In mid-June 2026, Credo Technology Group Holding Ltd (CRDO) sits at a highly lucrative yet intensely scrutinized intersection of the global tech sector. Following a spectacular 78.4% vertical rally over the past three months, the semiconductor connectivity innovator and quantum computing stock is trading near $237.68, boasting a powerful 65.95% gain year-to-date.

While the equity experienced brief 'sell-the-news' volatility, dropping immediately after its June 1 earnings report due to sky-high market expectations, underlying fundamentals have dramatically re-rated the firm's long-term enterprise value. Investors are aggressively factoring in a massive fourth-quarter fiscal 2026 earnings beat against a backdrop of tight semiconductor supply chains and an unyielding artificial intelligence infrastructure investment cycle.

As hyperscalers rapidly transition from cluster testing to deploying hundreds of thousands of interconnected GPUs, raw compute power is no longer the sole industry constraint. Instead, data center efficiency has run headfirst into a massive structural bottleneck: network reliability, latency, and power consumption. Credo's specialized high-speed signaling solutions have positioned the company as an indispensable provider of the 'picks and shovels' powering modern AI data factories.

This guide provides a comprehensive breakdown of the Credo Technology Group stock forecast and price prediction for the remainder of 2026, utilizing real-time financial metrics, S&P Global Market Intelligence data, Zacks Rank analytics, and recent post-earnings target updates from Mizuho, Bank of America, and TD Cowen.

You will also discover how to trade Credo Technology Group Holding Ltd (CRDO) stock futures and spot equities on BingX TradFi using crypto-collateralized assets.

Top 5 Things for Credo Technology (CRDO) Traders to Know in 2026

As Credo navigates a high-stakes ecosystem of exponential corporate scaling and premium valuation assessments, market participants must closely track these five critical catalysts:

- The Core AEC Growth Engine: Active Electrical Cables (AECs) remain Credo’s primary revenue driver. Hyperscalers are broadly adopting Credo’s ZeroFlap AEC architectures because they deliver up to 1,000x higher network reliability while slashing power consumption by roughly 50% compared to short-reach optical alternatives in dense XPU clusters.

- The $600M Optical Business Inflection: Beyond copper-based cabling, management expects a massive second-half acceleration in fiscal 2027 driven by its expanding optical integrated circuit (IC) portfolio. Total optical revenue is projected to eclipse $600 million, with ZeroFlap optics, silicon photonics PICs, and optical DSPs each expected to scale past the $100 million annualized run-rate milestone.

- The DustPhotonics Integration: Credo’s strategic acquisition of DustPhotonics has fundamentally enhanced its high-speed optical connectivity roadmap. By embedding advanced silicon photonics' Photonic Integrated Circuit (PIC) technology, Credo is actively securing its place in upcoming 800G and 1.6T deployment cycles, while engineering future 3.2T solutions.

- Severe Hyperscaler Customer Concentration: Despite expanding its footprint to emerging Neocloud providers, Credo’s revenue remains tightly clustered. In its latest financial disclosures, four distinct hyperscale cloud service providers each accounted for over 10% of Credo’s total corporate revenue, presenting an inherent single-client spending risk.

- Stretched Valuation & High Beta Multiples: Trading at a trailing price-to-earnings (P/E) ratio of 94.73 and a forward price-to-sales (P/S) ratio of 15.48, CRDO commands a heavy premium relative to the electronic semiconductor sector average of 9.14. Combined with a highly sensitive 1-year beta of 3.2, the equity is highly exposed to any macro-driven AI capital expenditure cooling.

What Is Credo Technology Group (CRDO)?

Founded in 2008 and legally headquartered in the Cayman Islands with operational bases in San Jose, California, Credo Technology Group Holding Ltd provides breakthrough, high-speed connectivity solutions for the global data infrastructure market. The core architectural foundation of Credo’s product suite is its proprietary Serializer/Deserializer (SerDes) and Digital Signal Processor (DSP) technology stack.

Rather than focusing on raw compute processors like Nvidia or AMD, Credo designs the specialized hardware required to transport data between chips, switches, and servers at extreme optical and electrical speeds. Its commercial portfolio includes integrated circuits (ICs), retimers, optical DSPs, SerDes chiplets, intellectual property (IP) licensing solutions, and turnkey Active Electrical Cables (AECs) for Ethernet and PCIe applications worldwide.

Credo's Performance in Early 2026: The Post-Earnings Repricing

Credo Technology Group (CRDO) YTD stock performance as of June 2026 | Source: Google Finance

Credo concluded a defining fiscal year on June 1, 2026, by delivering a blowout fourth-quarter financial print. Quarterly revenue exploded to $437.0 million, achieving an outstanding 157% year-over-year growth rate that eclipsed the $431.8 million Wall Street consensus. Non-GAAP net income for the single quarter reached $277 million, yielding an adjusted earnings per share (EPS) of $1.16, comfortably beating the $1.02 institutional estimate.

|

Metric (FQ4 2026) |

Reported Value |

Wall Street Consensus |

YoY Growth |

|

Quarterly Revenue |

$437.0 million |

$431.8 million |

1.57 |

|

Non-GAAP EPS |

$1.16 |

$1.02 |

+13.6% (Beat) |

|

Full-Year Revenue |

$1.34 billion |

$1.33 billion |

2.05 |

|

Non-GAAP Gross Margin |

68.10% |

67.50% |

+310 bps |

For the full fiscal year 2026, Credo’s total revenue more than tripled to $1.34 billion, while non-GAAP gross margins expanded by 310 basis points to finish at 68.1%. Management capitalized on this momentum by issuing exceptionally strong guidance for the upcoming first quarter of fiscal 2027, projecting revenue between $465.0 million and $475.0 million alongside stable gross margins in the 67% to 69% range. This structural expansion pushed the stock to a pristine Zacks Rank #1 (Strong Buy) status.

Credo 2026 Trading Strategy: Navigating Volatility Multiples

- The $220 – $225 Near-Term Support Floor: Following post-earnings profit-taking, the $220 to $225 range has emerged as an essential psychological and structural demand zone. Technical traders monitor this boundary closely on daily charts, as keeping above this level preserves the broader, intermediate bullish continuation pattern.

- Evaluating the Cash Profile vs. Inventory Ramp: Credo maintains an incredibly strong cash position of approximately $1.4 billion, giving the company massive flexibility for product R&D and accretive M&A. However, traders should note that corporate inventory nearly tripled year-over-year. While management explains this as a necessary buildout to secure supply chain capacity for upcoming 1.6T customer deployments, it demands cautious monitoring to ensure top-line demand completely absorbs the backlog.

- Managing the 3.2 Beta Exposure: Boasting a beta of 3.2, CRDO exhibits price movements that are highly magnified relative to the benchmark indices. Traders must actively size their positions to withstand abrupt, intraday price fluctuations and after-hours headline risks typical of high-multiple, high-growth AI infrastructure equities.

Credo Stock Price Prediction 2026: $300 Street-High Peak vs. $172 Bear Trap

A balanced assessment of Credo’s trajectory requires pitting an undeniable, multi-year hyperscaler hardware upgrade cycle against a steep valuation profile that leaves minimal margin for operational error.

The Bull Case: Credo's $290 – $300 Multi-Gen Connectivity Monopoly

The bullish thesis assumes an uninhibited acceleration of hyperscaler and emerging Neocloud infrastructure capex. Championed by Mizuho analyst Vijay Rakesh, who raised his price target to $290 following the June earnings print, and high-end street estimates reaching $300, this scenario envisions Credo solidifying an effective monopoly over advanced cluster fabrics.

As cluster sizes scale past 100,000 XPUs, the operational costs of network failures make alternative copper or lower-grade optical interconnects financially unviable. If Credo completely monetizes its newly announced ZeroFlap optics, Active Line Cards (ALCs), and OmniConnect platforms simultaneously, revenue will effortlessly track toward the company’s internal 2029 target of $3.2 billion. This operational execution would justify further multiple expansion, driving CRDO past its $261.38 52-week high toward the psychological $300 marker.

The Base Case for CRDO Stock: $230 – $260 Consolidation Plateau

The base case points to a prolonged consolidation era where the market systematically pairs Credo's massive 26.9% annualized revenue growth forecast against its premium valuation. Backed by Bank of America’s $252 target and the macro Wall Street consensus average of $256.30, this outlook models a highly productive, range-bound trading landscape.

Under this framework, Credo smoothly delivers on its FQ1 2027 revenue guidance of up to $475 million, and gross margins remain comfortably anchored near 68%. However, broader market awareness of heavy customer concentration keeps a lid on the stock's forward earnings multiple. The asset consolidates its massive year-to-date gains, fluctuating between major structural support at $220 and near-term resistance at $260.

The Bear Case: CRDO's $172 Valuation Compression Trap

The bearish outlook focuses on potential structural speedbumps within the broader AI spending cycle. Highlighted by conservative forensic models like 24/7 Wall St. (which maintains an internal model target of $220.11 and a structural bear-case target of $172.10), this narrative focuses on rapid multiple contraction.

If major hyperscalers enact a temporary pause in cluster deployments to digest existing inventory, or if deeply entrenched competitors like Broadcom (AVGO), Marvell Technology (MRVL), or Astera Labs (ALAB) ignite an aggressive price war for hardware allocations, Credo’s highly concentrated revenue stream would feel immediate pressure. Given its elevated trailing P/E of 94.73, any minor guidance markdown or compression of gross margins below the targeted 67% baseline could trigger sharp, institutional liquidation, exposing the stock to a sharp drop toward the $172 support zone.

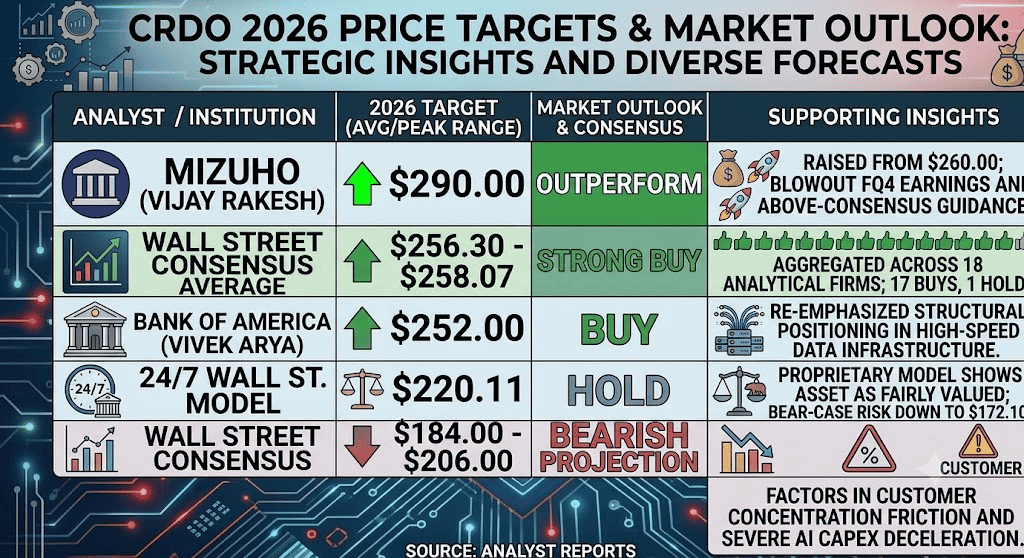

Credo Technology Group (CRDO) Price Forecasts for 2026 by Wall Street Analysts

|

Institution / Source |

2026 Price Target (Peak/Avg) |

Overall Market Outlook & Rating |

|

Mizuho (Vijay Rakesh) |

$290.00 |

Outperform: Raised target from $260 following a blowout FQ4 earnings report and above-consensus guidance. |

|

Wall Street Consensus Average |

$256.30 – $258.07 |

Strong Buy: Aggregated across 18 leading analytical firms; highlights 17 Buy ratings and 1 Hold rating. |

|

Bank of America (Vivek Arya) |

$252.00 |

Buy: Re-emphasized structural positioning within high-speed data infrastructure markets. |

|

24/7 Wall St. Model |

$220.11 |

Hold: Proprietary model implies the asset is fairly valued; outlines a bear-case risk target down to $172.10. |

|

Wall Street Consensus Low |

$184.00 – $206.00 |

Bearish Projection: Factors in customer concentration friction and severe AI capex deceleration. |

How to Trade Credo Technology (CRDO) Stock Futures on BingX TradFi

CRDO/USDT perpetual contract on BingX futures market

As Credo Technology Group navigates this volatile period of massive infrastructure deployments and high-volume earnings adjustments, tactical market participants can easily capture daily price trends via the advanced BingX platform.

- Access the Platform: Log into your account and navigate to the specialized TradFi / Stocks section on the main BingX exchange dashboard.

- Locate the Asset: Type in the ticker search bar and select the CRDO-USDT perpetual futures contract.

- Establish Your Market Direction: Choose Open Long if you believe expanding 1.6T optical portfolio deployments and strong hyperscaler traction will propel the asset to the $300 street-high target. Choose Open Short to capitalize on premium valuation adjustments and potential industry capex cool-downs.

- Configure Leverage and Margin Parameters: Set your preferred Isolated or Cross-Margin structures alongside disciplined, highly conservative leverage ratios to maximize capital allocation efficiency.

- Implement Risk Management Protocols: Deploy advanced BingX Take-Profit and Stop-Loss (TP/SL) tools to automatically shield your capital from sudden, news-driven market gaps during extended after-hours trading windows.

Top 5 Risks to Consider Before Investing in CRDO Stock

While Credo's exceptional revenue trajectory presents a highly enticing structural expansion narrative, building a position in this high-beta asset demands a thorough evaluation of these clear vulnerabilities:

- Pronounced Revenue Concentration: Relying on four core hyperscalers for over 40% of total inbound revenues leaves Credo exposed to localized corporate budget shifts or internal engineering re-allocations from any single client.

- Stretched Sector Valuation Multiples: A trailing P/E nearing 95x means the market leaves virtually zero room for logistical disruption, component shortages, or slight guidance misses.

- Fierce Semiconductor Competition: Formidable, heavily capitalized industry peers like Broadcom, Marvell, and Astera Labs are continuously innovating alternative connectivity modules, creating ongoing market share risks.

- Inventory Expansion and Cash Conversion: While the massive buildout of inventory is intended to feed upcoming 1.6T data center configurations, it temporarily ties up significant operational capital on the balance sheet.

- Macro Capex Vulnerabilities: Credo's business model is tethered to the sustainability of multi-billion-dollar global AI infrastructure spending. Any broader economic deceleration could prompt an immediate structural pause in data factory buildouts.

Final Thoughts: Is Credo Technology (CRDO) Stock a Buy in 2026?

As of mid-2026, Credo Technology Group Holding Ltd stands out as one of the purest and most structurally sound picks-and-shovels plays within the artificial intelligence infrastructure landscape. The firm’s capacity to triple full-year revenue to $1.34 billion while maintaining robust 68.1% non-GAAP gross margins confirms deep product market fit and a clear technological moat within dense XPU clustering fabrics.

However, entering an asset trading at such a high valuation multiple requires strict operational discipline and a solid risk management plan. For short-term tactical traders, Credo's high beta (3.2) and clear post-earnings ranges offer an ideal playground for volatility capture via BingX futures. Long-term market participants, conversely, may find it strategic to scale into positions via dollar-cost averaging during structural pullbacks, allowing the company’s underlying earnings power to organically mature into its premium market valuation.

Risk Reminder: Trading high-growth semiconductor and technology equities involves immense financial risk due to elevated beta metrics, capital-intensive manufacturing timelines, and rapidly evolving technological cycles. Always enforce strict risk management protocols, proper position sizing, and mandatory stop-losses.

Related Reading

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top 10 Quantum Computing Stocks to Watch in 2026: Companies Driving Next-Gen Computation

- Top AI Hyperscaler Stocks to Watch in 2026: The $700 Billion Cloud Infrastructure Race

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure