Few technology companies have undergone a more dramatic reinvention than Oracle. For decades, the enterprise software giant was known for relational databases and legacy on-premise infrastructure, a reliable but slow-growing business many investors viewed as a relic of the pre-cloud era. The AI buildout changed that narrative. Oracle’s second-generation cloud architecture proved well suited for large-scale AI model training, leading developers including OpenAI, Meta, and NVIDIA to sign some of the largest cloud infrastructure contracts in the industry. By the first half of fiscal 2026, Oracle’s Remaining Performance Obligations (RPO), its measure of contracted future revenue, had reached $523 billion.

Yet the ORCL stock has not reflected this transformation. After reaching $345.72 in September 2025, ORCL had fallen to roughly $152 by March 10, 2026. The decline highlights a central tension in Oracle’s investment case. To support its AI cloud contracts, the company has committed about $50 billion in capital expenditures for fiscal 2026, pushing free cash flow temporarily negative and long-term debt above $100 billion. This guide examines Oracle’s 2026 stock outlook using analysis from Jefferies, TD Cowen, Citi, Barclays, Evercore ISI, and RBC Capital, while evaluating the key drivers that could determine whether ORCL can recover.

Note: Oracle’s fiscal year runs from June to May, so fiscal Q3 2026 covers December 2025 through February 2026, roughly equivalent to calendar Q1 2026.

Key Highlights: Top 5 Things Oracle Investors Should Know in 2026

1. Remaining Performance Obligations Reached $523 Billion: Oracle's RPO grew 438% year over year in fiscal Q2 2026, reflecting binding long-term contracts with major AI developers including OpenAI, Meta, and NVIDIA. This figure provides multi-year contracted revenue visibility, though recognition timing depends on data center completion and customer drawdown schedules.

2. OCI IaaS Revenue Growing at 68% Year Over Year: Oracle Cloud Infrastructure IaaS revenue reached $4.1 billion in fiscal Q2 2026. Analysts at TD Cowen and Jefferies project growth acceleration toward 80–100% in the second half of fiscal 2026 as capacity for key customers continues to ramp.

3. $50 Billion Capital Expenditure Commitment for Fiscal 2026: Oracle revised its fiscal 2026 capex guidance upward mid-year to approximately $50 billion to fund AI data center construction across multiple U.S. states. This has resulted in negative free cash flow and long-term debt exceeding $100 billion, which remains the central concern for more cautious investors.

4. Analyst ORCL Price Targets Range from $160 to $320: The wide range reflects differing views on how quickly Oracle's contracted backlog will convert to recognized revenue and when free cash flow will return to positive territory. Wall Street consensus sits at approximately $280, implying significant upside from the current price level.

5. Fiscal Q3 2026 Earnings on March 10, 2026: Oracle reports fiscal Q3 2026 results tonight after market close. Consensus expects non-GAAP EPS of $1.70 and revenue of approximately $16.9 billion. OCI growth rate and net new RPO additions are the two metrics analysts expect to most influence the stock's reaction.

What Is Oracle (ORCL)?

Oracle Corporation is one of the world’s largest enterprise technology companies, providing database software, cloud applications, and cloud infrastructure services. Founded in 1977 by Larry Ellison, Bob Miner, and Ed Oates, Oracle built its early business around relational database technology, releasing its first commercial SQL-based database in 1979. Over the following decades, the company became a core data management platform for financial institutions, governments, manufacturers, and retailers worldwide, creating a large installed base that continues to generate substantial recurring support revenue.

Oracle’s revenue is organized into three segments. The Cloud and License segment, the largest, includes Oracle Cloud Infrastructure (OCI), SaaS applications such as Fusion Cloud ERP and NetSuite, and database license support. The Hardware segment covers engineered systems such as Exadata, while the Services segment provides implementation consulting. In recent years, OCI’s second-generation architecture, designed for low-latency cluster networking and large GPU workloads, has attracted major AI developers and shifted Oracle’s growth narrative toward cloud infrastructure.

Oracle's Strategic Evolution (1977–2026): From Database Software to AI Cloud Infrastructure

Oracle’s history reflects repeated expansion beyond its original database business. During the 1990s and 2000s, acquisitions including PeopleSoft, Siebel, and Sun Microsystems expanded the company into enterprise applications and hardware. In the 2010s, Oracle launched Oracle Cloud Infrastructure (OCI), though it initially lagged behind AWS, Microsoft Azure, and Google Cloud in market share.

The company’s more recent transformation has been driven by demand for AI training infrastructure. OCI’s cluster networking architecture proved well suited for large GPU workloads, attracting customers including OpenAI, Meta, and NVIDIA. These contracts pushed Oracle’s Remaining Performance Obligations (RPO) to $523 billion by fiscal H1 2026 and positioned AI cloud infrastructure at the center of the company’s growth strategy. In September 2025, Larry Ellison transitioned to Executive Chairman and CTO to focus on AI data center architecture, while Oracle committed roughly $50 billion in capital expenditures for fiscal 2026 to expand its data center capacity.

Oracle's Key Growth Phases

• The Database Era (1977–2010): Oracle Database became a global enterprise data platform. Deep integration into enterprise systems created high switching costs and long-term support revenue.

• The Application and Early Cloud Era (2010–2022): Oracle expanded into enterprise applications and launched OCI while initially trailing the major hyperscale cloud providers.

• The AI Infrastructure Era (2023–Present): OCI secured major contracts with leading AI developers. RPO reached $523 billion by fiscal H1 2026, prompting large-scale investment in new AI data center infrastructure.

Oracle (ORCL) FY2026 Performance Overview: Growth, Capex, and Profit Pressures

Oracle entered fiscal 2026 with strong cloud infrastructure demand and one of the largest contracted revenue backlogs in the technology sector. At the same time, the company is entering a capital-intensive phase as it builds AI data center capacity to support those contracts.

1. FY2025 Revenue Reached $57.4 Billion

Oracle reported $57.4 billion in fiscal 2025 revenue, up from $53.0 billion in fiscal 2024. While overall growth of 8% year over year was moderate, OCI IaaS grew 52%, reflecting a shift toward cloud infrastructure. Net income reached $12.4 billion, supported by Oracle’s high-margin software and support business, providing the financial base entering the capital-intensive fiscal 2026 expansion phase.

2. Fiscal Q2 2026: OCI Growth and $523 Billion RPO

In fiscal Q2 2026, OCI IaaS revenue grew 68% year over year to $4.1 billion, while cloud applications revenue reached $3.9 billion, up 11%. Total cloud revenue of $8.0 billion represented 34% growth. Oracle’s Remaining Performance Obligations (RPO) reached $523 billion, up 438% year over year, reflecting long-term AI infrastructure contracts and increased investor focus on future revenue conversion.

3. A $50 Billion Capital Expenditure Cycle

Oracle plans roughly $50 billion in fiscal 2026 capital expenditures to build AI data centers across the United States as part of the Stargate initiative with OpenAI. The investment has pushed free cash flow negative, increased long-term debt above $100 billion, and contributed to gross margin compression to about 67.8%, reflecting the lower-margin profile of cloud infrastructure relative to legacy software.

4. Multi-Cloud and AI Agent Adoption

Oracle has partnered with Google Cloud and Amazon AWS to run Oracle Database natively within their environments, expanding its enterprise market reach. At the same time, AI agents integrated into Fusion Cloud and NetSuite are increasing OCI compute consumption. While still early in revenue impact, analysts see these trends as potential growth drivers for 2026–2027.

The Oracle Investment Thesis for 2026: 4 Pillars of ORCL Stock Valuation

Oracle’s valuation in 2026 increasingly reflects more than its legacy enterprise software business. Analysts now evaluate the company through four structural drivers shaping its long-term trajectory: the conversion speed of its massive RPO backlog, OCI’s AI infrastructure advantage, the stabilizing margins of its legacy software business, and the earnings timeline that could confirm the AI growth narrative.

1. RPO Conversion: The Core Variable in Revenue Forecasts

Oracle’s $523 billion Remaining Performance Obligations (RPO) represents binding customer commitments rather than pipeline estimates. The key question is how quickly this backlog converts into recognized revenue. Conversion depends on data center construction, infrastructure deployment, and the pace at which customers utilize contracted capacity. Bullish forecasts assume faster ramp timelines, while more cautious models apply larger execution discounts.

2. OCI Architecture: Oracle’s AI Infrastructure Advantage

OCI’s cluster networking architecture was designed for the all-to-all GPU communication required during large AI training workloads. Adoption by OpenAI, despite access to multiple cloud providers, is often cited as evidence of real technical differentiation. Multi-cloud agreements with Google Cloud and AWS further expand Oracle’s potential market, though competing hyperscalers investing in similar AI infrastructure remain a key risk.

3. Legacy Software Economics: The Margin Stabilizer

Oracle’s database support contracts and SaaS subscriptions generate high-margin recurring revenue. This installed base offsets the lower margins of the rapidly growing OCI infrastructure business and provides financial stability during Oracle’s capex-heavy AI expansion phase.

4. Earnings Timing: The Near-Term Catalyst for RPO Validation

Oracle’s June–May fiscal year means its fiscal Q3 and Q4 results, covering December 2025 through May 2026, coincide with the expected ramp in OCI capacity. If OCI growth approaches the 80–100% range projected by analysts, those earnings reports could provide early confirmation that RPO is converting into revenue.

Oracle (ORCL) Price Forecasts for 2026: Bull vs. Bear Outlook

Several analysts revised price targets lower ahead of Oracle’s fiscal Q3 earnings release, reflecting more conservative assumptions around margin recovery and revenue recognition timelines. The consensus rating remains Buy, though the target range is unusually wide for a large-cap technology company.

Institutional Price Targets for Oracle (ORCL) in 2026

| Institution | 2026 Price Target | Market Outlook |

| Jefferies (Brent Thill) | $320 | Buy: Sees strengthening AI pipeline and views the post-September decline as disproportionate to OCI growth. Lowered from $400. |

| Citi (Tyler Radke) | $310 | Buy: Maintains positive AI infrastructure thesis with more conservative margin assumptions. Lowered from $370. |

| TD Cowen (Derrick Wood) | $250 | Buy: Projects OCI growth near 80% in fiscal Q3, accelerating toward 100% in Q4 as OpenAI capacity ramps. Lowered from $350. |

| Barclays (Raimo Lenschow) | $230 | Overweight: Supports long-term thesis while monitoring free cash flow recovery. Lowered from $310. |

| Evercore ISI (Kirk Materne) | $220 | Outperform: Views RPO conversion as the key re-rating catalyst. Lowered from $275. |

| RBC Capital (Rishi Jaluria) | $160 | Sector Perform: Flags capex discipline concerns and RPO concentration among AI customers. Lowered from $195. |

| Wall Street Consensus | ~$280 | Buy: Approximately 30 Buy / 10 Hold / 2 Sell ratings as of early March 2026. |

The Bull Case: OCI Growth and RPO Conversion Could Support a Return Toward $300

Bullish analysts argue that Oracle’s $523 billion Remaining Performance Obligations (RPO) provides a contracted revenue base that the market may undervalue. If OCI growth approaches the 80–100% range projected for fiscal Q3 and Q4, Oracle’s quarterly revenue run rate could move toward $20 billion by fiscal 2027, implying a valuation multiple below comparable cloud infrastructure peers.

They also argue that the current margin pressure reflects a temporary capex cycle. As utilization rises and infrastructure spending stabilizes, operating leverage from OCI combined with high-margin legacy software revenue could drive earnings expansion.

The Bear Case: Capex Pressure and Execution Risk Keep Downside Near $160

More cautious analysts focus on the gap between RPO as contracted backlog and RPO as realized revenue. Data center construction timelines, infrastructure deployment, and customer usage rates all influence how quickly the backlog converts into revenue.

With gross margins already falling to about 67.8% as IaaS scales, margin recovery may take time. Combined with concerns about capex discipline and project execution, some analysts warn that weaker results could push the stock back toward its $118.86 52-week low, especially with ORCL already trading near RBC’s $160 downside target.

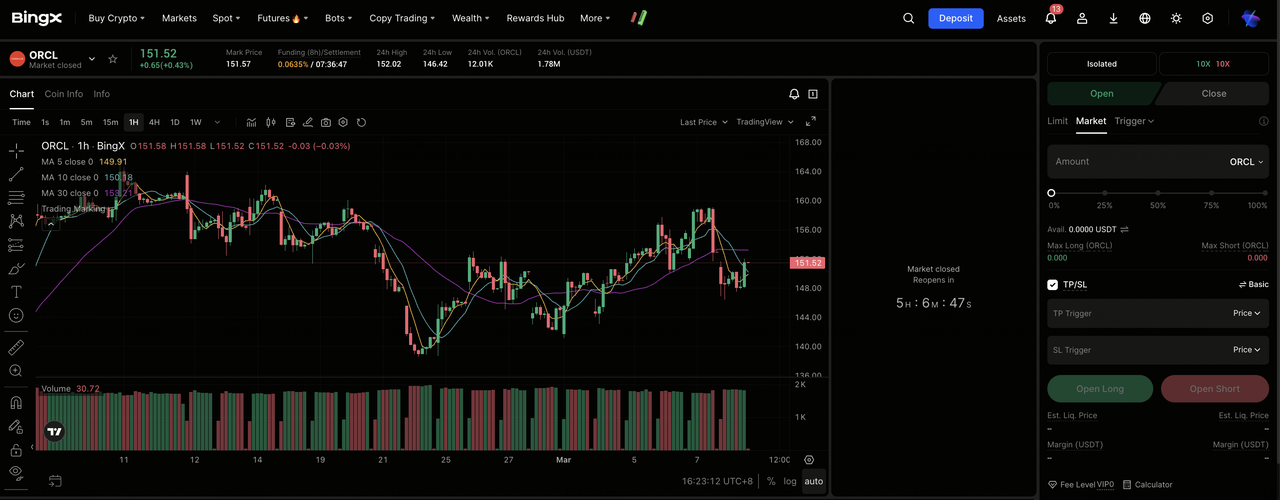

How to Trade Oracle (ORCL) Stock Futures on BingX TradFi

BingX TradFi offers USDT-settled Oracle stock perpetual contracts, allowing traders to take long or short positions on ORCL without a traditional brokerage account. BingX AI provides real-time volatility tools and automated execution features that may be useful when managing positions around earnings-related price movements.

Long or Short Oracle (ORCL) Stock Perpetuals with USDT on BingX Futures

1. Go to the BingX TradFi section and select Stock Futures.

2. Search for the ORCL/USDT perpetual contract.

3. Check the trading session before placing your order. Liquidity is typically lower during extended sessions, which can result in wider spreads and higher volatility. Oracle (ORCL) follows the NYSE schedule:

• Regular Hours: 9:30 AM – 4:00 PM Eastern Time (ET), Monday–Friday

• Pre-Market: 4:00 AM – 9:30 AM ET

• After-Hours: 4:00 PM – 8:00 PM ET

4. Select your Margin Mode (Isolated or Cross) and set your leverage. Oracle has averaged approximately 7.5% in price movement on earnings days over the past year. 2×–3× leverage is a commonly cited range for managing risk on a high-beta position around an event-driven catalyst.

5. Choose Open Long if you expect fiscal Q3 results to confirm OCI growth acceleration and RPO momentum, or Open Short if you expect continued margin pressure or weaker-than-expected revenue guidance.

6. Set Take-Profit (TP) and Stop-Loss (SL) levels before the earnings release. Post-earnings price movements on ORCL can be significant, and pre-set exit levels help manage risk in fast-moving conditions.

5 Critical Risks to Watch for Oracle Investors in 2026

Oracle’s AI infrastructure strategy introduces several risks that investors should monitor through fiscal 2026 and beyond.

1. Free Cash Flow Recovery Remains Unclear: Oracle’s roughly $50 billion fiscal 2026 capex program has pushed free cash flow negative. Management has not specified when spending will peak or when cash generation will normalize.

2. RPO Concentration in Key AI Customers: A large portion of Oracle’s $523 billion Remaining Performance Obligations (RPO) is tied to OpenAI. The shelving of the expanded Stargate Texas project showed that parts of the partnership can change, which could affect revenue conversion timelines.

3. Continued Gross Margin Pressure: Infrastructure services carry lower margins than Oracle’s legacy software business. As OCI expands, gross margins near 67.8% may remain under pressure until data center utilization improves.

4. Legal and Disclosure Risk: A February 2026 securities class action alleges Oracle did not fully disclose risks tied to the scale of its AI infrastructure spending relative to near-term revenue impact.

5. Rising Hyperscaler Competition: AWS, Microsoft Azure, and Google Cloud are investing heavily in AI infrastructure. At the same time, major AI developers may build their own data centers, potentially reducing reliance on third-party providers.

Conclusion: Should You Invest in Oracle (ORCL) Stock in 2026?

Oracle’s 2026 outlook combines strong structural growth with near-term financial pressure. The company holds $523 billion in contracted revenue, OCI is growing 68% year over year, and its legacy software business continues generating high-margin recurring income. With ORCL trading near $152, more than 50% below its September 2025 peak and well under the ~$280 Wall Street consensus target, some investors see potential upside if OCI growth accelerates and the backlog converts into revenue.

However, Oracle is currently in a capital-intensive phase. Free cash flow is negative, long-term debt exceeds $100 billion, and margins are compressing as cloud infrastructure scales. Investors should watch three indicators: OCI IaaS growth, particularly whether it approaches the 80–100% range projected by analysts; net new RPO additions as a signal of sustained demand; and management guidance on when capital spending will peak and free cash flow turns positive.

Risk Reminder: This article is for informational purposes only and does not constitute investment advice. Oracle stock carries significant risks including capital expenditure uncertainty, margin pressure, ongoing legal proceedings, and earnings volatility. Past performance and analyst price targets are not guarantees of future results. Investors should conduct independent research before making any investment decisions.

Related Reading

1. Tesla (TSLA) Stock Outlook for 2026: Can the Great AI and Robotaxi Pivot Take TSLA Stock to $600?

2. How to Buy Nvidia (NVDA) Stock in 2026: Complete Guide for Beginners

3. Top AI Tokenized Stocks to Watch in 2026

4. How to Trade Forex, Commodities, Stocks, and Indices With BingX TradFi: A Beginner's Guide (2026)