In early June 2026, Applied Materials Inc. (AMAT) finds itself at a pivotal market crossroads, balancing unprecedented AI-driven operational demand against stretched historical valuations. Following an extraordinary 92% vertical surge year-to-date, the Santa Clara-headquartered semiconductor wafer fabrication equipment (WFE) pioneer is currently trading near $499.21, hitting recent intraday highs of $525.98 and significantly outperforming the broader benchmark index.

While the stock has endured localized pockets of macro volatility, evidenced by a sharp 9% single-session sector drawdown on June 5 triggered by a broader chip selloff, back-to-back operational breakthroughs have fundamentally repriced its top-line revenue outlook. Investors are aggressively weighing an exceptionally strong fiscal second-quarter report and upgraded guidance against a tight supply chain landscape and high-profile insider selling that is tempering near-term momentum.

As the global technology ecosystem rapidly scales up advanced packaging, high-bandwidth memory (HBM), and sub-2nm foundry logic, the absolute physical necessity for materials engineering has transformed Applied Materials into a primary technological bottleneck. However, trading at an elevated premium relative to historical valuation multiples, market participants are split on how much future growth is already priced into the equity.

This guide breaks down the Applied Materials stock forecast and price prediction for the remainder of 2026, utilizing data from Morgan Stanley, Mizuho, Citigroup, Morningstar consensus estimates, and official regulatory disclosures.

You will also discover how to trade Applied Materials (AMAT) stock futures on BingX TradFi with USDT collateral.

Top 5 Things for Applied Materials (AMAT) Traders to Know in 2026

As Applied Materials navigates a high-stakes environment of exponential infrastructure scaling and macro monetary pressures, tactical traders must closely monitor these five market-moving factors:

- The 25% Southeast Asia Footprint Expansion: To meet unyielding global order books, Applied Materials has launched an aggressive initiative to expand its Southeast Asia workforce by 25% in calendar 2026. The company is actively hiring 1,000 additional advanced manufacturing and engineering personnel, primarily concentrated in its core Singapore hub, boosting regional headcount from its 4,000-employee baseline established at the end of 2025.

- Blowout >30% WFE Growth Guidance: Capitalizing on the rapid deployment of next-generation logic and greenfield DRAM capacity, CEO Gary Dickerson formally stated that the company expects its core semiconductor equipment segment to grow by more than 30% in calendar 2026, significantly outstepping initial single-digit industry baseline models.

- The $25 Million Insider Liquidation: In June 2026, Prabu Raja, President of AMAT’s core Semiconductor Products Group, executed a massive individual insider liquidation, netting approximately $25 million by selling a portion of his shares at an average price of $505. The transaction reduced his total individual position by 12%, introducing a near-term sentiment overhang at key psychological resistance levels.

- A 10-Year High Valuation Premium: Driven by intense algorithmic chasing of 'picks and shovels' AI plays, AMAT’s trailing price-to-earnings (P/E) multiple has expanded to 46.2x. This multiple sits directly adjacent to its historical 10-year ceiling, flashing stark overvaluation signals on automated quantitative models.

- Severe Upstream Supply Chain Constraints: Management has candidly confirmed that current revenue growth is no longer bound by downstream customer acquisition, but rather by real-world logistics and manufacturing capacity. The primary bottleneck remains supply chain transit times required to produce specialized high-precision components, keeping a strict lid on near-term fulfillment pacing.

What Is Applied Materials (AMAT)?

Applied Materials, Inc. (NASDAQ: AMAT) is the world's largest supplier of materials engineering solutions used to produce virtually every new semiconductor chip and advanced display globally. Operating out of Silicon Valley, the company does not design or manufacture chips itself; instead, it engineers the highly specialized deposition, etching, ion implantation, metrology, and inspection systems required by global semiconductor foundries.

As of mid-2026, Applied Materials represents the absolute baseline infrastructure supplier to the entire global artificial intelligence value chain. The firm sits as the indispensable middleman beneath hyperscalers and chip designers like Nvidia, AMD, and Broadcom, providing the structural physical systems that enable foundries like TSMC, Samsung, and Intel to execute complex manufacturing architectures like Gate-All-Around (GAA) transistors, High-Bandwidth Memory (HBM3e/HBM4), and advanced hybrid bonding packaging.

Applied Materials' Performance in Early 2026: The Post-Earnings Repricing

AMAT stock performance in H1 2026 | Source: Yahoo Finance

The company kicked off its mid-year cycle by reporting standout fiscal second-quarter financial results on May 14, 2026. Total corporate revenue expanded by 11.4% year-over-year to hit $7.91 billion, cleanly exceeding Wall Street consensus expectations of $7.68 billion. The expansion was propelled heavily by its core Semiconductor Systems division, which experienced accelerating momentum as global foundries aggressively pulled forward equipment delivery timelines.

Crucially, the firm achieved a stellar non-GAAP gross margin of 50.0%, marking its highest manufacturing efficiency print in over 25 years. Non-GAAP earnings per share (EPS) printed at a record $2.86, with GAAP EPS hitting $3.51, substantially outpacing institutional consensus marks of $2.68.

Backed by unprecedented rolling 8-quarter customer visibility, executive leadership elevated fiscal third-quarter revenue guidance to a midpoint of $8.95 billion and non-GAAP EPS to a midpoint of $3.36. This guidance prompt triggered massive upward estimate revisions across Wall Street, establishing a strong fundamental floor beneath the equity.

Applied Materials' 2026 Trading Strategy: Navigating Volatility Multiples

To successfully navigate Applied Materials' high-beta profile through the remainder of the year, market participants must look beyond near-term headlines and structure their positions around key technical floors, cash-flow metrics, and structural market correlations.

The $450 - $460 Structural Support Zone

Technical analysts emphasize that the structural window between $450 and $460 serves as an essential horizontal support floor. Following the June 5 semiconductor flush, where the asset plummeted 9.7% to close at $453.01 amid macro interest rate jitters and broader tech margin decompression, strong institutional buyers immediately stepped in to defend this zone, driving the asset back up to the $499 region within 48 hours.

Stretched Multiples vs. Robust Cash Conversion

Trading at a steep 46.2x P/E, AMAT's multiple is significantly stretched compared to its 5-year median. However, unlike speculative growth assets, AMAT’s valuation premium is anchored by fortress-grade financials. The firm averages over $6 billion to $8 billion in annualized free cash flow, representing a near 90% conversion rate of net income. On June 9, the board leveraged this capital strength to declare a consistent quarterly cash dividend of $0.53 per share, alongside signaling an enormous $13.2 billion remaining in its active share repurchase authorization program.

High S&P 500 Amplification: Beta and Capture Metrics

Long-term statistical profiles over a 5-year horizon reveal that AMAT maintains a high 0.69 correlation with the S&P 500, carrying an active 1-year beta of 1.67. Quantitative tracking indicates that on days the S&P 500 gains, AMAT captures roughly 302% of the upside, while absorbing about 233% of the downside on down days. Traders must acknowledge that AMAT operates primarily as a systemic macro market amplifier rather than an uncorrelated portfolio diversifier.

Applied Materials 2026 Stock Forecast: $575 Street-High Peak vs. $355 Correction Target

Evaluating AMAT’s forward trajectory through the remainder of 2026 requires balancing an extraordinary technological monopoly against acute macro cyclical and geopolitical variables.

The Bull Case: AMAT's $575 Angstrom-Era and HBM Dominance Monopolization

The bullish thesis assumes that Applied Materials will aggressively outgrow the baseline wafer fab equipment market by over 10 percentage points through late 2026. Championed by top-tier investment desks including Citigroup's $520 target and street-high targets scaling up to $575, this framework relies on AMAT capturing an outsized market share of the upcoming 1.4nm and angstrom-era foundry transitions.

In this scenario, explosive domestic greenfield DRAM/HBM rollouts alongside expanding engagements at AMAT's proprietary EPIC Co-Innovation Center with TSMC, Micron, and SK Hynix will entirely offset any localized supply bottlenecks. If supply chains normalize faster than anticipated, allowing AMAT to fully realize its projected 35% equipment sales surge, institutional target upgrades will likely run past initial resistance to challenge the $550–$575 valuation targets.

The Base Case: $460 – $510 Valuation Consolidation Plateau for Applied Materials Stock

The baseline consensus model envisions AMAT consolidating its massive year-to-date gains within a defined structural range. Under this view, revenue remains rigidly on track to hit the revised consensus marks of $33.2 billion for fiscal 2026, with full-year EPS consolidating around $12.02 to $13.00.

However, upside remains fundamentally capped by the company’s own capacity limits and the persistent valuation discount applied to the tech sector amid sticky global inflation data. For market participants, this setup favors a highly liquid, volatile trading band between $460 and $510, where blow-out quarterly earnings metrics are periodically met with technical profit-taking and rotational cooling.

The Bear Case: AMAT Stock's $355 Macro Compression and Geopolitical Squeeze Trap

The bearish framework points to acute multiple contraction driven by macroeconomic shifts and geopolitical friction. If the Federal Reserve shifts toward a hawkish posture by late 2026 due to sticky economic metrics, or if the U.S. government levies severe subsequent export restrictions on shipments to East Asian semiconductor manufacturers, AMAT’s concentrated customer base could see immediate disruption.

Furthermore, if localized supply chain shortages solidify into persistent manufacturing blocks, or if prominent competitors like Lam Research (LRCX) or KLA Corporation (KLAC) aggressively capture share in specialized conductor etch and process control markets, a break below the $450 structural line would invalidate the current upcycle. This would leave the stock highly vulnerable to a sharp mean-reversion selloff toward the $355 bearish consensus floor.

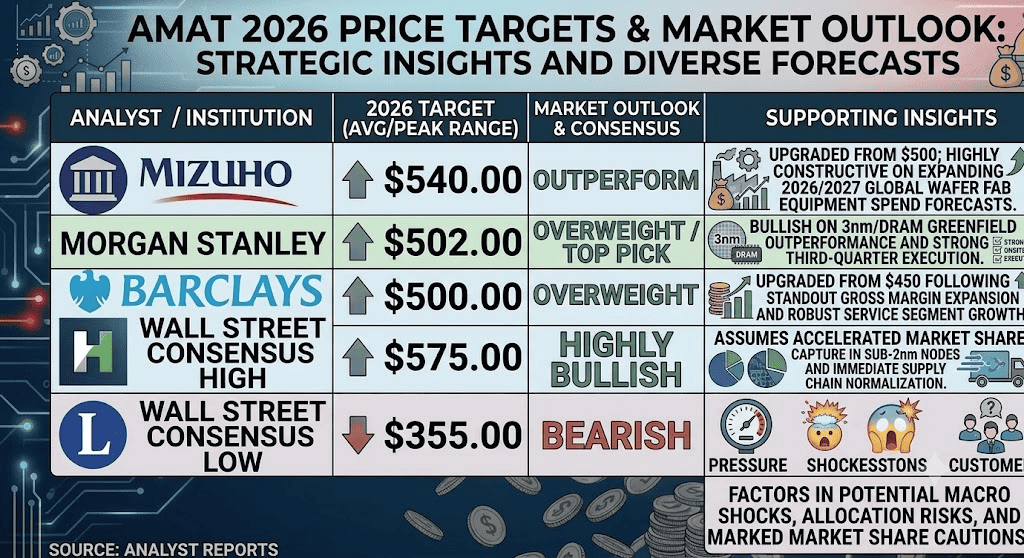

Applied Materials (AMAT) Price Predictions for 2026 by Wall Street Analysts

|

Institution / Source |

2026 Price Target (Peak/Avg) |

Overall Market Outlook |

|

Mizuho |

$540.00 |

Outperform: Upgraded from $500; highly constructive on expanding 2026/2027 global wafer fab equipment spend forecasts. |

|

Morgan Stanley |

$502.00 |

Overweight / Top Pick: Bullish on 3nm/DRAM greenfield outperformance and strong operational third-quarter execution. |

|

Barclays |

$500.00 |

Overweight: Upgraded from $450 following standout gross margin expansion and robust service segment growth. |

|

Wall Street Consensus High |

$575.00 |

Highly Bullish: Assumes accelerated market share capture in sub-2nm nodes and immediate supply chain normalization. |

|

Wall Street Consensus Low |

$355.00 |

Bearish: Factors in severe multiple compression, macro discount rate shocks, and customer allocation slowdowns. |

How to Trade Applied Materials (AMAT) Stock Futures on BingX TradFi

As Applied Materials moves through this high-momentum AI infrastructure supercycle, tactical traders can seamlessly capitalize on long or short price swings via the BingX platform.

- Access BingX TradFi: Log into your account and navigate to the specialized TradFi terminal located on the primary BingX global exchange dashboard.

- Select Applied Materials (AMAT): Input and select the AMAT-USDT perpetual futures contract within the trading interface.

- Establish Your Market Direction: Select Open Long if you anticipate that the workforce expansion and robust 50% gross margins will drive the equity toward its $575 street-high target. Select Open Short if you look to capitalize on the $25M insider selling overhang and high valuation multiples.

- Configure Leverage and Margin Parameters: Set your preferred Isolated or Cross-Margin structures alongside disciplined, conservative leverage levels to safely maximize capital efficiency.

- Deploy Risk Protection Protocols: Instantly configure advanced Take-Profit and Stop-Loss (TP/SL) orders to protect your capital against volatile, news-driven gaps during extended aftermarket and early morning hours.

Top 5 Risks to Consider Before Investing in AMAT Stock

While Applied Materials' central positioning in the AI expansion represents an incredibly compelling narrative, long-term exposure requires a deep calculation of structural risk factors:

- Stretched Historical Multiples: Trading at 46.2x forward earnings, the stock leaves an incredibly thin margin for operational error; any slight guidance adjustment could trigger sharp institutional de-risking.

- Intense Customer Concentration: AMAT remains highly reliant on a consolidated cohort of primary global buyers, including TSMC, Samsung, and Intel. A spending reduction from any single entity heavily impacts global revenues.

- Persistent Supply Chain Friction: The transition from unconstrained demand to constrained physical fulfillment means execution risk is completely tied to third-party sub-component suppliers.

- Geopolitical Export Jurisdictions: Escalating trade blockades and shifting technological compliance rules between Western and East Asian economic zones pose an unquantifiable, sudden regulatory risk to WFE shipping pipelines.

- Macro Discount Rate Volatility: Because AMAT acts as a high-volatility market amplifier, its valuation is exceptionally sensitive to shifts in macro interest rates and sovereign bond yield environments.

Final Thoughts: Is Applied Materials (AMAT) Stock a Buy in 2026?

As of June 2026, Applied Materials represents one of the cleanest, fundamentally sound 'picks and shovels' plays inside the global artificial intelligence infrastructure ecosystem. The firm's ability to maintain a 50% gross margin while guiding for a massive 30% expansion in calendar year equipment sales proves its staggering operational relevance and deep moat.

However, purchasing an asset trading near historical valuation ceilings requires meticulous tactical execution. For short-term derivatives traders, the stock provides an outstanding, highly liquid landscape for volatility capture via BingX futures. Conversely, long-term spot investors may find it mathematically advantageous to build exposure gradually via disciplined dollar-cost averaging, or wait for systemic market pullbacks to acquire larger structural positions at a relative discount.

Risk Reminder: Trading high-growth technology and semiconductor capital equipment equities involves substantial capital risk due to elevated beta metrics, capital-intensive R&D requirements, and changing global trade environments. Always enforce absolute risk discipline, tight position sizing, and automated stop-losses.

Related Reading

- SMCI Stock Price Prediction 2026: $65 Street-High Rack-Scale Boom or Corporate Governance Trap?

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide

- Top 10 AI Infrastructure Stocks to Buy in 2026: Chip Manufacturing and Design Leaders

- Top 10 AI Hardware Stocks to Watch in 2026: The Architecture Driving Next-Gen Intelligence

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle