In April 2026, GE Aerospace (GE) stands at a strategic crossroads. After completing its historic de-conglomeration with the spin-off of GE Vernova in 2024, the company has transformed into a high-margin, pure-play aviation leader. While its financial engine is firing on all cylinders, boasting 26.6% operating margins in its commercial segment, the stock has recently hit a 15-week low of $281. Analysts are currently debating whether the Aerospace Super-Cycle can sustain a forward P/E of 39x, or if supply chain fragility and Boeing’s (BA) ongoing production struggles will clip GE’s wings in the latter half of 2026.

Despite the recent pullback, the fundamental razor and blade model remains the envy of the industrial world. With GE powering approximately 75% of the world’s narrow-body aircraft through its CFM International joint venture, the company is effectively a toll booth on global air travel. This guide breaks down the GE Aerospace stock price prediction for 2026 using data from JPMorgan, Morgan Stanley, and Wells Fargo.

You will also discover how to gain exposure to GE Aerospace (GE) stock futures through BingX TradFi.

Top 5 Things for GE Aerospace Investors to Know in 2026

- The $190B Backlog: GE enters 2026 with a massive order book that provides multi-year revenue visibility, primarily driven by the high-demand LEAP and GE9X engines.

- The Buyback Floor: A $15 billion share repurchase program and a 25% dividend hike announced in early 2026 act as significant price support during market volatility.

- Boeing Dependency: As the sole engine provider for the 737 MAX and 777X, GE’s short-term delivery targets are heavily tied to Boeing’s regulatory and production recovery.

- Service-Led Growth: High-margin Maintenance, Repair, and Overhaul (MRO) services now drive the majority of long-term profits, insulating GE from the cyclical nature of new aircraft sales.

- Valuation Priced for Perfection: Trading at nearly 40x forward earnings, GE is at a significant premium compared to the industry average of 23x, leaving little room for earnings misses.

What Is GE Aerospace (GE)?

GE Aerospace is the global leader in jet engines, components, and integrated systems for commercial and military aircraft. Following the successful spin-offs of GE HealthCare and GE Vernova, it is now a streamlined pure-play aviation company. Its competitive advantage lies in its installed base of approximately 50,000 commercial and 30,000 military engines.

The company's crown jewel is CFM International, a 50-50 joint venture with Safran, which produces the LEAP engine. This engine is the workhorse of modern aviation, powering the Boeing 737 MAX and half of the Airbus A320neo fleet. Beyond manufacturing, GE’s Flight Deck lean operating model, inspired by the Toyota Production System, focuses on operational excellence and reducing supply chain bottlenecks.

GE Aerospace’s Strategic Evolution: From Conglomerate to Aviation Pure-Play

- The De-Conglomeration (2018–2024): Under CEO Larry Culp, GE shed its debt-laden legacy businesses (GE Capital, Appliances, Power) to focus exclusively on aerospace.

- The Super-Cycle (2025–2026): Global aircraft shortages and aging fleets have forced airlines to fly older planes longer, skyrocketing GE’s high-margin service revenue.

- The Sustainable Future (2027+): The RISE Program (Revolutionary Innovation for Sustainable Engines) targets a 20% reduction in CO2 emissions, positioning GE to lead the industry’s Net Zero 2050 transition.

GE Aerospace (GE) Revenue Crosses $42B in 2025: A Record-Breaking Year

GE Aerospace (GE) stock performance in 2025 | Source: Yahoo Finance

- Revenue Growth: Full-year 2025 revenue hit $42.3 billion, a 21% increase year-over-year.

- Backlog Strength: Commercial engine orders surged 76% in late 2025, reaching a total backlog value of nearly $190 billion.

- Cash Generation: The company generated approximately $7.7 billion in free cash flow in 2025, more than doubling its previous year's performance.

- Stock Rally: GE shares surged 67% over the last 12 months before the March 2026 correction.

GE Aerospace (GE) 2026 Investment Outlook: The Backlog vs. Valuation

The 2026 investment landscape for GE Aerospace stock is a high-stakes tug-of-war between its unprecedented $190 billion commercial order book and a 'priced for perfection' valuation that leaves no room for operational stumbles.

The Bull Case: GE Stock’s $425 Blue-Chip Breakout

The bull narrative hinges on the seamless conversion of GE’s $190 billion backlog into realized revenue as supply chain constraints finally dissolve in the latter half of 2026. In this scenario, GE successfully scales LEAP engine production to meet 100% of demand from Airbus and a stabilizing Boeing, effectively capturing 75% of the narrow-body propulsion market. With the $1 billion U.S. manufacturing investment clearing production bottlenecks, operating margins in the Commercial Engines & Services (CES) segment could exceed 27%, fueled by an unprecedented volume of high-margin shop visits as airlines rush to modernize aging fleets.

From a capital allocation perspective, the bull case is electrified by the $15 billion share repurchase program, which has the potential to retire nearly 5-6% of the float at current valuations. This aggressive buyback, combined with a projected 2026 Adjusted EPS at the top of guidance above $7.40, creates a powerful EPS pop that forces a market re-rating. If the RISE program achieves its hybrid-electric testing milestones by mid-year, GE transitions from a traditional industrial stock to a high-growth Aero-Tech leader, justifying a premium 50x forward P/E and driving the price toward the $425 institutional target.

The Base Case: GE's $355 Steady Climb Consolidation

The base case assumes GE executes within its guided operating profit range of $9.85 billion to $10.25 billion, acting as a quality compounder despite lingering macro headwinds. While Boeing’s 777X certification delays (now expected in 2027) remain a minor drag on the wide-body segment, the high-margin services business, which grew 31% year-over-year in late 2025, provides a rock-solid earnings floor. In this outlook, the razor and blade model performs predictably: even if new engine deliveries are flat, the massive installed base of 50,000 commercial engines ensures a constant stream of recurring maintenance revenue.

For practical investors, this scenario is defined by steady capital returns rather than explosive multiple expansion. With a fortress-like balance sheet and net debt effectively eliminated, GE is positioned to sustain its 25% dividend hike while tracking a modest 18x forward EV/EBITDA multiple. The stock likely recovers from its Q1 15-week low to settle near the analyst consensus of $355. Success here is measured by GE's ability to maintain a 1.0x book-to-bill ratio and steady progress on LEAP durability kits, which are designed to double time-on-wing for customers in harsh environments.

The Bear Case: GE Stock Dips to $280 on Margin Compression

The bear case is triggered by Inventory Quality red flags and a structural Privacy Cliff in supply chain transparency. If the inventory growth seen in Q4 2025, intended to support 2026 output, fails to convert due to Boeing production caps or FAA-mandated pauses, GE could face significant inventory write-downs. This would lead to a Forensic Red Flag event, where margin compression from liquidated parts or over-optimistic demand forecasting causes an earnings miss in H2 2026. Such a disruption would likely force the stock to test its $281 support level as institutional quality premiums evaporate.

Additionally, the re-emergence of tariff-related cost pressures and tighter Buy American requirements could inflate the cost of specialized raw materials, eroding the currently pristine 26.6% margins. If GE’s $1 billion reinvestment into domestic manufacturing fails to offset these rising costs, the market may de-rate the stock to a 10x–12x EV/EBITDA multiple, more in line with legacy industrial peers. In this pessimistic scenario, the stock loses its priced for perfection status and drifts toward the $280–$290 range, as investors seek safety in less volatile sectors until the aerospace supply chain proves its long-term resilience.

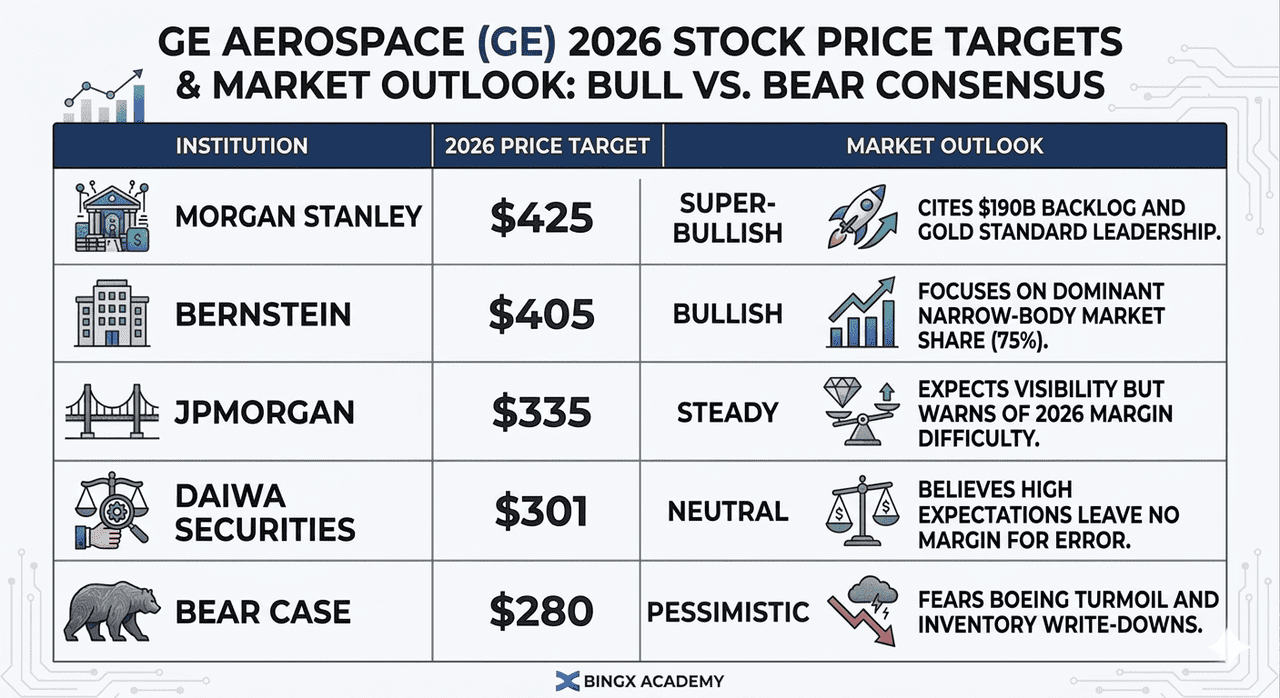

GE Aerospace (GE) Price Forecasts for 2026 By Wall Street Analysts

|

Institution |

2026 Price Target |

Market Outlook |

|

Morgan Stanley |

$425 |

Super-Bullish: Cites $190B backlog and Gold Standard leadership. |

|

Bernstein |

$405 |

Bullish: Focuses on dominant narrow-body market share (75%). |

|

JPMorgan |

$335 |

Steady: Expects visibility but warns of 2026 margin difficulty. |

|

Daiwa Securities |

$301 |

Neutral: Believes high expectations leave no margin for error. |

|

Bear Case |

$280 |

Pessimistic: Fears Boeing turmoil and inventory write-downs. |

How to Trade GE Aerospace (GE) Stock on BingX

Maximize your trading potential by using BingX's advanced TradFi tools and BingX AI insights to navigate GE’s earnings volatility.

GE/USDT perpetual contract on the BingX futures market

Long or Short GE Aerospace (GE) Stock Futures

- Navigate to BingX TradFi and select Stock Futures.

- Select the GE/USDT perpetual contract.

- Set your leverage (e.g., 2x–5x) and select Open Long if you expect a rebound or Open Short to hedge against supply chain risks.

- Set Take-Profit (TP) and Stop-Loss (SL) levels before the earnings release.

Top 5 Risks to Watch for GE Investors in 2026

While GE Aerospace holds a dominant market position, investors must navigate a high-stakes environment where valuation perfection meets a brittle global supply chain and shifting trade policies.

- The Boeing 777X Entry into Service (EIS) Cliff: As the exclusive engine provider for the 777X, any shift in the current early 2027 EIS target directly impacts the GE9X production ramp. Investors should monitor Boeing’s flight test milestones; a slip into late 2027 would defer billions in expected delivery revenue and increase inventory carry costs.

- Section 232 and Tariff Re-Emergence: With pending investigations into specialized medical and industrial equipment in 2025-2026, GE faces a margin squeeze from rising raw material costs. Increased compliance costs from tighter Buy American requirements could erode gross margins for critical engine components sourced through international partners like Safran.

- Inventory Quality and Forecasting Red Flags: Forensic analysts have flagged a disconnect between Q4 2025 inventory growth and realized cash flow. If GE’s demand forecasting proves over-optimistic, specifically regarding narrow-body delivery rates, the company may face significant inventory write-downs or liquidation events in late 2026.

- Tier 3 & 4 Supply Chain Bottlenecks: Despite a $1 billion reinvestment, the aerospace industrial base remains fragile. Shortages in high-temperature castings and forgings are the primary bottleneck; any failure by sub-tier suppliers to meet a 25% year-over-year delivery increase will cap GE’s ability to convert its $190 billion backlog into liquid profit.

- Enhanced Durability Mandates: Following recent reliability issues across the industry, the FAA and EASA have increased scrutiny on time-on-wing metrics. While the LEAP engine currently holds a 70% market share on the A320neo, any regulatory mandate for more frequent shop visits or hardware retrofits would drive up R&D expenses and strain MRO capacity.

Final Thoughts: Should You Invest in GE Aerospace (GE) Stock in 2026?

GE Aerospace in 2026 is a story of fundamental strength versus valuation gravity. At a forward P/E of 39x, it is no longer the cheap industrial play it was in 2021; it is now a premium asset priced for perfection. For investors, the earnings call coming up on April 21, 2026, is the critical litmus test. Specifically, monitoring whether the company can maintain its 26%+ commercial margins despite supply chain reinvestment will determine if the recent dip is a buying opportunity or a warning sign.

The $190 billion backlog provides a massive safety net, but the stock’s short-term momentum depends on Boeing’s stability and the successful ramp-up of LEAP production. If you believe in the multi-decade Aerospace Super-Cycle, GE remains the gold standard. However, conservative investors may wait for the P/E to compress closer to the 30x-35x range before building a full position.

Risk Reminder: Trading and investing in equities like GE involves a high risk of capital loss. GE Aerospace’s heavy reliance on Boeing’s production schedule and global trade policies introduces significant volatility. Conduct independent research before allocating capital.

Related Reading

- Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

- Palantir (PLTR) Stock Outlook for 2026: Can AI-Driven Enterprise Supercycle Take PLTR to $235+?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Microsoft (MSFT) Stock Outlook for 2026: Can Azure AI and Copilot Growth Drive MSFT Stock to $550+?