In April 2026, JPMorgan Chase & Co. (JPM) is executing a massive $105 billion operational bet. While competitors retrench, JPM has deliberately absorbed a $9 billion expense increase to fuel a tech-first transformation. Despite a 10.6% year-to-date pullback to $297.40, the firm remains the flight-to-quality benchmark. Investors are currently split: Bulls cite the integration of 12 million Apple Card users and a record Net Interest Income (NII) forecast as catalysts for a breakout to $350+, while skeptics point to a 35% recession probability and $19.8 billion in spending as priced for perfection.

As the April 14, 2026, earnings report looms, JPM is positioning itself beyond traditional banking. With CEO Jamie Dimon signaling a potential entry into prediction markets and the bank's AI production use cases doubling year-over-year, JPM is evolving into a tech-financial hybrid. This guide breaks down the JPM stock price prediction for 2026 using data from TIKR, Zacks Research, Barchart, and 24/7 Wall St.

You will also discover how to gain exposure to JPMorgan Chase (JPM) stock futures through BingX TradFi.

Top 5 Things for JPMorgan Investors to Know in 2026

-

The $104.5B NII Record: JPM has raised its 2026 Net Interest Income guidance to a staggering $104.5 billion, front-running a higher-for-longer rate environment driven by energy-driven inflation.

-

Apple Card Integration: The definitive agreement to acquire the $20 billion Apple Card portfolio adds massive scale, though it triggered a $2.2 billion reserve build that temporarily masked earnings strength.

-

The AI Multiplier: A $19.8 billion technology budget has already identified $600 million in efficiency savings, validating the bank's strategy that sustained investment drives long-term margin expansion.

-

The $5B Legal Shadow: A lawsuit filed regarding the alleged debanking of political entities continues to weigh on retail sentiment, acting as a headline risk through mid-2026.

-

Direct Lending Pivot: JPM has earmarked $50 billion for private credit/direct lending initiatives to combat the rise of shadow banking and capture market share in distressed credit.

What Is JPMorgan Chase & Co. (JPM)?

JPMorgan Chase & Co. is the largest bank in the United States by assets, worth $4.4 trillion as of April 2026, and a Global Systemically Important Bank (G-SIB). Operating through four primary segments, Consumer & Community Banking, Commercial & Investment Bank, Asset & Wealth Management, and Corporate, it serves as the ultimate lender of last resort.

Under the leadership of Jamie Dimon, JPM has maintained a fortress balance sheet with a CET1 capital ratio of 15.1%. Its competitive moat is built on unmatched scale, allowing it to outspend rivals on innovation while maintaining a 19% Return on Tangible Common Equity (ROTCE).

JPMorgan enters Q1 2026 with an EPS consensus of $5.42, marking a 6.9% year-over-year increase that signals robust profitability despite a massive $105 billion spending plan. While the stock's 13x forward P/E sits at the higher end of its historical valuation, projected revenues of $48.2 billion and a record $104.5 billion Net Interest Income (NII) suggest that the bank’s aggressive investment in AI and the Apple Card integration is successfully generating operating leverage. With a steady 2.0% dividend yield and a lean 52% efficiency ratio, the firm continues to trade as a premium fortress asset capable of outperforming the broader financial sector during periods of economic volatility.

JPMorgan’s 2026 Strategy: The Scale Compounder

-

Prediction Markets Entry: Jamie Dimon hinted at offering regulated prediction markets for institutional clients, potentially legitimizing a sector currently dominated by Polymarket and Kalshi.

-

International Digital Dominance: Following the profitability of Chase UK, the bank is launching a digital retail offering in Germany in Q2 2026, bypassing the need for physical branches.

-

Fortress AI: Unlike traditional IT spend, JPM’s $19.8 billion budget is focused on LLMs for fraud detection and automated tax strategies, aiming to transform from a lender into a tech-first juggernaut.

JPM Stock 2026 Investment Outlook: $400 Alpha vs. $245 Execution Risk

The 2026 outlook for JPM is a battle between its industry-leading earnings power and the macro risks of a 35% recession probability.

The Bull Case: JPM’s $400 Blue-Chip Breakout

The bullish narrative centers on a massive valuation re-rating driven by positive jawboning from the April 14 earnings call. If management confirms that the $9 billion expense surge has peaked, the market will likely pivot from penalizing the spend to pricing in the $104.5 billion NII record. A Q1 EPS beat above the $5.42 consensus would validate the $19.8 billion AI budget, particularly if the identified $600 million in efficiency savings scales toward a $1.5 billion annualized run rate. This conversion of high-octane investment into margin expansion supports the TIKR projection of $29.78 normalized EPS by 2030, suggesting the current price is a deep discount for a tech-leveraged financial powerhouse.

To hit the $400 psychological ceiling, JPMorgan must demonstrate predatory stability by weaponizing its $1.4 trillion liquidity hoard. In this scenario, JPM capitalizes on private credit market stress and commercial real estate (CRE) volatility to acquire distressed, high-quality assets at deep discounts, essentially repeating the First Republic playbook. The integration of 12 million Apple Card users acts as a low-cost customer acquisition engine, driving cross-selling in wealth management and personal lending. If the bank maintains a 19%+ ROTCE while growing its asset base toward $5 trillion, the 'Dimon Premium' will likely push the stock toward a 15x–16x forward multiple, a rare tier for mega-cap banks.

The Base Case: JPMorgan’s $335 Fair Value Consolidation

The base case positions JPMorgan as the ultimate market compounder, expected to reach a mean analyst target of $334.53, a roughly 13% upside. This outlook assumes the higher-for-longer interest rate regime persists with a neutral Fed rate of 3.50%–3.75%, allowing JPM to maintain fat lending spreads despite the $105 billion operational expense load. Revenue is projected to track steadily at $48.2 billion for Q1, supported by mid-to-high teens growth in investment banking fees and resilient equities trading revenue, which recently surged 40%. Here, JPM tracks the S&P 500 Financials Index but remains the gold standard with significantly lower volatility.

Technically, the JPMorgan stock enters a period of high-floor consolidation as it absorbs the $2.2 billion Apple Card reserve build. While capital requirements remain a point of discussion, the Fed’s signals to scale back Basel III mandates unlock billions in potential share buybacks, with analysts anticipating a $25 billion to $30 billion program announcement later this year. For investors, this scenario offers a reliable 2.0% dividend yield and steady price appreciation, where JPM’s 52% efficiency ratio continues to lead the peer group. It is a 'steady-as-she-goes' narrative where scale serves as a protective moat against minor macro headwinds.

The Bear Case: JPM Stock at $245 Amid Credit Cycle Turn

The bear case is triggered by a macro-skunk entering the party: an energy-driven inflation shock where oil sustains levels above $115 per barrel. Such a spike would likely push JPMorgan’s internal 35% recession probability toward a 100% certainty, forcing a massive shift from capital deployment to defensive provisioning. In this risk-off environment, the $2 trillion private credit market could see a redemption surge, and JPM’s recent loan markdowns would serve as a lead indicator for a systemic credit turn. If credit card delinquencies exceed the expected 3.4%, the bank would be forced to aggressively hike loss reserves, erasing the projected 6.9% earnings growth.

Under this pressure, JPM’s stock would likely test its 52-week floor of $202–$211 before settling near the $245 support level. The primary catalyst for a downward spiral would be valuation multiple compression if investors perceive the $105 billion spending plan as a sunk cost that failed to provide a buffer against a hard landing. Furthermore, a $5 billion debanking lawsuit loss or regulatory gold-plating of capital rules could restrict the bank's ability to return capital to shareholders. In this scenario, the premium 13x forward multiple evaporates, and the stock is priced as a traditional lender exposed to a deteriorating consumer credit cycle rather than an AI-protected fortress.

Read more: Crude Oil Price Forecast 2026: $140 War Premium or $60 Surplus Baseline?

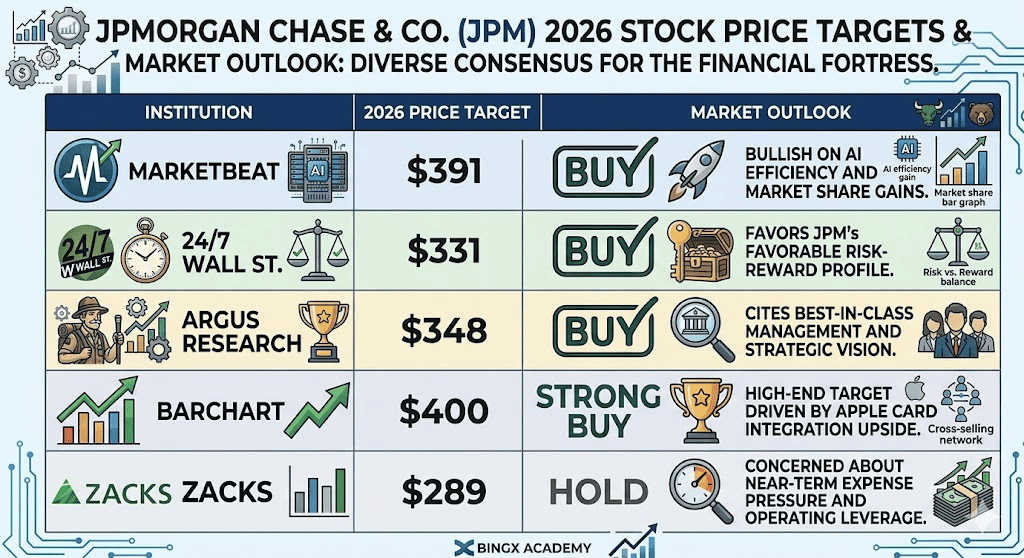

JPMorgan Stock Price Forecasts for 2026 By Wall Street Analysts

| Institution | 2026 Price Target | Market Outlook |

| MarketBeat | $391 | Buy: Bullish on AI and market share gains. |

| 24/7 Wall St. | $331 | Buy: Favors JPM’s risk-reward profile. |

| Argus Research | $348 | Buy: Cites best-in-class management. |

| Barchart | $400 | Strong Buy: High-end target on Apple Card upside. |

| Zacks | $289 | Hold: Concerned about near-term expense pressure. |

How to Trade JPMorgan (JPM) Stock on BingX

Navigate the volatility of JPMorgan’s earnings using BingX TradFi and BingX AI tools. By leveraging advanced AI-driven predictive analytics, you can better anticipate market sentiment shifts and price action ahead of the April 14 release.

JPM/USDT perpetual futures on BingX TradFi

Long or Short JPM Stock Futures on BingX

-

Navigate to BingX TradFi and select Stock Futures.

-

Select the JPM/USDT perpetual contract.

-

Set your leverage (e.g., 2x–5x) and select Open Long if you expect an NII beat, or Open Short to hedge against recession risks.

-

Set Take-Profit (TP) and Stop-Loss (SL) levels before the earnings release.

Top 5 Risks to Watch for JPM Investors in 2026

To successfully navigate the 2026 market, investors must balance JPMorgan’s tech-driven dominance against these five critical macro and operational headwinds.

-

Succession Uncertainty: As Jamie Dimon approaches his transition to Executive Chairman, any perceived weakness in the Lake vs. Rohrbaugh race could cause multiple compression.

-

Private Credit Contagion: Systemic stress in the $2 trillion private credit market could impact JPM’s loan marks.

-

Regulatory 'Whack-a-Mole': While Basel III requirements were scaled back, new scrutiny on AI-driven bank runs could introduce fresh compliance costs.

-

Energy-Driven Inflation: $100+ oil on geopolitical tensions threatens the soft landing narrative, potentially forcing the Fed into a restrictive stance that hurts credit quality.

-

Cybersecurity Threats: As the world's most systemic bank, JPM remains the primary target for state-sponsored cyberattacks, requiring constant capital allocation.

Final Thoughts: Should You Invest in JPMorgan (JPM) Stock in 2026?

JPMorgan Chase in 2026 represents a calculated transition from a traditional financial giant to an AI-augmented tech-first juggernaut. While the 13x forward P/E multiple reflects a premium relative to its peers, this valuation is underpinned by an industry-leading 19% ROTCE and the strategic absorption of the Apple Card’s 12 million users. For investors, the April 14, 2026, earnings release serves as the definitive proof of concept: it will reveal whether the $9 billion expense increase is actively yielding the projected operating leverage or if the fortress balance sheet is being pressured by a shifting credit cycle.

Practically, JPM remains a core flight-to-quality asset for those prioritizing scale and defensive stability during geopolitical volatility. However, the potential for a hard landing driven by $100+ oil and private credit markdowns suggests that entry timing is critical. Conservative traders may find value in monitoring the $287 support level before initiating long-term positions, while those seeking alpha should look for confirmation that Net Interest Income (NII) is tracking toward the record $104.5 billion target.

Risk Reminder: Trading and investing in equities like JPM involves a significant risk of capital loss. The bank’s performance is highly sensitive to Federal Reserve interest rate pivots, global energy prices, and evolving regulatory capital requirements. Historical performance is not indicative of future results; always conduct independent due diligence or consult a financial advisor before allocating capital.

Related Reading

1. Goldman Sachs (GS) Price Prediction 2026: Strategic Renaissance or Value Trap at $860?

2. Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

3. GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?

4. Accenture (ACN) Outlook 2026: Can AI Transformation and Consulting Demand Drive ACN Stock to $450+?

5. Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?