Arbitrage is the practice of simultaneously exploiting price differences for the same asset across different markets or trading pairs to generate a risk-free (or near risk-free) profit. In crypto spot markets, the most commonly discussed form is triangular arbitrage, a three-leg trade that cycles through multiple pairs, for example, BTC → ETH → USDT → BTC, to profit from momentary pricing inefficiencies between the pairs. While the concept is simple, the execution is more nuanced than most guides reveal.

This article explains exactly how it works, why most retail arbitrage opportunities are smaller than they appear, and where genuine opportunities still exist.

What Is Arbitrage Trading?

Arbitrage is one of the oldest trading strategies in financial markets.

The core idea: if the same asset is priced differently in two places simultaneously, you can buy it cheaply in one place and sell it at a higher price in another, capturing the difference as profit without taking directional market risk.

In traditional finance, arbitrage kept markets efficient as the moment a price discrepancy appeared, arbitrageurs would close it within milliseconds.

In crypto, markets are more fragmented, trading 24/7 across hundreds of exchanges and thousands of pairs, creating more frequent and persistent pricing inefficiencies but also attracting sophisticated automated systems that close those gaps just as quickly.

Read more: What Is Crypto Arbitrage and How to Make Low-Risk Gains?

Why Crypto Markets Create Arbitrage Opportunities

Arbitrage opportunities in 2026 arise from the inherent fragmentation of liquidity across global decentralized and centralized venues, where millisecond delays in information propagation create temporary price inefficiencies for the observant trader.

|

Factor |

Why it creates arbitrage |

|

Fragmented liquidity |

Prices on BingX, Binance, Coinbase, and Kraken can diverge briefly |

|

24/7 trading |

No single open/close resets pricing globally |

|

Thousands of pairs |

Cross-pair relationships can go out of sync momentarily |

|

Varying liquidity depth |

Low-liquidity pairs show wider price deviations |

|

Different fee structures |

Different exchanges price assets slightly differently to reflect their costs |

|

New listings |

Newly listed assets have less efficient pricing |

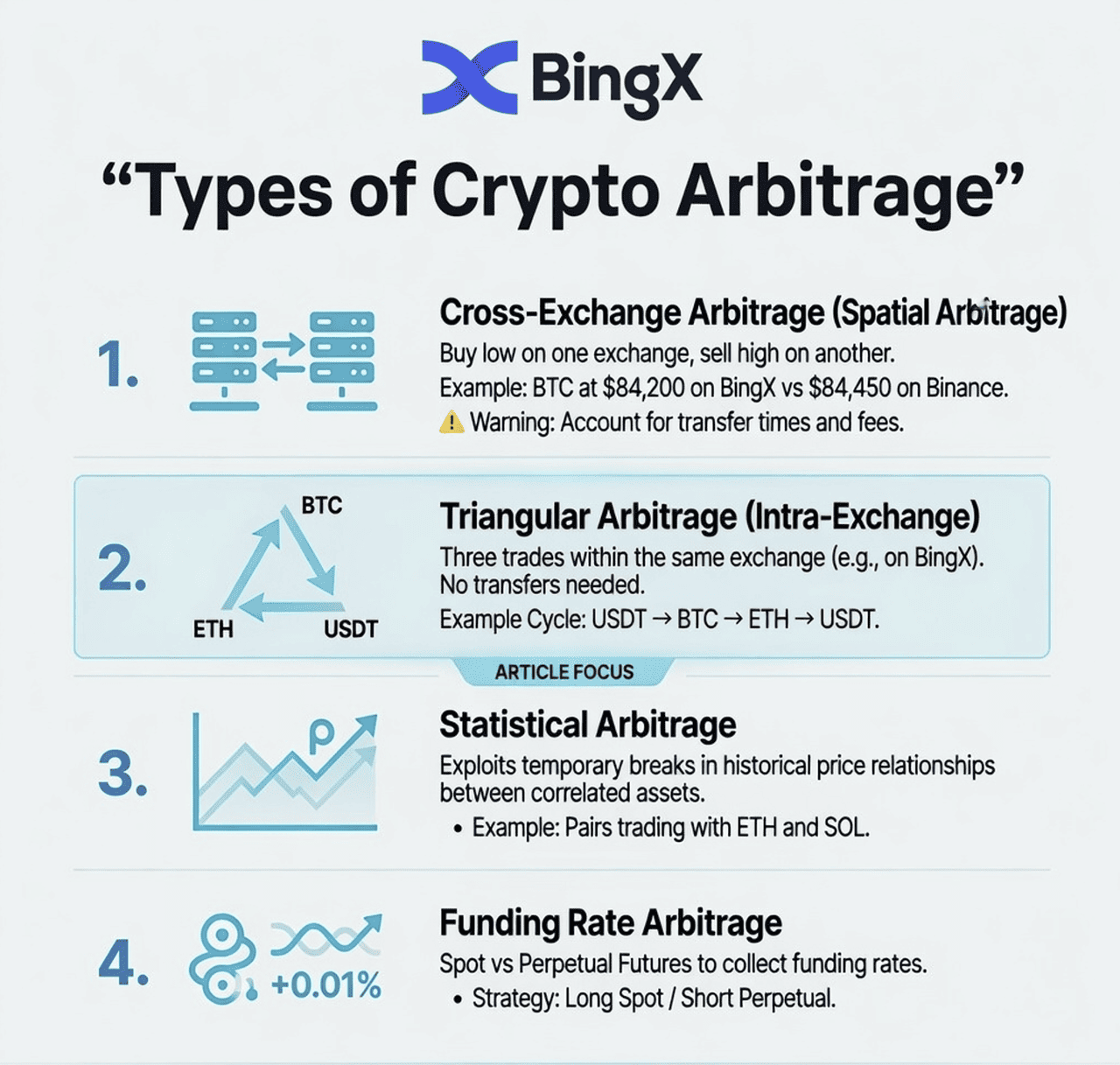

What Are the Different Types of Crypto Arbitrage?

Before diving into triangular arbitrage specifically, it helps to understand the full landscape of crypto arbitrage strategies:

1. Cross-Exchange Arbitrage: Spatial Arbitrage

Buy an asset on one exchange where it is priced lower, and simultaneously sell it on another exchange where it is priced higher.

Example: BTC trades at $84,200 on BingX and $84,450 on Binance simultaneously. Buy on BingX, sell on Binance, profit: approx 250 per BTC before fees and transfer costs.

The catch: Transferring funds between exchanges takes time (blockchain confirmation times), during which the price gap can close or reverse. Most cross-exchange arbitrage requires pre-positioning funds on both exchanges simultaneously.

2. Triangular Arbitrage: Intra-Exchange

Execute three sequential trades within the same exchange to exploit a mispricing between three related pairs.

Example: BTC → ETH → USDT → BTC on BingX. If the implied rates across these three trades don't net to exactly 1, a profit or loss exists.

This is the focus of this article. It requires no cross-exchange transfer and can be executed entirely within BingX.

3. Statistical Arbitrage

A quantitative strategy that exploits historical price relationships between correlated assets (e.g., BTC and ETH tend to move together). When the correlation temporarily breaks, a pairs trade is entered expecting the relationship to revert.

This requires statistical modelling and is beyond the scope of this article.

4. Funding Rate Arbitrage: Futures vs. Spot

When perpetual futures funding rates are high, traders buy the asset spot and simultaneously short the futures contract, collecting the funding rate as near-risk-free yield while the positions offset each other.

This is not technically spot arbitrage but is widely used in crypto.

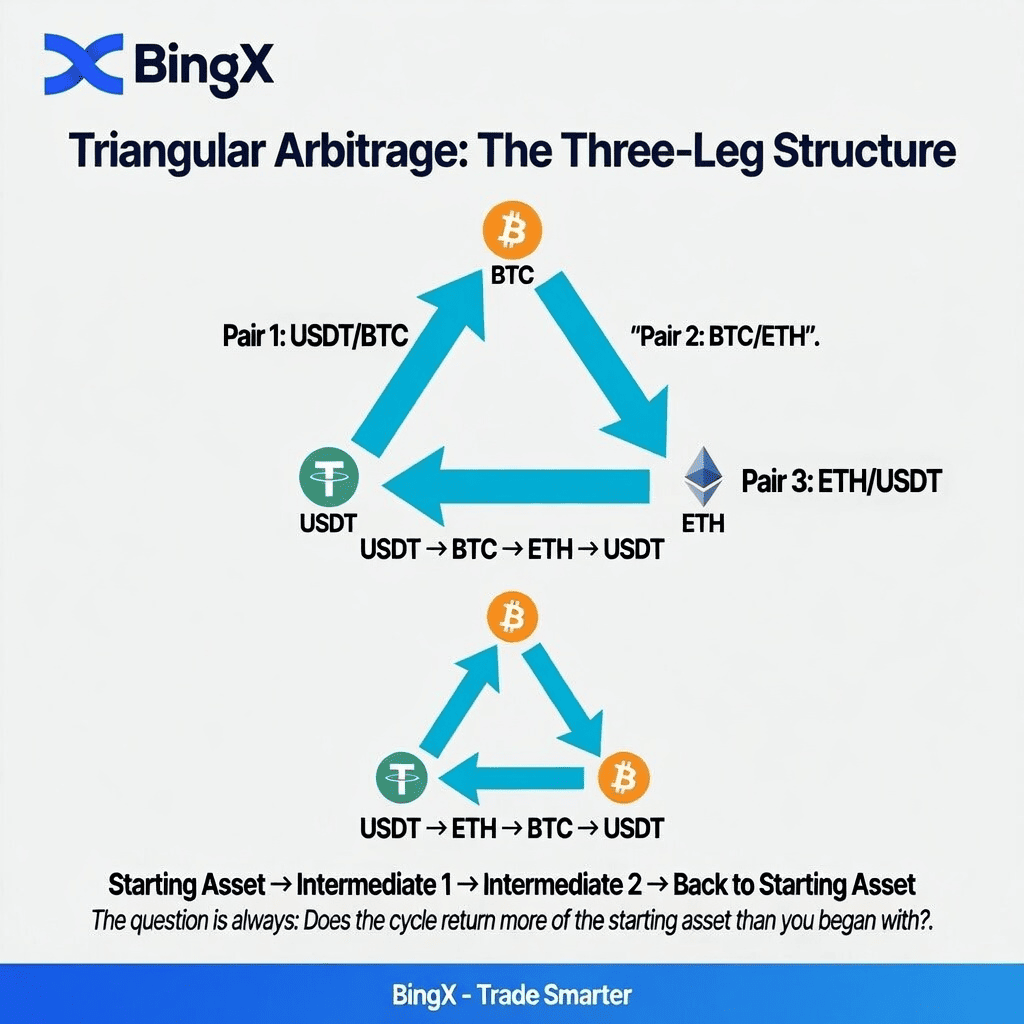

What Is Triangular Arbitrage and How to Use It on BingX: Step by Step

Triangular arbitrage is a three-trade cycle that begins and ends with the same asset. If the cycle produces more of that asset than you started with (after fees), a profit has been captured.

How Triangular Arbitrage Works: The Three-Leg Structure

Starting asset → Pair 1 → Intermediate asset → Pair 2 → Second intermediate → Pair 3 → Starting asset

Most common example:

USDT → BTC → ETH → USDT

Or in reverse:

USDT → ETH → BTC → USDT

The question is always: does the cycle return more USDT than you started with?

Why the Mispricing Happens

On any exchange, three related pairs must be consistent with each other.

For BTC/USDT, ETH/USDT, and ETH/BTC, the following relationship must hold for the market to be perfectly efficient:

ETH/BTC price = ETH/USDT price ÷ BTC/USDT price

When this relationship breaks, even briefly, a triangular arbitrage opportunity exists. Market makers and automated bots constantly monitor this and close gaps in milliseconds, but during periods of high volatility or low liquidity, small discrepancies can persist for a few seconds.

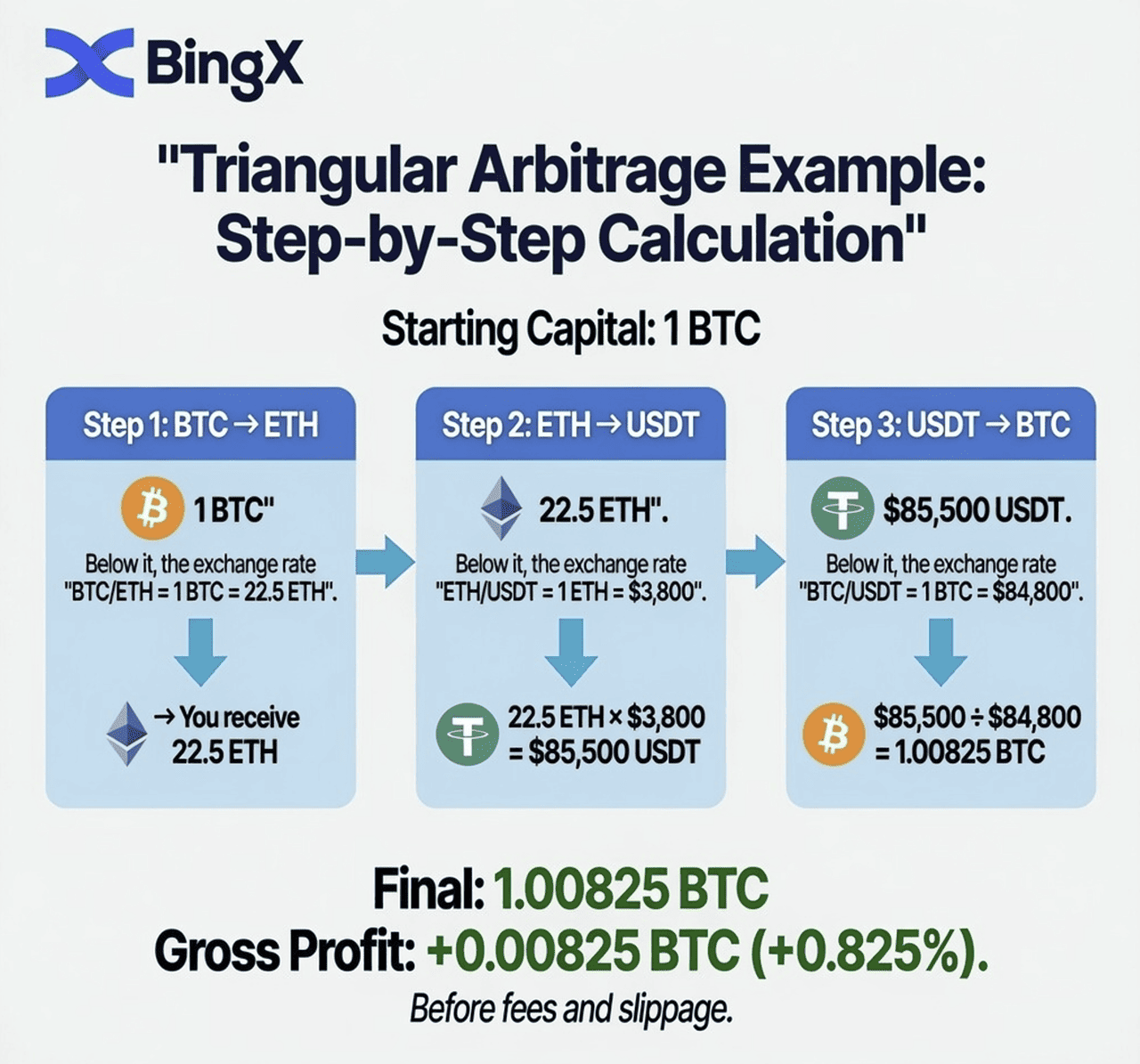

An Example of Triangular Arbitrage: BTC → ETH → USDT → BTC

Let's walk through a complete calculation using illustrative prices that show a small discrepancy.

Starting capital: 1 BTC Exchange: BingX spot market

Step 1: BTC → ETH

- BTC/ETH price: 1 BTC = 22.5 ETH

- After selling 1 BTC: 22.5 ETH

Step 2: ETH → USDT

- ETH/USDT price: 1 ETH = $3,800

- After selling 22.5 ETH: $85,500 USDT

Step 3: USDT → BTC

- BTC/USDT price: 1 BTC = $84,800

- After buying BTC: 85,500 ÷ 84,800 = 1.00825 BTC

Gross profit: +0.00825 BTC (0.825% gain before fees)

Fee Adjustment: The Reality Check

With BingX's spot taker fee of 0.1% per trade across three legs:

Fee cost = 0.1% × 3 trades = 0.3% of capital

Fee-adjusted result:

- Gross gain: +0.825%

- Fee cost: −0.3%

- Net profit: +0.525%

At 1 BTC (~$84,800), this nets approximately $445 profit from a single arbitrage cycle — if the opportunity was genuinely available.

The Reverse Cycle

The same three pairs can be traded in reverse if the mispricing is in the other direction:

USDT → ETH → BTC → USDT

Step 1: Buy ETH with USDT (ETH/USDT)

Step 2: Sell ETH for BTC (ETH/BTC)

Step 3: Sell BTC for USDT (BTC/USDT)

Both directions must be tested. The direction that returns more than 1.00 (after fees) is the profitable leg.

How Profitable Is Triangular Arbitrage Strategy?

Before executing any triangular arbitrage cycle, calculate whether a genuine profit exists after fees. Use this framework:

Step 1: Calculate the implied ETH/BTC rate from the USDT pairs:

Implied ETH/BTC = ETH/USDT price ÷ BTC/USDT price

Step 2: Compare to the actual ETH/BTC spot price on the exchange:

If (implied rate > actual rate): trade USDT → BTC → ETH → USDT

If (implied rate < actual rate): trade USDT → ETH → BTC → USDT

Step 3: Calculate the gross profit ratio:

Profit ratio = (implied rate / actual rate) - 1

Step 4: Subtract total fees:

Net profit = Profit ratio - (fee rate × 3)

Step 5: Execute ONLY if Net profit > 0

For example:

- BTC/USDT: $84,800

- ETH/USDT: $3,810

- ETH/BTC actual: 0.04490

- ETH/BTC implied: 3,810 / 84,800 = 0.04493

Implied (0.04493) > Actual (0.04490) → Trade: USDT → ETH → BTC → USDT

Profit ratio: (0.04493 / 0.04490) - 1 = 0.067%

Fee cost (3 × 0.1%): 0.3%

Net profit: 0.067% - 0.3% = -0.233% ← LOSS, do not execute

This is the most important lesson: most apparent triangular arbitrage opportunities disappear after fees. The price discrepancy must be larger than your total fee cost (typically 0.3% for three spot trades) to be profitable.

The Hard Truth About Retail Triangular Arbitrage: Key Considerations

Here is what most arbitrage guides don't tell you clearly:

1. You Are Competing Against Automated Bots

Every major exchange, including BingX, has automated market-making algorithms and arbitrage bots monitoring price relationships in real time. These bots execute in milliseconds. By the time a retail trader manually spots a triangular arbitrage opportunity, opens three trade windows, and executes the orders, the opportunity has almost certainly closed.

2. The Gap Must Exceed Your Total Fees

For three BingX spot trades at 0.1% each, the minimum profitable discrepancy is >0.3% before slippage. Genuinely exploitable discrepancies of this size are rare and brief on high-liquidity pairs.

3. Slippage Reduces Profits Further

For large trades, the act of buying or selling moves the price against you. A $100,000 triangular arbitrage trade on a pair with moderate liquidity will experience slippage on all three legs — potentially turning a theoretical 0.4% gain into a 0.1% gain or a loss.

4. Execution Must Be Near-Simultaneous

Triangular arbitrage requires all three legs to be executed as close to simultaneously as possible. If BTC/ETH moves against you between leg 1 and leg 2, the trade loses money. Manual execution introduces execution risk that automated systems don't have.

Do Genuine Arbitrage Opportunities Still Exist in Crypto?

Despite these challenges, real triangular arbitrage opportunities do occur in crypto:

- During high-volatility events: When markets move sharply, pricing relationships temporarily break down across pairs

- On lower-liquidity pairs: Newer or smaller trading pairs have less efficient pricing and wider discrepancies

- At exchange open after maintenance periods: When an exchange resumes trading after a pause, pricing may be momentarily misaligned

- For well-capitalised traders using APIs: Connecting to BingX's API and executing trades programmatically is significantly faster than manual execution

Top Cross-Pair Arbitrage Opportunities on BingX Spot

Rather than the highly competitive BTC/ETH/USDT triangle, less-traded triangles sometimes offer better opportunities:

Lower-Competition Triangles to Monitor

|

Factor |

Why it creates arbitrage |

|

Fragmented liquidity |

Prices on BingX, Binance, Coinbase, and Kraken can diverge briefly |

|

24/7 trading |

No single open/close resets pricing globally |

|

Thousands of pairs |

Cross-pair relationships can go out of sync momentarily |

|

Varying liquidity depth |

Low-liquidity pairs show wider price deviations |

|

Different fee structures |

Different exchanges price assets slightly differently to reflect their costs |

|

New listings |

Newly listed assets have less efficient pricing |

How to check for triangular opportunities on BingX:

- Open BingX Spot and note the current prices for all three pairs in your triangle

- Calculate the implied cross-rate vs the actual cross-rate using the formula above

- If the discrepancy is greater than 0.35–0.4% (to cover fees and slippage), the opportunity may be viable

- Execute all three legs as quickly as possible, ideally using limit orders placed simultaneously in separate windows

How to Identify Trianglular Arbitrage Opportunities on BingX: Step-by-Step

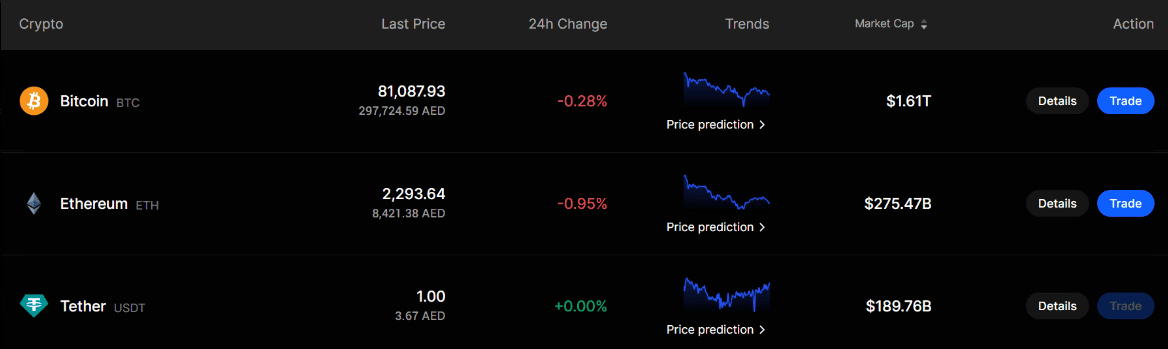

Arbitrage in spot markets means checking whether the same value is priced differently across related trading pairs. In this example, we use the prices shown in the BingX screenshot for BTC, ETH, and USDT to understand whether a triangular arbitrage opportunity may exist.

|

Asset |

Price shown |

|

Bitcoin BTC |

$81,087.93 |

|

Ethereum ETH |

$2,293.64 |

|

Tether USDT |

$1.00 |

The triangle we are checking is: USDT → ETH → BTC → USDT

Step 1: Calculate the Implied ETH/BTC Price

To find the fair ETH/BTC rate, divide the ETH/USDT price by the BTC/USDT price.

Formula: Implied ETH/BTC = ETH/USDT ÷ BTC/USDT

Calculation: $2,293.64 ÷ $81,087.93 = 0.02828 BTC

This means that based on the screenshot prices, 1 ETH should be worth around 0.02828 BTC.

Step 2: Compare with Actual ETH/BTC Price

Now open the ETH/BTC spot pair on BingX and check the live price.

For example, assume the actual ETH/BTC price on BingX is: Actual ETH/BTC = 0.02845 BTC

Now compare it with the implied rate: Actual ETH/BTC: 0.02845 and Implied ETH/BTC: 0.02828

The actual price is higher than the implied price.

Difference: 0.02845 ÷ 0.02828 - 1 = 0.58%

So, ETH is trading around 0.58% higher against BTC than the BTC/USDT and ETH/USDT prices suggest.

Step 3: Run the Trade Cycle

Assume you start with 10,000 USDT. First, buy ETH using USDT: 10,000 ÷ 2,293.64 = 4.3598 ETH

Next, sell ETH into BTC at the actual ETH/BTC price: 4.3598 × 0.02845 = 0.12403 BTC

Finally, sell BTC back into USDT: 0.12403 × 81,087.93 = 10,058.04 USDT

Step 4: Calculate Gross Profit

You started with: 10,000 USDT

You ended with: 10,058.04 USDT

Gross profit: 10,058.04 - 10,000 = 58.04 USDT

That equals around 0.58% gross profit before fees.

Step 5: Adjust for Trading Fees

If the spot trading fee is around 0.10% per trade, then three trades may cost around 0.30% total.

Estimated net result: 0.58% gross gap - 0.30% fees = 0.28% net profit

On a 10,000 USDT cycle, that would be approximately: 10,000 × 0.28% = 28 USDT net profit

Simple Takeaway

In this example, the arbitrage only works because the actual ETH/BTC price is higher than the implied ETH/BTC rate. The trader buys ETH with USDT, converts ETH into BTC at the stronger ETH/BTC rate, and then sells BTC back into USDT.

However, this is only profitable if the price difference is large enough to cover:

- Trading fees

- Bid and ask spread

- Slippage

- Execution delay

- Partial order fills

That is why beginners should first practice the calculation manually before attempting live arbitrage.

API Method for Serious Arbitrage

For traders who can code, BingX's API allows programmatic access to order placement:

- Monitor real-time price feeds for all three pairs simultaneously

- Calculate implied vs actual cross-rates continuously

- Trigger all three orders automatically when a profitable discrepancy appears

- Execute in milliseconds rather than seconds

This is how genuine arbitrage is conducted at scale.

What Are the Risks of Spot Arbitrage Trading?

Despite being described as risk-free in theory, crypto spot arbitrage carries real risks:

- Execution risk: Between placing the first and third order, prices can move against you — especially during high volatility. What looked like a 0.5% gain can become a loss if the middle pair moves unfavourably.

- Liquidity risk: If your order doesn't fill at your expected price, you are exposed. A large order in a thin market can move the price significantly, closing the gap before your cycle is complete.

- Fee miscalculation: Forgetting to include all three fee legs, slippage, or any platform-specific costs can turn an apparent profit into a loss.

- Technology risk: Manual execution is slow. API execution depends on reliable connectivity and code that handles edge cases correctly.

- Capital requirements: Small discrepancies require large capital to generate meaningful profits. A 0.2% net gain on $1,000 is $2. On $100,000, it's $200. Arbitrage is a volume game.

Is Crypto Arbitrage Legal?

Yes, crypto arbitrage is entirely legal. It is a standard market mechanism that improves price efficiency across markets. Regulators in all major jurisdictions allow it. Exchanges explicitly permit it in their terms of service.

Arbitrage is not market manipulation. You are not creating artificial price movements, you are responding to existing price discrepancies and closing them, which makes markets more efficient for all participants.

The only exception would be if arbitrage were used in conjunction with market manipulation (e.g., coordinating with someone to artificially create a discrepancy then arbitrage it) but pure arbitrage between legitimate markets is always legal.

Conclusion

Triangular arbitrage is elegant in theory: a self-contained, three-leg trade cycle that starts and ends with the same asset and profits from pricing inconsistencies between related pairs. In practice, it requires either sophisticated automation to compete with market-making bots, or patient monitoring for the relatively rare moments when discrepancies are large enough to survive fees and slippage.

For most retail traders on BingX, the value in understanding triangular arbitrage is not the strategy itself. It is the understanding it builds of how crypto markets are interconnected. When you understand that ETH/BTC, ETH/USDT, and BTC/USDT are all related and must be consistent, you see the market with greater clarity. That understanding improves every trade, not just the ones that explicitly exploit discrepancies.

Related Articles

- What Is Crypto Arbitrage and How to Make Low-Risk Gains?

- What Is Funding Rate Arbitrage in Crypto? A Complete Guide for Futures Traders

- Risk Management in Crypto Trading: 7 Rules Every Trader Must Know

- Crypto Chart Patterns: The Complete Guide for Traders

- What Are the Best Crypto Trading Bots?

- How to Keep a Trading Journal: A Complete Guide for Crypto Traders

- What Is Crypto Day Trading? A Beginner's Guide

- How to Use MACD in Crypto Trading

FAQs on Triangular Arbitrage

1. What is triangular arbitrage in crypto?

Triangular arbitrage is a three-leg trading strategy that cycles through three related trading pairs on the same exchange for example, USDT → BTC → ETH → USDT — to exploit momentary pricing inconsistencies between the pairs. If the cycle returns more of the starting asset than you began with (after fees), a profit has been captured without taking directional market risk.

2. How does triangular arbitrage work with BTC, ETH, and USDT?

You start with USDT, buy BTC, use that BTC to buy ETH, then sell ETH back for USDT. If the three exchange rates are not perfectly in sync, you either end up with more or less USDT than you started with.

The triangular arbitrage works when the implied ETH/BTC rate (calculated from the USDT pairs) differs from the actual ETH/BTC spot price by more than your total fees.

3. Is crypto arbitrage profitable?

Crypto arbitrage can be profitable, but the opportunities are smaller and shorter-lived than most retail traders expect. On high-liquidity pairs like BTC/ETH/USDT, automated bots close pricing gaps in milliseconds. For manual traders, the discrepancy must exceed your total fee cost (typically 0.3% for three spot trades) plus slippage to generate any profit. Genuine manual opportunities are rare on major pairs but more common on lower-liquidity alt pairs.

4. Is crypto arbitrage legal?

Yes, crypto arbitrage is completely legal in all major jurisdictions. It is a standard market mechanism that improves price efficiency. Exchanges explicitly permit it in their terms of service. Arbitrage is not market manipulation, it responds to existing price differences and helps close them, benefiting market efficiency.

5. What is the difference between triangular arbitrage and cross-exchange arbitrage?

Triangular arbitrage operates entirely within one exchange — you cycle through three pairs without moving funds between platforms. Cross-exchange arbitrage buys an asset on one exchange where it's cheaper and sells it on another where it's more expensive. Triangular arbitrage avoids the transfer delays and risks of cross-exchange arbitrage but requires near-simultaneous execution across three pairs.

6. What are the risks of triangular arbitrage?

The main risks are execution risk (prices move before all three legs fill), liquidity risk (insufficient order book depth causes slippage), fee miscalculation (forgetting all three fee legs), and technology risk (slow manual execution). Unlike the theoretical "risk-free" description, real-world triangular arbitrage carries genuine risks from imperfect execution.

7. How much capital do I need for crypto arbitrage?

Because price discrepancies are typically small (0.1–0.5%), you need significant capital to generate meaningful profits. A 0.3% net gain on $1,000 is $3. On $50,000, it's $150. Most retail arbitrage is done with $10,000+ positions to make the execution effort worthwhile. Algorithmic traders operate with much larger sums.

8. Can I automate triangular arbitrage on BingX?

Yes, BingX provides an API that allows programmatic order placement. Traders with coding skills can build automated systems that monitor real-time price feeds for all three pairs simultaneously, calculate the implied vs actual cross-rates continuously, and execute all three orders in milliseconds when a profitable opportunity appears. Manual execution is significantly slower and less competitive.

9. What is the minimum price discrepancy needed for triangular arbitrage to be profitable on BingX?

For three spot trades at BingX's standard 0.1% taker fee, the minimum gross discrepancy is 0.3% (three legs × 0.1% each). In practice, you should target discrepancies of 0.35–0.5%+ to also account for slippage and execution imperfections. Anything below 0.3% will result in a net loss after fees.