In early June 2026, MP Materials Corp. (NYSE: MP) has become one of the most closely watched U.S. rare earth stocks. The company operates Mountain Pass, the only active large-scale rare earth mine in the Western Hemisphere, and is building a vertically integrated mine-to-magnet supply chain for defense, EVs, AI hardware, and advanced manufacturing.

The bull case is built on MP's U.S. rare earth monopoly position, a U.S. Department of Defense partnership with a $110/kg NdPr price floor, a $500 million Apple recycling partnership, secured offtake from Apple and General Motors, and the 10X Northlake magnet campus targeting nearly 10,000 metric tons of annual NdFeB magnet output by 2028. The risk is that MP already trades at a rich valuation while executing several complex facility ramps at the same time. This guide breaks down the MP Materials stock forecast, 2026 price scenarios, key risks, and how to trade MP stock futures on BingX TradFi with USDT collateral.

Key Catalysts That Could Affect MP Materials (MP) Stock in 2026

MP Materials' 2026 setup is shaped by the market's reassessment of the company from a rare earth miner into a strategic U.S. mine-to-magnet platform. The major catalysts are no longer just rare earth commodity prices, but government support, commercial offtake, magnet production execution, and U.S.-China supply chain policy.

- The DoD partnership gives MP a policy-backed demand floor: In July 2025, the U.S. Department of Defense agreed to buy $400 million of MP preferred stock, making the Pentagon the company's largest shareholder. The broader agreement also supports the 10X magnet facility and reflects Washington's push to reduce dependence on China for rare earth magnets. This gives MP a strategic policy premium, but it also means investors will watch government funding, procurement execution, and defense demand closely.

- Apple adds commercial validation beyond defense: Apple announced a $500 million commitment to buy American-made rare earth magnets from MP, with magnets expected to come from MP's Fort Worth facility and recycling work tied to Mountain Pass. The deal helped confirm that MP's magnet strategy is not only a defense story, but also a commercial supply chain story linked to consumer electronics and U.S. manufacturing.

- The 10X Northlake campus is the biggest execution test: MP's planned 10X facility in Northlake, Texas, is expected to require more than $1 billion in investment and target about 10,000 metric tons of annual rare earth magnet production when fully built. This could materially expand MP's downstream revenue base, but it also raises execution risk because the company must scale magnet manufacturing, manage costs, and deliver on customer commitments over several years.

- Q1 2026 results support the ramp, but the next quarters matter more: MP's Q1 2026 results showed stronger revenue and early Magnetics Segment contribution, suggesting the mine-to-magnet transition is gaining traction. The key question for the rest of 2026 is whether Independence magnet shipments, heavy rare earth separation progress, and EPS improvement can continue without major delays or margin pressure.

- China rare earth policy remains a major swing factor: MP benefits when U.S. policymakers and companies prioritize domestic rare earth supply chains. If China tightens export controls or U.S. defense rules become stricter, MP's strategic value could rise. If trade tensions ease or rare earth prices weaken, part of the geopolitical premium in the stock could compress.

Read More: How to Trade Commodities With Crypto in 2026 as Oil, Gold, Silver, and TradFi Go On-Chain

What Is MP Materials (NYSE: MP)?

MP Materials Corp. (NYSE: MP) is a Las Vegas-based rare earth materials and magnetics company founded in 2017. The company acquired the Mountain Pass rare earth mine in San Bernardino County, California, and became public in 2020.

Mountain Pass is the only active large-scale rare earth mining and processing operation in the Western Hemisphere. It produces neodymium-praseodymium (NdPr) oxide, a key input for neodymium-iron-boron (NdFeB) magnets. These magnets are used in EV motors, wind turbines, defense systems, robotics, smartphones, and hard drive components inside data center storage infrastructure.

MP operates through two main segments. The Materials Segment covers rare earth mining, separation, and NdPr oxide production at Mountain Pass. The Magnetics Segment covers NdPr metal production and NdFeB permanent magnet manufacturing at the Independence facility in Fort Worth, Texas. The company's long-term strategy is to move from mining and oxide separation into a fully integrated U.S. rare earth-to-magnet platform.

Read More: Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

MP Materials' Performance in Early 2026: From Mine Ramp to Magnetics Revenue

MP entered 2026 in the middle of its most important operational transition. After stopping sales to China in July 2025 under the DoD agreement, the company had to replace its former concentrate revenue stream with higher-value NdPr oxide, metal, and magnet sales.

Q4 2025 revenue declined 14% year over year to $52.7 million as the China sales exit hit before the NdPr ramp fully offset it. Still, the quarter delivered $0.09 EPS against a $0.02 consensus estimate and marked the first commercial NdFeB magnet production at Independence. Full-year 2025 revenue reached $275.5 million, up 35%, while NdPr oxide production hit a record 2,599 metric tons.

Q1 2026 confirmed the transition is gaining traction. Revenue rose 49% year over year to $90.6 million, Materials Segment adjusted EBITDA improved by $33 million, and Magnetics Segment revenue reached $18.4 million. MP also had about $2 billion in cash and short-term investments against roughly $1 billion in debt. The next key checkpoint is the July 30, 2026 Q2 earnings report, where investors will watch Independence shipment volumes, heavy rare earth separation progress, and Q3 EPS guidance.

MP Materials' 2026 Trading Strategy: Mine-to-Magnet Execution Drives the Setup

MP's 2026 setup depends on three key signals: whether Independence magnet revenue accelerates in H2 2026, whether Mountain Pass heavy rare earth separation commissions on schedule, and whether earnings continue tracking toward the full-year EPS target.

- Watch the $58 to $65 Support Zone: After rallying from around $50 in early April to above $63 after Q1 earnings and analyst upgrades, MP has built a key consolidation zone around $58 to $65. A hold above $62 into Q2 earnings would support the case for another move toward the $80 to $90 analyst target range. A break below $55 could trigger selling toward $45 to $48 if investors start questioning the magnet ramp or valuation.

- Defense and Commercial Premium vs. Materials Valuation Risk: The bull case values MP as the only vertically integrated U.S. rare earth-to-magnet platform, backed by a DoD price floor, Apple and GM offtake, and the January 2027 DFARS demand catalyst. The cautious case is that MP still trades at a high sales multiple, remains early in its magnet revenue ramp, and must execute several large facilities without major delays or cost overruns.

- AI Data Center and Robotics Demand Could Add Upside: Most MP coverage still focuses on EVs and defense. However, NdFeB magnets are also used in hard drive voice coil actuators, AI data centers, AI storage infrastructure, servo motors, robotics, and automation systems. If AI infrastructure and robotics demand grow faster than expected, MP's long-term magnet demand could be broader than current consensus models assume.

Read More:Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

The MP Materials 2026 Forecast: $90+ Defense and AI Upside vs. $45 Execution Risk Floor

MP's 2026 outlook depends on whether the company can scale Independence magnet shipments, commission heavy rare earth separation at Mountain Pass, and keep earnings on track while the market prices in defense, Apple, GM, and 10X upside.

The Bull Case: H2 Magnet Revenue Acceleration Pushes MP Above $90

The bull case requires Independence magnet shipments to accelerate in Q3 and Q4, Q2 earnings to confirm the EPS trajectory, and Mountain Pass heavy rare earth commissioning to support dysprosium and terbium production for high-performance magnets. If MP shows clear progress on commercial magnet volumes and confirms that Apple, GM, and DoD demand can absorb future output, the stock could move toward $90 to $94. The January 2027 DFARS deadline would add another demand catalyst because defense contractors must shift away from Chinese-origin rare earth magnets.

Read More: Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

The Base Case: Steady Execution Keeps MP Between $62 and $80

The base case assumes disciplined execution without a major new re-rating before Q4. Independence ramps shipments gradually, heavy rare earth separation begins on schedule, and the 10X Northlake project proceeds without major cost surprises. In this scenario, MP could consolidate between $62 and $80 as investors wait for Q3 and Q4 results to confirm whether magnet margins justify the current premium valuation.

The Bear Case: Facility Delays Pull MP Toward $45

The bear case is driven by Independence shipment delays, higher-than-expected ramp costs, weak Q2 earnings, or slower heavy rare earth commissioning. If investors shift back to valuing MP mainly on its current Materials Segment earnings rather than its future magnet platform, the stock could fall toward $45 to $50. A broader rare earth sentiment reset, lower NdPr prices, or easing China export restrictions could also reduce the geopolitical premium in the stock.

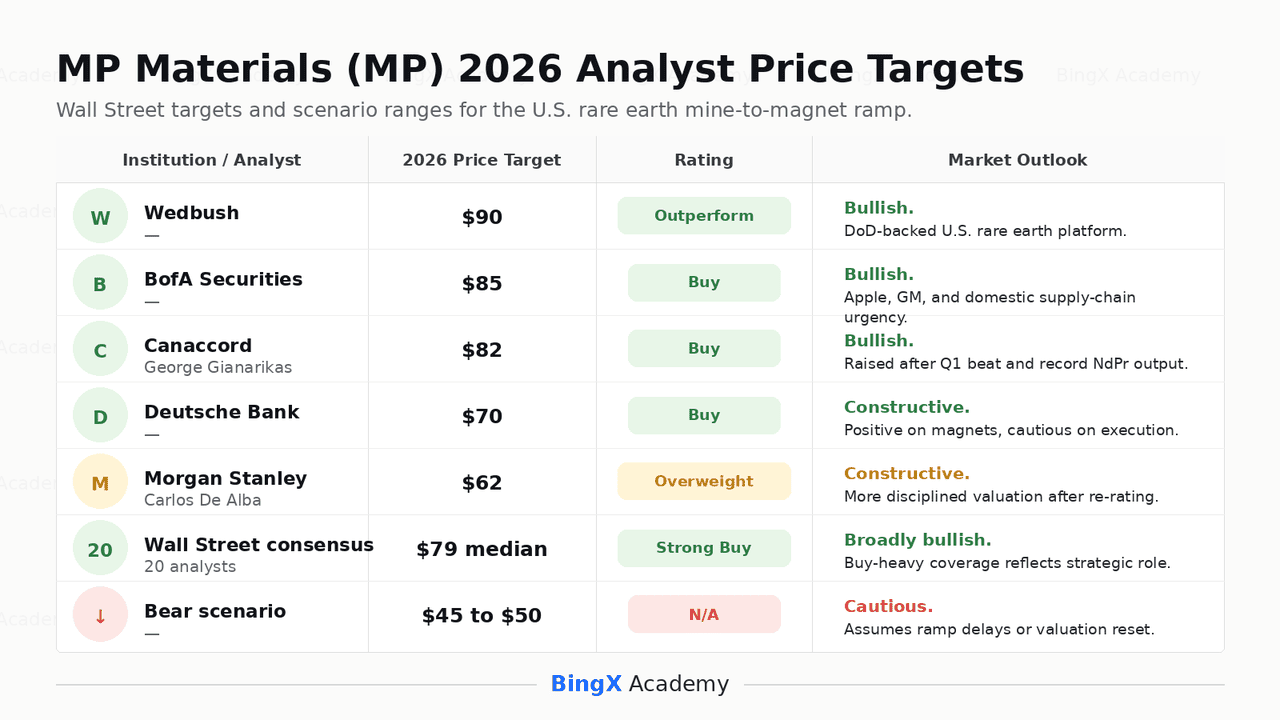

MP Materials Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Analyst |

2026 Price Target |

Rating |

Market Outlook |

|

Wedbush |

$90 |

Outperform |

Bullish. Wedbush sees MP as a vertically integrated U.S. rare earth mine-to-magnet platform, with the DoD partnership reducing commodity and demand risk. |

|

BofA Securities |

$85 |

Buy |

Bullish. BofA highlights MP's structural insulation from China rare earth risk and the urgency of domestic rare earth supply chain development. |

|

Canaccord / George Gianarikas |

$82 |

Buy |

Bullish. Canaccord raised its target after the Q1 2026 beat, citing record NdPr production, stronger revenue, and EPS upside. |

|

Deutsche Bank |

$70 |

Buy |

Constructive. Deutsche Bank acknowledges the Q1 beat and magnet segment progress, but applies a more conservative view due to multi-facility execution risk. |

|

Morgan Stanley / Carlos De Alba |

$62 |

Overweight |

Constructive but more cautious. Morgan Stanley recognizes the DoD-backed domestic supply chain thesis, but uses a more disciplined valuation framework after the stock's rally. |

|

Wall Street consensus |

$79 median |

Strong Buy |

Broadly bullish. Analyst coverage shows unusually strong support, reflecting MP's strategic position, government backing, and DFARS demand catalyst. |

|

Bear scenario |

$45 to $50 |

N/A |

Cautious. This scenario assumes magnet ramp delays, weaker Q2 earnings, and a valuation reset toward the current Materials Segment rather than future 10X upside. |

How to Trade MP Materials (MP) Stock Futures on BingX TradFi

As MP Materials navigates Independence magnet production, Mountain Pass heavy rare earth commissioning, 10X Northlake construction, and the January 2027 DFARS demand deadline, tactical traders can trade MP stock futures on BingX TradFi using USDT collateral.

Step 1: Access BingX TradFi. Sign up and navigate to the specialized TradFi section on the main BingX exchange dashboard.

Step 2: Select MP Materials (MP). Search for and select the MPUS-USDT perpetual futures contract.

Step 3: Choose your direction. Select Open Long if you expect MP Q2 earnings to confirm the EPS trajectory, Independence magnet shipments to scale, and the DFARS demand catalyst to remain intact. Open short if you expect earnings disappointment, facility ramp delays, margin pressure, or valuation compression after MP's strong rally.

Step 4: Select leverage and margin mode. Choose Isolated or Cross-Margin based on your risk tolerance. MP can move sharply around earnings, rare earth policy headlines, DoD updates, and China export control developments, so conservative leverage and clear position sizing are important.

Step 5: Use TP/SL controls. Set Take-Profit and Stop-Loss (TP/SL) levels before or immediately after entering the trade. MP can react quickly to Q2 earnings, NdPr price moves, DFARS implementation updates, China rare earth policy changes, and facility ramp disclosures.

Top 5 Risks to Consider Before Investing in MP Materials Stock

MP Materials has one of the strongest strategic positions in the U.S. rare earth sector, but MP still carries risks tied to execution complexity, valuation, government funding, insider activity, and China policy sensitivity.

- Three facility ramps create execution risk: MP is scaling Independence magnet production, commissioning heavy rare earth separation at Mountain Pass, and building the 10X Northlake campus at the same time. Any delay or cost overrun could pressure the stock because the current valuation assumes smooth execution across all three programs.

- Valuation is already rich: MP trades at a high price-to-sales multiple and remains loss-making on a net income basis despite the Q1 EPS beat. If magnet ramp costs are higher than expected or revenue misses the path implied by the full-year EPS target, multiple compression could be sharp.

- DoD support still carries government risk: The DoD partnership is central to MP's investment case, but it depends on policy continuity, budget support, and procurement execution. Any change in defense spending priorities or rare earth procurement rules could affect the value of the price protection structure.

- Insider selling may weigh on sentiment: CEO James H. Litinsky sold shares near the $64 level under pre-scheduled 10b5-1 plans. While these sales do not necessarily signal a negative view, insider selling near multi-year highs can still affect market sentiment.

- China rare earth policy can move the stock both ways: MP benefits from the urgency created by China export restrictions and U.S. supply chain policy. If tensions escalate, MP could gain further geopolitical premium. If restrictions ease or rare earth prices fall, part of that premium could compress.

Final Thoughts: Is MP Materials Stock a Buy in 2026?

As of June 2026, MP Materials (MP) is one of the most strategically important industrial stocks in the U.S. market. Its position as the only large-scale rare earth miner in the Western Hemisphere, combined with the DoD price floor, Apple and GM offtake, the 10X Northlake magnet campus, and the January 2027 DFARS deadline, gives MP a rare combination of policy support and commercial demand.

The risk is execution and valuation. MP is no longer priced like a simple materials company. The market is already assuming that Independence magnet shipments scale, Mountain Pass heavy rare earth separation begins on schedule, and 10X construction stays on track. For active traders, MP futures on BingX TradFi offer a way to trade around Q2 earnings, facility ramp updates, and rare earth policy headlines. For longer-term investors, the key question is whether MP can turn its strategic position into sustained magnet revenue and earnings growth without major execution setbacks.

Related Reading

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- USA Rare Earth (USAR) Stock Outlook 2026: Can Magnet Production Drive USAR Above $45?

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Top AI Memory Stocks to Buy in 2026: DRAM, HBM, and AI Storage Demand Explained

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders