In late June 2026, Ford Motor Company (NYSE: F) finds itself positioned at an extraordinary strategic crossroads, transforming from a traditional internal combustion engine (ICE) builder into an agile commercial software and AI-adjacent infrastructure play. Following a massive 45% vertical surge in May 2026, the Dearborn-headquartered automaker is currently trading near $14.11, logging a highly resilient 14.4% year-to-date gain and significantly outperforming the broader consumer discretionary sector.

While the equity spent the past two fiscal years absorbing severe financial punishment, punctuated by a massive $19.5 billion write-down from restructured electric vehicle (EV) operations that wiped out its 2025 earnings, back-to-back operational breakthroughs have fundamentally re-engineered Ford's long-term revenue outlook. Investors are aggressively weighing an exceptionally strong fiscal first-quarter earnings report against immediate macroeconomic headwinds, supply disruptions, and pivotal Canadian labor talks.

As the global technology ecosystem experiences a massive supply bottleneck for AI data center power infrastructure, Ford's surprise entry into grid-scale battery manufacturing has completely changed the institutional narrative. However, acute materials shortages and near-term vehicle sales softness continue to present a persistent valuation overhang.

This guide breaks down the Ford Motor Company stock forecast and price prediction for the remainder of 2026, utilizing data from Morgan Stanley, Barclays, JPMorgan, Morningstar consensus estimates, and official financial disclosures.

You will also discover how to trade Ford Motor Co. (F) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Ford (F) Traders to Know in 2026

As Ford navigates a high-stakes environment of corporate reorganization and infrastructure scaling, traders must closely monitor these five market-moving factors:

- The Ford Energy AI Data Center Play: In May 2026, Ford officially launched its Ford Energy subsidiary, repurposing its idle Kentucky battery plant to build grid-scale Battery Energy Storage Systems (BESS). Its flagship product, the shipping-container-sized Ford Energy DC Block, targets data centers and utilities struggling to power the generative AI boom.

- The 20 GWh EDF Power Solutions Contract: Validating immediate commercial demand, Ford signed a five-year supply agreement with EDF Power Solutions for up to 4 gigawatt-hours (GWh) of annual storage capacity, totaling up to 20 GWh over the contract term. Deliveries are scheduled to begin in 2028.

- The $1.3 Billion Supreme Court Tariff Windfall: A landmark U.S. Supreme Court ruling in February 2026 struck down certain trade tariffs, handing Ford a $1.3 billion paper gain in Q1 2026. This massive refund powered a blowout adjusted earnings per share (EPS) print of $0.66, vastly exceeding Wall Street consensus estimates of just $0.20.

- The Novelis Aluminum Fire & Supply Shock: Ford’s core profit engine, the aluminum-intensive F-150 pickup line, suffered a severe supply blow following two devastating fires at its primary materials supplier, Novelis. The disruption triggered a 12% year-over-year drop in F-Series first-quarter production and an acute 38% collapse in April dealer inventory.

- The Unifor Labor Confrontation: On June 22, 2026, Unifor officially launched high-stakes contract negotiations on behalf of 5,150 Canadian autoworkers at Ford facilities. As the chosen pattern-setting automaker for the Detroit Three negotiations, Ford faces a strict July 10, 2026, strike deadline amid a complex global trade environment.

What Is Ford Motor Company (F)?

Ford Motor Company (NYSE: F) is a premier global automaker responsible for designing, manufacturing, and servicing an expansive lineup of commercial vans, trucks, SUVs, and luxury Lincoln vehicles. Under its comprehensive Ford+ corporate strategy, the company has segmented its operations into distinct, highly specialized reporting units to optimize execution:

|

Business Unit |

Core Operational Mandate |

|

Ford Pro |

The high-margin commercial fleet, software, and telematics division serving contractors and industrial operators. |

|

Ford Blue |

The traditional core vehicle portfolio focused on internal combustion engines (ICE) and high-demand hybrid architectures. |

|

Ford Model e |

The advanced technology hub managing electric vehicle software development, digital architectures, and connectivity. |

|

Ford Energy |

The newly formed 2026 energy storage segment manufacturing utility-scale battery systems using licensed CATL cell technology. |

As of mid-2026, Ford is aggressively leveraging its deep industrial scaling capacity, automated assembly footprint, and advanced battery joint ventures to position itself as a key supplier to both the commercial automotive sector and the rapidly expanding AI data center grid market.

Ford's Performance in Early 2026: The Post-Earnings Repricing

Ford kicked off the spring of 2026 by reporting standout first-quarter financial results on April 29. Corporate revenue climbed to $43.3 billion, achieving a robust 6% year-over-year expansion. Adjusted Earnings Before Interest and Taxes (EBIT) surged to $3.5 billion, representing an 8.1% operating margin, a massive rebound from the negative operating territory recorded during the peak of the 2025 EV restructuring charges.

While the headline bottom line was significantly flattered by the $1.3 billion one-time tariff refund, Ford’s core commercial division, Ford Pro, demonstrated exceptional structural strength, generating $1.7 billion in EBIT at a stellar 11.4% profit margin. Furthermore, the loss-heavy Model e segment showed signs of stabilizing, narrowing its quarterly operating loss to $777 million. Citing this underlying structural momentum, management confidently upgraded its full-year 2026 adjusted EBIT guidance to a range of $8.5 billion to $10.5 billion, up from its initial $8.0 billion to $10.0 billion projection.

Ford's 2026 Trading Strategy: Navigating Volatility Multiples

- The $13.10 Structural Support Floor: From a technical perspective, market analysts point to the $13.10 to $13.50 structural window as a vital horizontal support zone. On weekly candle intervals, keeping price action firmly above this level preserves the broader macro-recovery path initiated during the massive May volume breakout.

- The Reorganization Alpha: In April 2026, Chief Operating Officer Kumar Galhotra assumed full leadership of the newly unified Product Creation and Industrialization division. By merging engineering, manufacturing, purchasing, and advanced software-defined vehicle (SDV) blueprints under one command following the departure of veteran executive Doug Field, Ford expects to slash vehicle development cycles and aggressively scale its next-generation, low-cost Universal Electric Vehicle (UEV) platform.

- Dividend Yield Cushioning: Trading at a forward price-to-earnings (P/E) ratio of roughly 8x to 10x relative to full-year 2026 EPS expectations of $1.64 to $1.84, Ford offers an incredibly robust dividend yield between 4.1% and 5.2% ($0.15 quarterly). For macro-focused traders, this rich yield acts as a formidable capital floor during broader market retracements.

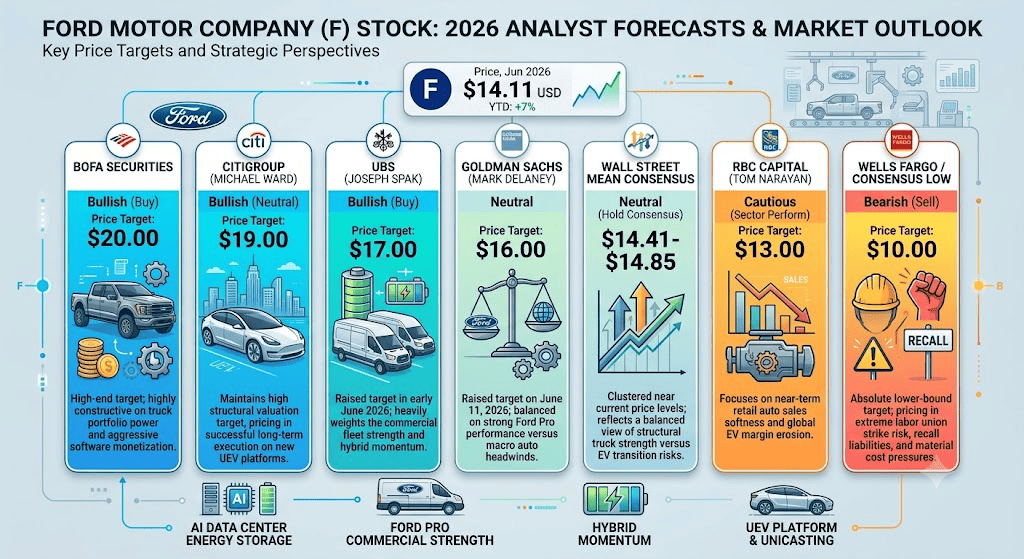

Ford 2026 Stock Forecast: $20.00 Street-High Peak vs. $10.00 Production Recall Trap

Evaluating Ford’s forward equity trajectory requires balancing a high-margin commercial fleet monopoly and an exponential AI grid infrastructure opportunity against near-term industrial supply shocks, traditional automotive recall liabilities, and localized institutional adjustments.

The Bull Case for Ford Motor: The $17.00 – $20.00 Energy Re-Rating and Commercial Monopoly

The bullish thesis is anchored on Ford successfully executing its transformation into a dual-engine energy and commercial technology company. Supported by specific June 2026 institutional revisions, including UBS raising its target to $17.00 with a Buy rating, Citigroup maintaining a $19.00 target, and BofA Securities pushing the street-high ceiling to $20.00, this path assumes that Morgan Stanley's $10 billion standalone valuation for the Ford Energy subsidiary becomes fully priced into the market cap.

In this scenario, Ford rapidly secures additional high-volume, utility-scale BESS contracts with global cloud hyperscalers seeking immediate power capacity for their AI semiconductor clusters. Concurrently, the newly consolidated product organization successfully rolls out its ultra-cheap, highly casted (unicasting) UEV mid-size pickup truck featuring proprietary low-cost electric motors. If full-year EPS aggressively outperforms the consensus and tracks toward the high end of estimates, the stock is heavily favored to break its 52-week resistance at $17.78 and trade toward the $17.00 to $20.00 institutional target zone.

Ford Stock's Base Case: $13.90 – $16.00 Consensus Consolidation Plateau

The base case envisions a prolonged consolidation phase where the market thoroughly digests Ford's massive $2 billion initial capital expenditure into the energy segment. Because actual physical deliveries of the containerized battery blocks do not commence until 2028, near-term stock performance remains heavily tethered to traditional automotive operational metrics and a strict 60–65% Wall Street "Hold" consensus. This is marked by major firms like Goldman Sachs raising its target to $16.00 while maintaining a Neutral stance, and RBC Capital reiterating a Sector Perform rating at $13.00.

Under this framework, full-year 2026 adjusted EPS settles into the consensus range of $1.64 to $1.70, with a Q2 target of $0.34 to $0.36 expected around the July 29, 2026 earnings print. Robust cash flows from the high-margin Ford Pro commercial segment and expanding paid software subscriptions effectively neutralize persistent macro headwinds. The equity remains bound within a tight horizontal consolidation range between $13.90 and $16.00, where explosive energy updates are routinely counterbalanced by softer month-over-month U.S. consumer retail sales data.

The Bear Case for F Stock: The $10.00 Supply Chain and Recall Margin Trap

The bearish outlook focuses on acute near-term margin compression and traditional legacy liabilities, a stance championed by Wells Fargo's early June 2026 Sell rating. If the production restarts at the fire-damaged Novelis aluminum facility experience prolonged delays stretching past the summer, Ford's inability to fulfill high-margin F-150 orders will heavily penalize its core bottom-line cash generation.

This operational risk is further amplified by immediate legacy headwinds: a massive mid-year U.S. vehicle recall affecting over 255,000 Focus models over critical engine defects is expected to drive up warranty expenses significantly. If Unifor negotiations break down leading to an extended strike at Canadian manufacturing hubs past the July 10 deadline, or if intense price wars in the global hybrid space compromise gross margins, a decisive breakdown below structural support would validate the street-low forecast, exposing the asset to a steep liquidation selloff toward Wells Fargo and RBC-aligned floors of $10.00 to $13.00.

Ford Motor Co. (F) Price Predictions for 2026 by Wall Street Analysts

|

Institution / Metric |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

BofA Securities |

$20.00 |

Bullish (Buy): High-end target; highly constructive on truck portfolio power and aggressive software monetization. |

|

Citigroup (Michael Ward) |

$19.00 |

Bullish (Neutral): Maintains a high structural valuation target, pricing in successful long-term execution on new UEV platforms. |

|

UBS (Joseph Spak) |

$17.00 |

Bullish (Buy): Raised target from $14.00 in early June 2026; heavily weights the commercial fleet strength and hybrid momentum. |

|

Goldman Sachs (Mark Delaney) |

$16.00 |

Neutral: Raised target from $13.00 on June 11, 2026; balanced on strong Ford Pro performance versus macro auto headwinds. |

|

Wall Street Mean Consensus |

$14.41 – $14.85 |

Neutral (Hold Consensus): Clustered near current price levels; reflects a balanced view of structural truck strength versus EV transition execution risks. |

|

RBC Capital (Tom Narayan) |

$13.00 |

Cautious (Sector Perform): Focuses on near-term retail auto sales softness and global EV margin erosion. |

|

Wells Fargo / Consensus Low |

$10.00 |

Bearish (Sell): Absolute lower-bound target; pricing in extreme labor union strike risk, recall liabilities, and persistent material cost pressures. |

How to Trade Ford Motor Company (F) Stock Futures on BingX TradFi

FUS/USDT perpetual contract on BingX futures market

As Ford navigates this period of intensive corporate restructuring and volatile energy headlines, tactical traders can seamlessly capitalize on both upward momentum and downward price swings through the specialized BingX platform.

- Access BingX TradFi: Log in to your account and navigate directly to the BingX TradFi section on the main BingX exchange platform interface.

- Select Ford Motor Company (F): Use the interactive search bar to locate and select the FUS-USDT perpetual futures contract.

- Choose Your Market Direction: Select Open Long if you believe the expanding grid-scale battery contracts and resilient commercial software margins will drive the stock toward its $19 to $20 targets. Select Open Short to capitalize on potential production setbacks, labor strike risks, or recall-driven pullbacks.

- Configure Your Position Parameters: Establish your preferred Isolated or Cross-Margin parameters and input highly disciplined leverage settings to maximize capital efficiency while mitigating asset volatility.

- Deploy Risk Management Protocols: Utilize the advanced, real-time BingX Take-Profit and Stop-Loss (TP/SL) tools to safely insulate your trading capital from unexpected headline gaps during high-impact corporate announcements.

Top 5 Risks to Consider Before Investing in Ford Stock

While Ford's entry into the AI data center grid-scale market presents a compelling narrative shift, navigating this industrial transition requires a cold, disciplined analysis of its underlying risk profile:

- Delayed Revenue Realization for Ford Energy: Despite drawing immense institutional hype and securing the 20 GWh EDF partnership, actual commercial product shipments do not commence until 2028, meaning the venture will remain a capital-absorbing cost center throughout 2026.

- Severe Aluminum Material Bottlenecks: The critical dependence on specialized aluminum sheets for the top-selling F-150 leaves Ford highly vulnerable to ongoing supplier disruptions, threatening production volumes of its primary cash-flow engine.

- Imminent Detroit Three Labor Strife: With Unifor establishing a strict July 10 contract deadline, any failure to rapidly resolve wage and pension disputes could trigger widespread factory shutdowns across Canadian facilities.

- Strained Automotive Cost Controls: Historically, Ford has struggled with elevated warranty expenses and structural cost overruns relative to core cross-town rivals like General Motors, limiting its ability to achieve premium equity multiples.

- Softening Consumer Retail Auto Demand: Broader macroeconomic headwinds and a structural cooling in retail hybrid and consumer EV adoption could depress core North American sales, increasing reliance on commercial fleets.

Final Thoughts: Is Ford Motor Company (F) Stock a Buy in 2026?

As of late June 2026, Ford Motor Company stands as one of the most intriguing and highly debated turnarounds in the large-cap cyclical landscape. Fundamentally, the company’s ability to generate over $43 billion in a single quarter while supporting a high-margin commercial software ecosystem proves its core enterprise relevance.

However, trading a legacy titan in the midst of a multi-billion-dollar energy pivot requires sharp operational timing. For short-term tactical traders, the equity provides an exceptional environment for high-liquidity volatility capture via BingX futures around key catalysts like the July labor deadline and late-July Q2 earnings. For long-term investors, the combinations of an 8x forward P/E multiple and a rock-solid 4%+ dividend yield offer a highly attractive risk-reward profile to get paid while waiting for the AI data center battery strategy to fully scale.

Risk Reminder: Trading equity derivatives and large-cap cyclical futures involves substantial capital risk due to macroeconomic fluctuations, complex supply chain dependencies, and unexpected labor adjustments. Always employ rigorous position sizing, clear risk targets, and hard stop-losses.

Related Reading

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Top Energy Stocks and ETFs to Buy in 2026: The AI Power Crunch Meets Geopolitical Volatility

- Aluminum (XAL) Price Prediction 2026: $4,000 Black Swan Peak or Macro Demand Destruction?