platform that commands over 325 million paid memberships across more than 190 countries. Moving away from its historical stance against platform commercialization, Netflix has restructured its business model to operate on a hybrid foundation: a premium ad-free tier and a budget-friendly, highly scalable ad-supported tier.

As of mid-2026, Netflix represents the benchmark for digital entertainment monetization. Rather than operating purely as a traditional media studio, the company relies heavily on machine learning recommendation engines, specialized mood-based content tailoring algorithms, and optimized programmatic ad-delivery software to maximize customer retention and lower user churn metrics.

Netflix's Performance in Early 2026: The Post-Earnings Repricing

Netflix kicked off the spring by reporting its fiscal first-quarter financial results on April 16, 2026. Top-line revenue surged 16.1% year-over-year to reach $12.25 billion, narrowly beating Wall Street consensus estimates of $12.17 billion. The underlying financial profile revealed pristine operating leverage, as quarterly operating income expanded 18.2% to $3.957 billion, keeping full-year operating margin guidance firmly on track for an expanded 31.5% target.

However, a complex bottom-line print triggered institutional repricing. While diluted earnings per share (EPS) printed at $1.23, the headline figure missed the core Wall Street estimate of $1.345 when factoring out the non-recurring impact of the $2.8 billion Warner Bros. termination fee. Furthermore, management’s decision to maintain, rather than raise, full-year revenue guidance between $50.7 billion and $51.7 billion disappointed momentum investors who had priced in immediate growth acceleration from recent monthly subscription price hikes.

This guidance friction, compounded by a back-weighted content slate heavy on H2 2026 releases, caused the stock to undergo a sharp valuation contraction from its spring consolidations down to its early June support zone.

Netflix's 2026 Trading Strategy: NFLX Traders to Navigate Volatility Multiples

- The $75 – $80 Structural Support Floor: Technical traders note that the $75 to $80 zone represents a formidable long-term horizontal support base. This area aligns closely with the macro lows established in February 2026. As long as weekly candle closes hold above $75, the long-term structural framework remains neutral-to-bullish.

- Compression to Value-Stock Valuation: Historically valued at triple-digit multiples, Netflix's trailing price-to-earnings (P/E) ratio has compressed significantly to 25.7x, putting it squarely in line with the broader entertainment industry average. Trading at roughly 22 to 23 times forward earnings estimates, the stock is showing deep fundamental value support, though it continues to experience technical friction from high-beta market rotations.

- Amortization Cycles and the Margin Cap: Traders must closely evaluate the second-quarter content amortization schedule. With significant production costs set to hit the balance sheet in the first half of the year, short-term operating margins face brief headwinds before the blockbuster content cycle scales up in late Q3 and Q4.

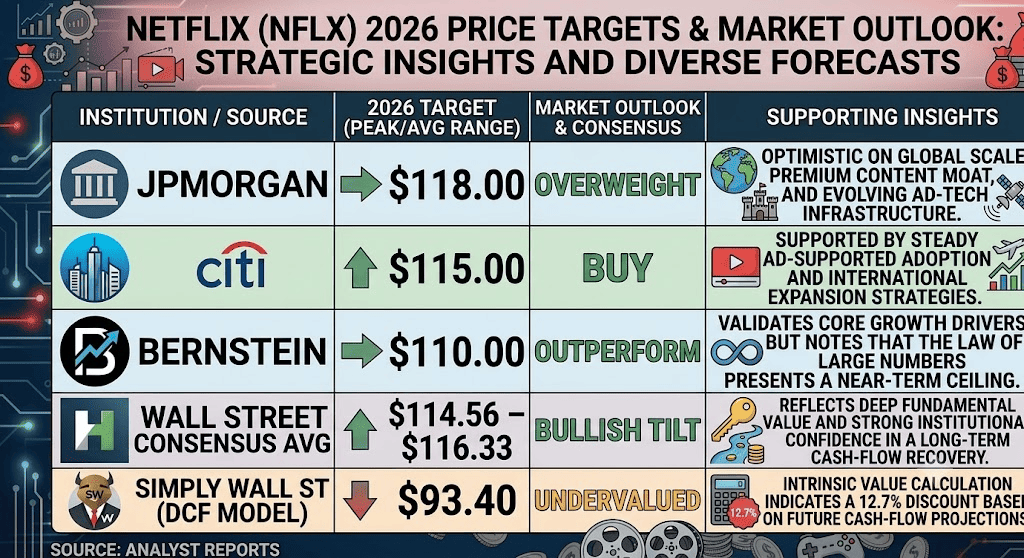

Netflix 2026 Stock Forecast: $116 Street-High Peak vs. $75 Macro Breakdown Trap

Wall Street analyst forecasts for Netflix stock in 2026

Evaluating Netflix’s trajectory for the remainder of 2026 requires balancing its unparalleled cash-generation capabilities against intense digital ad-market competition and slowing subscriber growth in hyper-mature Western regions.

The Bull Case: NFLX Stock's $116+ Ad-Tier Dominance and Multiple Expansion

The bullish thesis hinges on the successful scale-out of Netflix's programmatic advertising ecosystem. Championed by constructive Wall Street price targets from Citi ($115) and JPMorgan ($118), this narrative presumes that the introduction of advanced creator-focused AI tools and personalized ad formats will significantly drive up average revenue per user (ARPU) without triggering subscriber defections.

In this scenario, live marquee events, such as the upcoming NFL Christmas Day broadcasts and WWE Raw programming, will serve as massive user acquisition channels. If the ad tier systematically matches or exceeds the $3 billion targeted revenue milestone while preserving steady mid-teens subscriber growth in emerging markets, Netflix's forward P/E is highly likely to expand back toward 30x, propelling the equity past near-term resistance levels toward the Wall Street consensus high of $116.33.

The Base Case: $80 – $95 Consolidation Plateau for Netflix Stock

The base case outlines a prolonged accumulation phase where Netflix functions primarily as a highly profitable digital utility. Under this framework, top-line revenue scales at a sustainable 12% to 14% annual rate as the password-sharing crackdown benefits fully mature, and price increases stabilize existing domestic revenue pools.

However, the upside remains capped due to a highly competitive landscape for living-room screen time. As Amazon Prime Video leverages its bundled shopping memberships and YouTube dominates overall watch-time statistics, Netflix will likely trade within a well-defined horizontal channel between $80 and $95. Institutional capital will treat the asset as a defensive cash-flow play rather than an aggressive engine of explosive growth.

The Bear Case: NFLX's $75 Margin Trap and Structural Slowdown

The bearish outlook focuses on structural margin decay and competitive market share losses. If the ad-supported tier begins cannibalizing the high-margin premium ad-free subscription base, or if programmatic ad-spending slows down due to broader macroeconomic headwinds, Netflix's operating margins could fall short of the targeted 31.5%.

This downside risk is exacerbated by rising content acquisition and live-sports rights fees, which could trigger a costly bidding war against deep-pocketed tech entities like Apple and Alphabet. If global subscriber growth drops into the single digits or triggers net deflections following recent subscription hikes, a technical break below the critical $75 structural support line would invalidate the bullish recovery narrative, exposing NFLX to a steep valuation drop toward multi-year macro lows.

Netflix (NFLX) Stock Prediction for 2026 by Wall Street Analysts

|

Institution / Source |

2026 Price Target (Peak / Avg) |

Overall Market Outlook |

|

JPMorgan |

$118.00 |

Overweight: Optimistic on global scale, premium content moat, and evolving ad-tech infrastructure. |

|

Citi |

$115.00 |

Buy: Supported by steady ad-supported adoption and international expansion strategies. |

|

Bernstein |

$110.00 |

Outperform: Validates core growth drivers but notes that the law of large numbers presents a near-term ceiling. |

|

Wall Street Consensus Avg |

$114.56–$116.33 |

Bullish Tilt: Reflects deep fundamental value and strong institutional confidence in a long-term cash-flow recovery. |

|

Simply Wall St (DCF Model) |

$93.40 |

Undervalued: Intrinsic value calculation indicates a 12.7% discount based on future cash-flow projections. |

How to Trade Netflix (NFLX) Stock Futures on BingX TradFi

NFLX/USDT perpetuals on BingX futures market

As Netflix navigates this critical period of monetization scaling and macro asset allocation shifts, tactical traders can seamlessly capitalize on its short-term price action using the BingX platform and BingX AI-powered automated analysis:

- Access BingX TradFi: Navigate to the specialized TradFi section on your main BingX exchange account dashboard.

- Select Netflix (NFLX): Search for and select the NFLX-USDT perpetual futures contract.

- Choose Your Direction: Select Open Long if you believe the expanding ad-tier scale, share buybacks, and live-sports push will drive the equity back toward the $116 consensus target. Select Open Short to capitalize on the YouTube/Amazon engagement pressure and potential margin pullbacks.

- Configure Leverage and Margin Parameters: Apply your preferred Isolated or Cross-Margin settings along with appropriate, conservative leverage to optimize capital efficiency.

- Implement Robust Risk Management: Utilize advanced BingX Take-Profit and Stop-Loss (TP/SL) orders to systematically protect your capital against abrupt market gaps during pre-market and after-hours trading sessions.

Top 5 Risks to Consider Before Investing in NFLX Stock

While Netflix's premium position and pristine cash flow present a highly compelling value narrative, managing risk demands a thorough evaluation of its operational headwinds:

- Sustained Big Tech Competition: Deep-pocketed competitors like Amazon Prime Video, Alphabet's YouTube, and Apple are aggressively scaling content budgets, threatening Netflix's historical dominance over daily watch time.

- Ad-Tier Cannibalization Vulnerabilities: There is a persistent structural risk that cheaper ad-supported tiers could inadvertently pull users away from higher-priced, higher-margin premium subscription plans.

- Escalating Production and Sports Rights Costs: Branching into live broadcasts, video podcasts, and live sporting events exposes Netflix to volatile and highly capital-intensive licensing environments.

- Diminishing Password-Crackdown Returns: The phenomenal subscriber and revenue gains achieved via the password-sharing clampdown between 2023 and 2025 have largely run their course, limiting future incremental benefits.

- Macro Volatility and Beta Exposure: Carrying an elevated beta profile, NFLX remains highly sensitive to broader market selloffs, consumer discretionary spending cutbacks, and international currency fluctuations.

Final Thoughts: Is Netflix (NFLX) Stock a Buy in 2026?

As of June 2026, Netflix presents an intriguing transition from a volatile, pure-play growth equity into a highly disciplined, cash-generating media utility. Fundamentally, the platform's unique capability to clear over $12 billion in quarterly revenue while scaling annual free cash flow toward a targeted $12.5 billion highlights an incredibly durable operational model.

For short-term tactical traders, the stock's recent consolidation near major horizontal support zones provides an optimal setup for volatility capture and range trading via BingX perpetual futures. Long-term investors, conversely, must carefully evaluate if the accelerating $3 billion ad-revenue stream can successfully outpace the rising costs of live-content acquisition and the aggressive attention-share grab by major Big Tech platforms.

Risk Reminder: Trading global blue-chip equities involves substantial capital risk due to shifting consumer behaviors, platform development costs, and macro sector rotations. Always practice strict position sizing, disciplined capital preservation strategies, and mandatory risk mitigation protocols.

Related Reading

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?