In mid-June 2026, Cerebras Systems (CBRS) sits directly at the center of the technology sector’s most anticipated market inflection point. Following its historic Nasdaq listing on May 14, 2026, which marked the largest U.S. tech initial public offering since 2019, the Sunnyvale-headquartered semiconductor pioneer is currently trading around $226.55, displaying an intensely volatile post-debut trajectory.

While the stock initially skyrocketed nearly 70% to hit intraday peaks of $386.34 during its opening sessions, a sector-wide technology cooling and macro-driven profit-taking led to a sharp 30% to 40% pullback toward a structural $201 support level. However, a massive wave of synchronized Wall Street analyst coverages has ignited an energetic rebound. As the global AI market rapidly transitions from initial model training toward massive, real-time agentic AI inference workloads, Cerebras' unique wafer-scale technology has positioned it as one of the most compelling pure-play underdogs challenging the legacy hardware status quo.

This comprehensive guide breaks down the Cerebras Systems stock forecast and price prediction for the remainder of 2026, utilizing data from Morgan Stanley, Citigroup, UBS, Wedbush, LSEG consensus estimates, and official IPO prospectus filings.

You will also discover how to trade Cerebras Systems (CBRS) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Cerebras Systems (CBRS) Traders to Know in 2026

As Cerebras navigates a high-stakes post-IPO trading environment defined by astronomical growth projections and intense market volatility, traders must monitor these five core market-moving factors:

- The Extraordinary $24.6 Billion Backlog: Cerebras entered the public markets boasting a staggering $24.6 billion backlog of remaining performance obligations. This massive figure represents roughly 48 times the company's total fiscal 2025 revenue, providing a visible, multi-year pipeline for aggressive top-line expansion.

- The Landmark Multi-Year OpenAI Compute Pact: The bedrock of Cerebras’ long-term validation is a multi-year master relationship agreement with Sam Altman’s OpenAI valued at over $20 billion. Running through 2028, the deal dictates the deployment of up to 750 megawatts (MW) of ultra-low-latency inference capacity, with an option for OpenAI to expand the commitment by an additional 1.25 gigawatts.

- The AWS Disaggregated Inference Integration: In March 2026, Cerebras finalized a pivotal architecture collaboration with Amazon Web Services (AWS) to deliver rapid generative AI decoding via Amazon Bedrock. This hybrid infrastructure pairs AWS Trainium for the initial prompt prefill stage with the Cerebras CS-3 system for the low-latency token generation decode stage.

- The Upcoming Q1 2026 Earnings Flashpoint: Cerebras will report its highly anticipated first public quarterly earnings report post-IPO on June 23, 2026, after the market close. This conference call will serve as a crucial test of the company's operational execution and near-term revenue recognition schedules.

- Severe, Sovereign-Scale Customer Concentration Risk: While Cerebras has made major strides diversifying its client roster through OpenAI and AWS, its historical filings reveal acute concentration risk. In fiscal 2025, the Mohamed bin Zayed University of Artificial Intelligence (MBZUAI) in the United Arab Emirates accounted for 62% of corporate revenues, while UAE-based tech giant G42 brought in an additional 24%.

What Is Cerebras Systems (CBRS)?

Founded in 2015, Cerebras Systems Inc. (CBRS) is a specialized semiconductor and cloud infrastructure company aiming to completely redefine artificial intelligence computing. Rather than cutting large silicon wafers into hundreds of individual small graphics processing units (GPUs) and connecting them via complex networking fabrics, Cerebras builds single, massive processors out of an entire silicon wafer.

Its flagship processor, the Wafer-Scale Engine 3 (WSE-3), is the largest commercialized AI chip in existence. Roughly 58 times larger than a leading legacy GPU, the dinner-plate-sized WSE-3 packs vastly superior on-chip memory and thousands of times more memory bandwidth directly onto the silicon. By keeping entire Large Language Model (LLM) weights fully resident on-chip, Cerebras eliminates the data transfer bottlenecks that slow down traditional clustered computing, delivering inference processing speeds up to 15 to 20 times faster than traditional GPU servers.

As of mid-2026, Cerebras offers its wafer-scale architecture both through the CS-3 system's on-premises computer deployments and via its high-performance, subscription-based cloud inference service.

Cerebras’ Post-IPO Performance: A Month of Volatile Repricing

Cerebras priced its historic IPO late Wednesday, May 13, 2026, at $185 per share, easily raising $5.55 billion by selling 30 million shares in an oversubscribed offering. When trading officially commenced on the Nasdaq on May 14 under the ticker CBRS, institutional and retail demand sent the stock opening at $350, peaking intraday at $386.34, and closing its inaugural session up 68% at $311.07, briefly implying an intraday market valuation of $95 billion.

However, the subsequent weeks delivered a harsh post-listing reality check. Concerns over elevated valuations across the semiconductor sector and hawkish Federal Reserve monetary policies triggered a prolonged 35% retracement, pushing shares down to a local low of $201.

The momentum shifted dramatically on Monday, June 8, 2026, following the expiration of the post-IPO quiet period. A powerhouse cohort of at least nine major Wall Street underwriting brokerages simultaneously initiated coverage on CBRS with unanimous Buy and Overweight ratings. This collective endorsement sparked an immediate 18.3% single-session surge back to the $226.55 zone, solidifying a volatile yet resilient floor well above the initial $185 listing price.

Financial disclosures from the company's mid-2026 prospectus illustrate the immense scale fueling this market enthusiasm:

Cerebras (CBRS) Key Financial Trajectory: Fiscal Year 2024 vs. 2025

- Revenue Acceleration: Total revenue reached $510 million in fiscal 2025, representing an impressive 75.9% year-over-year expansion compared to the $290.3 million generated in 2024. Growth was broad-based, with hardware revenue printing $358.4 million and cloud services surging 93.6% to $151.6 million.

- The Profitability Paradigm: Cerebras reported a GAAP net income of $237.8 million for 2025, a dramatic recovery from the $481.6 million GAAP net loss posted in 2024. However, market participants note that this net profit was heavily impacted by a one-time, non-cash accounting gain of $363.3 million related to the extinguishment of a forward contract preferred stock liability.

- Non-GAAP Realities: Excluding that singular accounting adjustment, Cerebras operated at a non-GAAP net loss of approximately $75.7 million in 2025 as it continued to invest aggressively in capital-intensive infrastructure, chip fabrication, and corporate scaling.

Cerebras’ 2026 Trading Strategy: What's Driving Volatility in CBRS Stock?

- The $185 - $200 Structural Support Floor: For technical traders, the region between the $185 IPO pricing level and the $201 post-debut low represents a critical, high-liquidity support zone. Holding above this structural range on weekly charts keeps the post-initiation recovery narrative firmly in play.

- Evaluating the Stretched Price-to-Sales Multiple: Trading at a trailing price-to-sales (P/S) ratio hovering around 88x, CBRS carries an immense premium compared to the broader tech sector's average multiple of 9x. Because traditional P/E tracking is distorted by the company's non-GAAP losses, traders must treat CBRS as a pure hyper-growth vehicle where valuations are explicitly linked to backlog conversion speed rather than current trailing earnings.

- The Post-Listing High-Beta Play: As a newly public AI pure-play, CBRS exhibits an exceptionally high intraday beta. Traders must brace for wide, single-day swings of 10% to 15%, particularly surrounding macro semiconductor data prints, supply chain allocation updates from chip foundries, and news emerging from key backers like SoftBank.

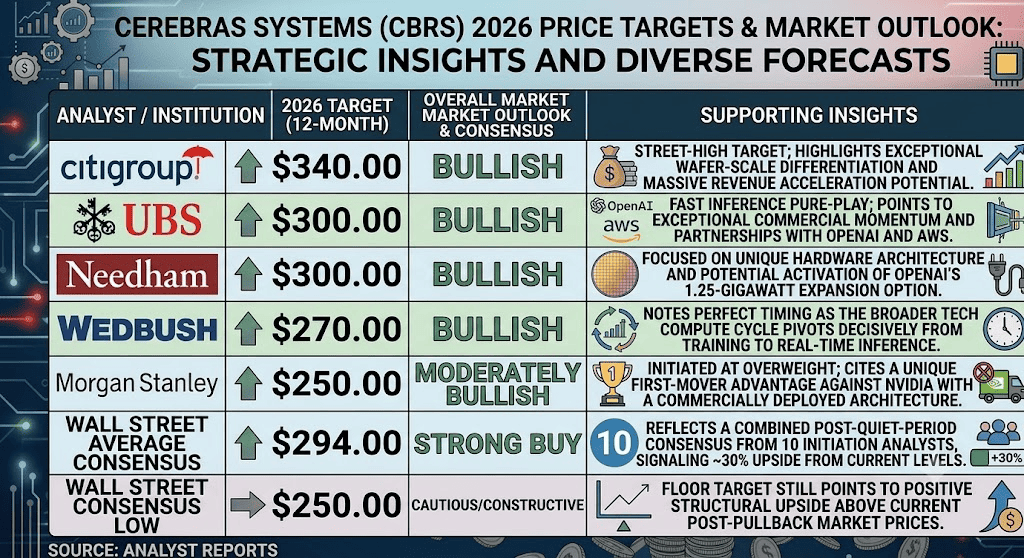

Cerebras 2026 Stock Forecast: $340 Street-High Peak vs. $185 IPO Floor

Cerebras stock price predictions for 2026 by Wall Street analysts

Evaluating Cerebras' forward path through the remainder of 2026 requires balancing an unprecedented, multi-billion-dollar contracted order book against the structural headwinds of an unprofitable balance sheet confronting a heavily entrenched incumbent.

The Bull Case for CBRS Stock: The $340 Fast Inference Monopoly

The bullish thesis is built around Cerebras' clear first-mover advantage in commercially deployed wafer-scale processors. Led by Citigroup's street-high price target of $340, this scenario assumes that the global AI landscape's structural pivot from training models to running Agentic AI reasoning workloads will spark a premium demand cycle for ultra-fast, low-latency inference.

If Cerebras flawlessly executes its massive infrastructure deployments for OpenAI and successfully ramps up its disaggregated cloud deliveries with AWS Bedrock, revenue recognition will scale exponentially throughout the upcoming quarters. Furthermore, if the company demonstrates meaningful margin expansion during its June 23 earnings call and signs an additional marquee hyperscaler to its cloud service, institutional capital is highly likely to drive CBRS past its near-term $250 and $300 resistance boundaries to retest its $386.34 all-time high.

The Base Case: $240 – $294 Consolidation Plateau for Cerebras Stock

The base case maps out an orderly, volatile consolidation phase where the market systematically digests Cerebras' massive operational potential against its near-term corporate constraints. Under this framework, supported heavily by the Wall Street consensus average target of $294, revenue remains firmly on track to hit triple-digit growth metrics as hyperscale entities aggressively activate their contracted backlogs.

However, the asset's upside will face a psychological cap driven by its current non-GAAP losses and the natural lock-up expiration dynamics typical of recent IPOs. For market participants, this sets up a highly liquid trading corridor between $240 and $294, where blowout top-line revenue metrics are balanced out by structural gross margins (currently near 39.03%) and capital expenditure demands.

Cerebras Systems' Bear Case: The $185 Valuation Multiples and Capital Trap

The bearish outlook focuses on the execution risks inherent to early-stage infrastructure providers. If the highly concentrated Middle Eastern revenues from MBZUAI and G42 experience any deployment delays, or if OpenAI slows down its capital expenditure drawdown schedules due to power availability or regulatory barriers, Cerebras’ astronomical 88x P/S valuation multiple will face a severe institutional de-rating.

This downside is amplified by fierce competitive threats. Nvidia is not sitting still; its aggressive rollout of Blackwell and upcoming Rubin platforms, combined with its acquisition of architectural alternatives like Groq-based assets, could pressure Cerebras' pricing power and compress its 39% gross margins. In this scenario, missing key metrics on the June 23 report would likely trigger a sharp break below the $201 local support, sending the stock crashing down to test its definitive $185 IPO pricing floor.

Cerebras Systems (CBRS) Price Prediction for 2026 by Wall Street Analysts

|

Institution |

2026 Price Target (12-Month) |

Overall Market Outlook |

|

Citigroup |

$340.00 |

Bullish: Street-high target; highlights exceptional wafer-scale differentiation and massive revenue acceleration potential. |

|

UBS |

$300.00 |

Bullish: Fast inference pure-play; points to exceptional commercial momentum and partnerships with OpenAI and AWS. |

|

Needham |

$300.00 |

Bullish: Focused on unique hardware architecture and potential activation of OpenAI’s 1.25-gigawatt expansion option. |

|

Wedbush |

$270.00 |

Bullish: Notes perfect timing as the broader tech compute cycle pivots decisively from training to real-time inference. |

|

Morgan Stanley |

$250.00 |

Moderately Bullish: Initiated at Overweight; cites a unique first-mover advantage against Nvidia with a commercially deployed architecture. |

|

Wall Street Average Consensus |

$294.00 |

Strong Buy: Reflects a combined post-quiet-period consensus from 10 initiation analysts, signaling ~30% upside from current levels. |

|

Wall Street Consensus Low |

$250.00 |

Cautious/Constructive: Floor target still points to positive structural upside above current post-pullback market prices. |

How to Trade Cerebras Systems (CBRS) Stock Futures on BingX TradFi

CBRS/USDT perpetual contract on BingX futures market

As Cerebras Systems navigates its post-IPO price discovery phase, tactical market participants can easily capture daily volatility and macro developments through the institutional-grade BingX platform.

- Access BingX TradFi: Log into your account and navigate to the specialized TradFi terminal located on the main BingX global exchange dashboard.

- Select Cerebras Systems (CBRS): Use the search function to locate and load the CBRS-USDT perpetual futures contract interface.

- Establish Your Market Bias: Select Open Long if you believe the upcoming June 23 quarterly earnings and massive $24.6 billion backlog will propel the stock toward Wall Street's $294 average consensus target. Select Open Short if you expect high valuation multiples and Nvidia's competitive moat to spark a retracement toward the IPO floor.

- Configure Leverage and Margin Parameters: Set your preferred Isolated or Cross-Margin modes alongside highly conservative leverage settings to maintain pristine capital efficiency.

- Deploy Risk Mitigation Tools: Enforce advanced BingX Take-Profit and Stop-Loss (TP/SL) orders to fully shield your portfolio against abrupt, news-driven price gaps during volatile pre-market and after-hours trading sessions.

Top 5 Risks to Consider Before Investing in CBRS Stock

While Cerebras' monumental tech architecture presents an alluring growth story, navigating the stock requires a disciplined understanding of its underlying operational risks:

- Pervasive Structural Unprofitability: Despite booking half a billion dollars in annual revenue, Cerebras continues to operate at a significant non-GAAP net loss, meaning its long-term viability depends on rapidly achieving real operational scale.

- Acute Customer and Sovereign Concentration: Relying on OpenAI for a baseline backlog, alongside historically drawing over 80% of revenues from a concentrated pair of entities in the United Arab Emirates (MBZUAI and G42), exposes the company to extreme single-point failure risks.

- The Nvidia Competitive Moat: Nvidia maintains a near-monopoly on AI capital allocation. Its immense research budget, software dominance (CUDA ecosystem), and deep hyperscaler relationships present a constant existential challenge to underdog hardware architectures.

- Extreme Valuation Premium: A trailing price-to-sales multiple near 88x leaves zero margin for operational error. Any minor shipment delay, component constraint, or missed quarterly estimate can result in violent institutional liquidations.

- Supply Chain and Foundry Dependencies: Cerebras does not own its manufacturing facilities. Its massive, cutting-edge wafer-scale chips rely entirely on third-party fabrication foundries, leaving the company highly vulnerable to global semiconductor supply disruptions.

Final Thoughts: Is Cerebras Systems (CBRS) Stock a Buy in 2026?

As of mid-2026, Cerebras Systems stands as one of the most exciting, high-beta pure-plays in the artificial intelligence ecosystem. Fundamentally, the company's ability to secure a historic $24.6 billion order backlog and a validation deal from OpenAI proves that its dinner-plate-sized wafer-scale architecture delivers concrete economic and performance advantages in the ultra-competitive fast inference sector.

However, trading a newly listed equity that carries an 88x P/S multiple alongside non-GAAP net losses demands immense operational care. For short-term tactical traders, the stock provides an elite, highly liquid vehicle for volatility capture via BingX futures ahead of the June 23 earnings print. Conversely, long-term investors may prefer a dollar-cost-averaging approach, scaling carefully into positions only as the company transforms its paper backlog into verified, realized cash flow.

Disclaimer: This article is provided for informational and educational purposes only and does not constitute financial, investment, or trading advice. Digital asset and TradFi derivatives trading involve significant risk of capital loss. Always perform your own due diligence (DYOR) and enforce strict risk management protocols.

Related Reading

- What Is OpenAI Pre-IPO and How to Trade It on BingX?

- Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

- TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

- SMCI Stock Price Prediction 2026: $65 Street-High Rack-Scale Boom or Corporate Governance Trap?

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide