In April 2026, SanDisk Corporation (SNDK) is no longer just a memory chip maker but it is also the primary friction point in the global AI arms race. Since its 2025 spinoff from Western Digital, SNDK has delivered a staggering 239% year-to-date return, trading at $913.02 after hitting a lifetime high of $965. Investors are currently laser-focused on April 20, 2026, the effective date of SanDisk's promotion to the prestigious Nasdaq-100 Index. While bulls argue that passive inflows of over $600 billion tracking the index will force a massive buying spree, skeptics warn that the stock's 2,700% one-year surge has left it vulnerable to 'buy the rumor, sell the news' dynamics.

As the April 30, 2026, earnings report approaches, SanDisk is riding an unprecedented memory supercycle. With data center revenues surging 64% and management signaling that NAND supply is effectively sold out through 2026, the company is weaponizing extreme pricing power. This guide breaks down the SNDK stock price prediction for 2026 using data from Evercore ISI, Bernstein, Trefis, and ChartMill.

You will also discover how to trade SanDisk (SNDK) stock futures on BingX TradFi.

Top 5 Things for SanDisk Investors to Know in 2026

- Nasdaq-100 Index Inclusion: On April 20, 2026, SNDK officially replaced Atlassian in the Nasdaq-100. This mechanical event forces institutional ETFs like QQQ to acquire billions in shares, creating a high-liquidity floor for the stock.

- The NAND Pricing Power: SanDisk's gross margins are projected to hit 65-67% in Q3 2026, driven by an acute shortage of high-performance Enterprise SSDs required for Large Language Models (LLMs).

- The TurboQuant Threat: Google's new TurboQuant algorithm claims to reduce AI memory requirements by 6x. While it caused a temporary 11% dip in March, analysts remain divided on whether this efficiency will kill demand or accelerate AI adoption (the Jevons Paradox).

- Fiscal Q3 Earnings Outlook: Wall Street expects a massive $14.46 EPS on $4.73 billion in revenue for the April 30 report, representing a year-over-year earnings explosion of over 4,000%.

- 2028 Cliff Risk: While 2026 and 2027 forecasts are ultra-bullish, consensus estimates for 2028 suggest a potential negative growth rate as the memory cycle naturally matures and supply finally catches up.

What Is SanDisk Corporation (SNDK)?

Founded in 1988 and headquartered in Milpitas, California, SanDisk is a global leader in NAND flash storage solutions. Following its highly successful 2025 spinoff, the company has repositioned itself from a consumer-grade USB and SD card provider into an enterprise-first AI infrastructure powerhouse.

SanDisk enters Q3 2026 with a forward P/E of approximately 20x, which many analysts consider reasonable given its projected 124% EPS growth for 2027. Its competitive moat is built on vertical integration and strategic supply partnerships, such as the recent capacity deal with Nanya Technology, allowing it to capture a larger share of the $140 billion+ market cap it now commands.

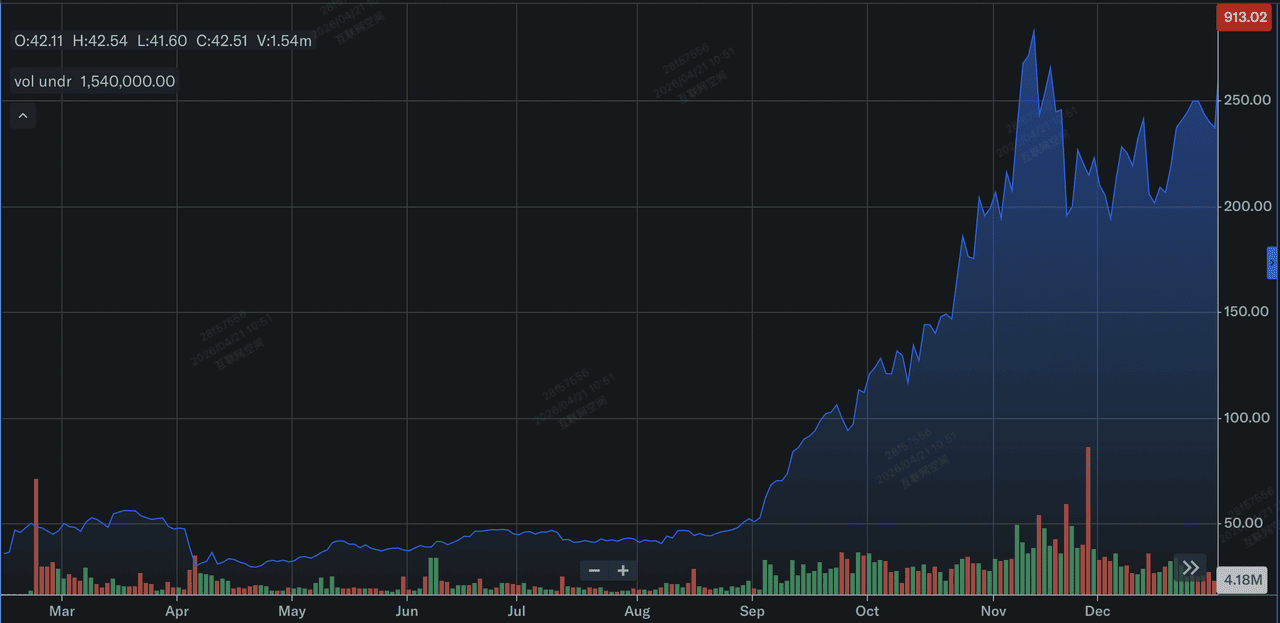

An Overview of SanDisk (SNDK) Stock Performance in 2025

SanDisk's stock performance review in 2025 | Source: Yahoo Finance

In 2025, SanDisk (SNDK) experienced a transformative and parabolic year, primarily defined by its historic spinoff from Western Digital in early 2025. Following its return to the public markets as a standalone entity, the stock saw a massive surge of approximately 550% over the calendar year. This rally was ignited by a perfect storm of tightening NAND flash supply and an explosion in demand for enterprise-grade Solid State Drives (SSDs) required to power the global AI data center buildout.

Financially, while the company spent much of the year navigating the tail end of a cyclical downturn, reporting a GAAP loss of $23 million in its fiscal fourth quarter, its underlying metrics signaled a massive pivot. By the second half of 2025, revenue began to exceed analyst expectations, climbing to $1.90 billion in the final quarter. Investors aggressively priced in SanDisk’s new identity as a pure-play AI infrastructure leader, setting the stage for the even more extreme 2,700% gains witnessed as the company approached its 2026 Nasdaq-100 inclusion.

Read more: Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?

SanDisk’s 2026 Strategy: The Storage-as-Compute Pivot

- Enterprise SSD Dominance: SanDisk is aggressively shifting its mix toward high-margin Enterprise SSDs, which now account for the majority of its sequential revenue growth.

- AI Data Center Vertical: CEO David Goeckeler recently noted that data centers are now the single largest buyers of NAND, surpassing consumer electronics for the first time in the company's history.

- Supply Discipline: Unlike previous cycles, SanDisk and its peers like Micron and Samsung are maintaining strict build-to-demand discipline to keep ASPs (Average Selling Prices) elevated.

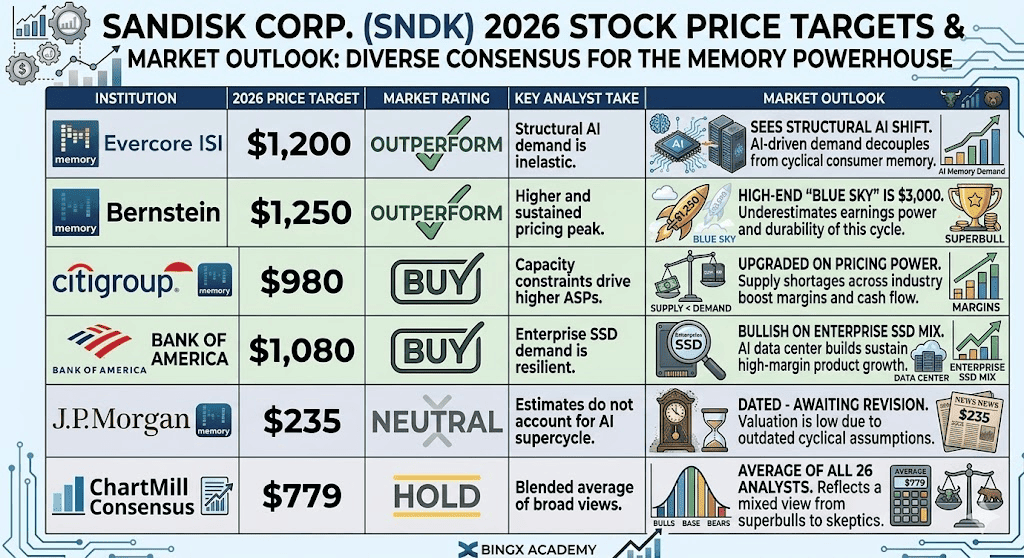

SNDK Stock 2026 Investment Outlook: $1,250 Blue Sky vs. $740 Mean Reversion

SanDisk stock forecasts for 2026 by various Wall Street analysts

The 2026 outlook for SNDK stock is a battle between its unprecedented earnings inflection and the technical exhaustion of a parabolic stock.

The Bull Case: SanDisk's $1,250 AI Supercycle Continuation

The bullish thesis hinges on the belief that the current memory boom is structural rather than merely cyclical. If SanDisk fulfills its aggressive Q3 guidance of $12–$14 EPS, it will validate the narrative that AI-driven demand for Enterprise SSDs has fundamentally decoupled from the traditional PC and smartphone cycles. With Average Selling Prices (ASPs) projected to climb 30% per quarter, analysts at Evercore ISI and Bernstein argue that SNDK is entering a period of extreme, inelastic pricing power. In this scenario, the stock undergoes a permanent valuation re-rating, shifting from a commodity-based multiple to a premium AI infrastructure multiple, potentially catapulting the price toward the $1,250 mark.

Practically, this scenario requires SanDisk to maintain its 65%+ gross margin profile while weaponizing its sold out inventory status through 2028. Investors should watch for sequential revenue growth in the data center segment exceeding 60% as a lead indicator. If hyperscalers continue their all-in CapEx spending despite rising costs, SNDK becomes a high-margin proxy for the Agentic Web. For traders, this represents a buy-the-dip environment where the Nasdaq-100 inclusion provides a permanent liquidity floor, transforming what was once a volatile memory play into a core, high-alpha technology holding.

The Base Case: $940 Fair Value Consolidation for SNDK Stock

The base case positions SNDK for a period of healthy digestion following its parabolic 2,700% run. While the stock has arguably outpaced its mean analyst target of $779, the floor is being aggressively raised by institutional revisions from Citigroup at $980 and Cantor Fitzgerald at $1,000. This scenario anticipates that the mechanical buying pressure from the Nasdaq-100 inclusion will be offset by profit-taking after the April 30 earnings report. The stock is expected to oscillate within a high-floor consolidation zone between $900 and $950, tracking the broader PHLX Semiconductor Index (SOX) rather than moving in isolation.

For the disciplined investor, this consolidation represents a transition from speculative mania to institutional stability. Data-wise, success in the base case is defined by SanDisk meeting, but not necessarily blowing away, its $4.6 billion revenue midpoint guidance. It assumes that while the AI arms race continues, the extreme 55% sequential price hikes in NAND will begin to normalize toward a sustainable 15–20% range. This results in a lower volatility alpha, where SNDK remains a market leader but yields the floor to technical indicators like the 50-day moving average to dictate entry points for long-term accumulation.

The Bear Case: SanDisk's $740 Correction on Efficiency Gains

The bear case is centered on The TurboQuant Paradox, the risk that AI software becomes too efficient for the hardware that supports it. Google’s announcement of a 6x reduction in memory usage per model serves as a warning that hyperscalers are actively engineering their way around the high cost of NAND. If this efficiency gain leads to a sudden drop in bits shipped, SanDisk could find itself with billions in committed CapEx just as demand hits a digestion phase. This would trigger a sharp multiple compression, as investors realize that the insatiable demand was, in fact, a temporary supply-chain bottleneck rather than a permanent shift.

From a technical perspective, a break below the $850 support level would likely trigger a mass exodus of momentum traders and speculators who entered specifically for the Nasdaq-100 inclusion pop. In this risk-off environment, the stock would likely seek its mean support level at $740, a 19% correction from current levels. Investors must monitor the Price-to-Sales ratio; if it remains elevated while revenue growth stalls below 20% sequentially, it signals a valuation bubble. This scenario serves as a reminder that in the memory industry, the transition from shortage to glut can happen in a single quarterly reporting cycle.

SanDisk Stock Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Evercore ISI |

$1,200 |

Outperform: Sees structural AI shift. |

|

Bernstein |

$1,250 |

Outperform: High-end "blue sky" is $3,000. |

|

Citigroup |

$980 |

Buy: Upgraded on pricing power. |

|

Bank of America |

$1,080 |

Buy: Bullish on Enterprise SSD mix. |

|

J.P. Morgan |

$235 |

Neutral: (Dated - awaiting revision). |

|

ChartMill Consensus |

$779 |

Hold: Average of all 26 analysts. |

How to Trade SanDisk (SNDK) Stock on BingX

Navigate the volatility of the AI memory cycle on BingX TradFi with BingX AI's predictive analytics. Traders can utilize leverage to position for the next leg of the rally or hedge against a cyclical turn.

SNDK/USDT perpetuals on BingX futures market

Long or Short SNDK Stock Futures on BingX

- Navigate to BingX TradFi and select Stock Futures.

- Select the SNDK/USDT perpetual contract.

- Set your leverage, e.g., 2x–5x, and select Open Long if you expect an earnings beat, or Open Short if you believe the Nasdaq-100 inclusion was a top signal.

- Set Take-Profit (TP) and Stop-Loss (SL) levels to manage the extreme 10-15% daily swings common in SNDK.

Top 5 Risks to Watch for SanDisk Investors in 2026

To successfully navigate the 2026 market, investors must balance SanDisk's dominant position in the AI memory supercycle against these five critical macro and operational headwinds.

- TurboQuant Software Efficiency: Continued advancements in model compression could lower the total addressable market for NAND.

- Hyperscaler CapEx Digestion: After a massive 2025-2026 buildout, big tech firms may enter a digestion phase where they stop buying new hardware.

- Cyclical Maturity: Historically, every memory boom ends in a supply glut. Watch for any expansion in production capacity from Samsung or SK Hynix.

- Geopolitical Supply Chains: With manufacturing concentrated in Asia, any escalation in regional tensions could disrupt SanDisk's sold out inventory.

- Regulatory Scrutiny: As a dominant AI component provider, SanDisk could face antitrust or export restriction hurdles in specific regional markets.

Final Thoughts: Should You Invest in SanDisk (SNDK) in 2026?

SanDisk in 2026 represents a pivotal transition from a cyclical commodity manufacturer to a high-margin pillar of AI infrastructure. While its 20x forward P/E is a significant departure from historical norms for the memory sector, it reflects a unique period of extreme pricing power and 65% gross margins that mimic software-like profitability. For the practical investor, the April 30, 2026, earnings release serves as the definitive proof of concept; it will determine whether the AI supercycle can fundamentally sustain a four-digit share price or if the recent Nasdaq-100 inclusion surge marks a technical exhaustion point.

In a market defined by the Agentic Web, SanDisk’s performance is no longer tied to consumer electronics but to the capital expenditure cycles of global hyperscalers. Investors should prioritize monitoring Enterprise SSD bit shipments and management’s commentary on NAND pricing sustainability post-April 20. For those seeking exposure, the current $913 level offers a high-conviction entry point for structural bulls, while conservative traders may prefer to wait for the post-earnings digestion phase to see if the $850 support level holds against potential software-driven demand efficiencies.

Risk Reminder: Trading and investing in equities like SNDK involves a significant risk of capital loss. The memory industry is notoriously cyclical, and past 2,700% gains are no guarantee of future returns. SanDisk’s performance is highly sensitive to hyperscaler CapEx shifts, hardware efficiency breakthroughs like TurboQuant, and evolving global supply chain dynamics. Always conduct independent due diligence or consult a financial advisor before allocating capital.

Related Reading

- Nasdaq 100 (NAS100) Forecast 2026: 27,000 AI Breakthrough or 22,000 Stagflation Trap?

- Micron (MU) Stock Price Forecast 2026: Can AI Memory and DRAM Demand Push MU to $500?

- TSMC (TSM) Price Prediction 2026: AI Monopoly or Geopolitical Trap at $480?

- Intel (INTC) Stock Forecast 2026: Foundry Breakthrough to $89 or Value Trap?

- ASML Holding (ASML) Stock Price Forecast 2026: AI Infrastructure King or Geopolitical Target?