In early 2026, AppLovin (APP) find itself in a paradox: while its financial performance is at an all-time high, generating $1.31 billion in free cash flow in Q4 2025 alone, its stock price has cratered from a high of $745 to under $390. The narrative has shifted from unstoppable AI growth to regulatory risk management as the SEC continues its probe into the company’s data collection practices. Yet, beneath the market jitters, AppLovin’s AXON 2.0 engine continues to gain wallet share, with domain integrations increasing 148% in the last three months.

AppLovin (APP) enters the second quarter of 2026 at a critical valuation floor. Despite a 45% year-to-date decline driven by an active SEC investigation and fears of a Nvidia-style hardware dependency in its AI stack, the company maintains a fortress-like 84% Adjusted EBITDA margin. With the general availability of its e-commerce advertising platform looming and a $3.3 billion remaining share buyback authorization, AppLovin is betting its $131 billion market cap on the belief that its AXON AI engine can outpace regulatory headwinds. Explore the institutional price targets, the rented land risk, and whether APP is a deep-value play at 14x forward earnings.

This guide breaks down the AppLovin stock price prediction for 2026 using data from Evercore ISI, Benchmark, and Piper Sandler. You will also discover how to gain exposure to AppLovin (APP) stock futures through BingX TradFi.

Top 5 Things for AppLovin Investors to Know in 2026

- The E-Commerce Pivot: General availability for the AXON-powered e-commerce tier is expected in mid-2026, aiming to bridge the gap between mobile gaming and retail.

- SEC Overhang: An active data practices probe by the SEC remains the primary weight on the stock’s P/E multiple, with a resolution unlikely before late 2026.

- Margin Superiority: AppLovin maintains a 57.4% net margin, significantly outperforming peers like Meta (30%) and Apple (27%).

- The Buyback Floor: With $3.3 billion left in its repurchase program, the company has the firepower to retire over 6% of its outstanding shares at current prices.

- Institutional Bullishness: Despite the price drop, 8 out of 9 major analysts maintain a Buy rating, with price targets averaging $654 to $775.

What Is AppLovin (APP)?

AppLovin is a leading AI-powered marketing platform that provides end-to-end software solutions for businesses to reach and monetize global audiences. In 2026, it has transitioned from being a gaming company to a core infrastructure utility for the mobile app economy. Its value lies in AXON, a real-time machine-learning auction engine that processes millions of data points per second to predict user behavior. Unlike traditional ad networks, AppLovin’s AI is designed to maximize performance (actual sales or installs) rather than just impressions.

AppLovin faces a structural prove-it year. CEO Adam Foroughi is pushing to diversify the revenue mix away from mobile gaming (historically 90% of advertisers) toward global e-commerce and Connected TV (CTV) via the Wurl acquisition. While short-sellers have targeted the company's reliance on Apple and Google’s privacy rules, the underlying AI efficiency continues to deliver a Return on Ad Spend (ROAS) that competitors struggle to match.

AppLovin’s Strategic Evolution (2012–2026): From Ad Network to AI Utility

- The Scaling Phase (2012–2020): Built a massive first-party data set by acquiring mobile game studios (Lion Studios) and launching the MAX mediation platform.

- The Software Pivot (2021–2024): Successfully shifted revenue from first-party games to high-margin software fees, powered by the launch of AXON 2.0.

- The Vertical Expansion (2025–2026+): Leveraging AI dominance in gaming to capture the $30 billion CTV and e-commerce markets, while navigating a tightening global regulatory landscape.

AppLovin (APP) 2025 Performance Overview: Record Cash, Volatile Price

AppLovin stock performance over the past year | Source: Google Finance

- Revenue Jump: Full-year 2025 revenue surged 70% to $5.48 billion, driven by Software Platform growth.

- Cash Conversion: The company generated $3.95 billion in free cash flow, one of the highest conversion rates in the tech sector.

- Stock Rollercoaster: APP shares soared 80% through mid-2025 before a late-year pullback triggered by short-seller reports and interest rate uncertainty.

- Inventory Expansion: Integrated with Wurl to bring AI bidding to streaming platforms, diversifying away from handheld mobile devices.

AppLovin (APP) 2026 Investment Outlook: The E-Commerce AI Pivot vs. SEC Regulatory Overhang

AppLovin stock outlook for 2026 | Source: Various analysts

The Bull Case: AppLovin Stock's $750 E-Commerce Hyper-Growth

The bull narrative hinges on the AXON-to-Everything expansion. In this scenario, the SEC probe concludes with a nominal fine and no structural changes to data collection, allowing AppLovin to maintain its attribution edge. By mid-2026, the general availability of the e-commerce platform scales rapidly, adding an estimated $1.2 billion in incremental software revenue. This shift diversifies the advertiser base beyond gaming, reducing cyclical risk and justifying a valuation re-rating toward a 25x forward P/E.

Practical execution in this scenario sees AppLovin leveraging its 87.9% gross margins to aggressively outbid competitors for high-intent traffic. With the $3.3 billion buyback program potentially retiring 6-8% of the float at current depressed prices, the resulting EPS pop would likely drive the stock toward the $750–$775 range. Investors should watch for Axon-pixeled domain counts to exceed 300% year-over-year growth as a primary indicator of this breakout.

The Base Case: The $650 Cash Cow Consolidation for APP Stock Price

The base case assumes AppLovin maintains its dominant moat on rented land within the mobile gaming sector. While the e-commerce rollout provides steady but not explosive growth, the core Software Platform continues to deliver a 1.0x LTV/CAC ratio (Life-Time Value to Customer Acquisition Cost). In this outlook, revenue growth stabilizes at a healthy 30-35%, and the company focuses on operational efficiency to keep Adjusted EBITDA margins locked at the 84% mark.

For investors, this is a play on capital return. Even without a massive valuation multiple expansion, the company’s ability to generate $4 billion+ in annual free cash flow creates a powerful floor. The stock likely trends toward $650, tracking a modest 18x forward earnings multiple. Success here is measured by wallet share gains among East Asian developers and the steady integration of AI creative tooling to lower advertiser friction.

The Bear Case: AppLovin Stock Dips to $350 on Regulatory De-Rating

The bear case is triggered by a Privacy Cliff, where the SEC or State AGs mandate a transition to non-deterministic attribution. This would blind the AXON engine's predictive accuracy, causing a sharp drop in ROAS (Return on Ad Spend) and forcing advertisers to migrate to walled gardens like Meta or Google. Simultaneously, if competitive pressure from Unity’s Vector AI forces AppLovin to lower its take rate to retain developers, the currently pristine 57% net margins would face immediate compression.

In this scenario, the market would likely strip away AppLovin’s AI Premium, de-rating the stock to a 10x–12x EV/EBITDA multiple. A failure of the e-commerce pilot to gain traction among non-gaming agencies would signal that AXON’s intelligence is siloed, not universal. If quarterly revenue growth slips into the single digits, institutional de-risking could see the stock test its 52-week support of $350, regardless of the ongoing buyback program.

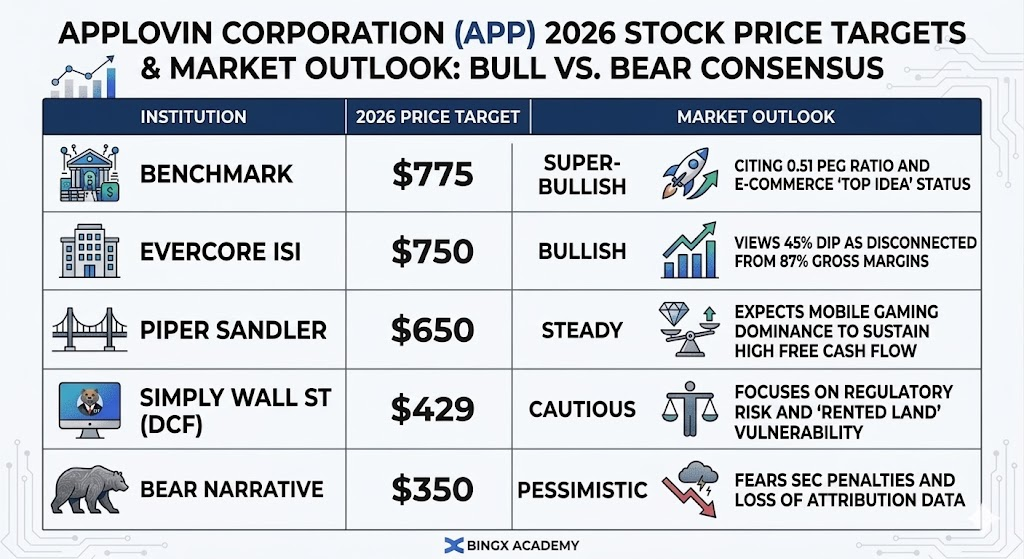

AppLovin Stock Price Forecasts for 2026: Bull vs. Bear Outlook

|

Institution |

2026 Price Target |

Market Outlook |

|

Benchmark |

$775 |

Super-Bullish: Cites 0.51 PEG ratio and e-commerce Top Idea status. |

|

Evercore ISI |

$750 |

Bullish: Views 45% dip as disconnected from 87% gross margins. |

|

Piper Sandler |

$650 |

Steady: Expects mobile gaming dominance to sustain high free cash flow. |

|

Simply Wall St |

$429 |

Cautious: Focuses on regulatory risk and rented land vulnerability. |

|

Bear Case |

$350 |

Pessimistic: Fears SEC penalties and loss of attribution data. |

How to Trade AppLovin (APP) Stock on BingX

Maximize your trading potential by using BingX's advanced TradFi tools to navigate AppLovin's Q1 earnings volatility.

Long or Short AppLovin (APP) Stock Futures

APP/USDT stock futures on BingX TradFi

- Navigate to BingX TradFi and select Stock Futures.

- Select the APP/USDT perpetual contract.

- Set your leverage, e.g., 2x–5x, and select Open Long if you expect a rebound, or Open Short to hedge against regulatory risk.

- Set Take-Profit (TP) and Stop-Loss (SL) levels before the May 6th earnings call.

Top 5 Risks to Watch for AppLovin Investors in 2026

While AppLovin’s AI-driven growth appears robust, investors must weigh the company’s exceptional margins against a high-stakes environment of regulatory scrutiny and platform dependency.

- The SEC Hammer: Any enforcement action that limits cross-app tracking would fundamentally impair AXON’s effectiveness.

- The Nvidia Tax: As AI models scale, rising compute costs could begin to eat into the currently pristine 84% EBITDA margins.

- Unity's Resurgence: Unity’s restructuring and Vector AI launch represent the first credible threat to AppLovin’s gaming dominance in three years.

- E-commerce Friction: If non-gaming advertisers find AXON's self-serve tools too complex, the 2026 growth story could stall.

- Platform Dependency: A single policy update from Apple (iOS) or Google (Android) regarding privacy could disrupt the company’s attribution logic overnight.

Final Thoughts: Should You Invest in AppLovin (APP) Stock in 2026?

AppLovin currently presents a Show-Me story characterized by Magnificent Seven fundamentals trading at a deep-value discount. At approximately 14x forward EV/EBITDA, the market has priced in a significant growth slowdown and regulatory fallout that the financial data has yet to reflect. For practical investors, the May 6, 2026, earnings call serves as the primary near-term litmus test; specifically, monitoring whether the 84% Adjusted EBITDA margin remains intact will reveal if the company’s AI efficiency can withstand rising compute costs and competitive pressure from Unity's Vector platform.

The mid-2026 outlook hinges on the general availability of the e-commerce suite, which represents the company's best chance to decouple its valuation from the volatile mobile gaming sector. If AXON 2.0 demonstrates high ROAS for non-gaming retailers, the stock could rapidly re-rate toward institutional targets of $750. However, the SEC overhang remains a non-trivial barrier; until there is clarity on the data collection probe, the stock may remain range-bound regardless of its $3.3 billion buyback firepower. Investors should prioritize tracking Axon-pixeled domain growth and quarterly free cash flow conversion as the ultimate indicators of long-term sustainability.

Risk Reminder: Trading and investing in equities like APP involves a high risk of capital loss. AppLovin’s heavy reliance on external OS policies by Apple andGoogle and the ongoing SEC investigation introduce significant volatility. All investors should conduct independent research or consult a financial advisor before allocating capital to high-growth ad-tech assets.

Related Reading

- Apple (AAPL) Stock Outlook for 2026: MacBook Neo Growth or AI Valuation Trap?

- Alphabet (GOOGL) Stock Outlook 2026: Can Gemini and Google Cloud AI Drive GOOGL Cross $420?

- Meta (META) Stock Price Prediction 2026: Can AI Efficiency and Custom Silicon Drive META to $900?

- Nvidia (NVDA) Stock Price Outlook for 2026: Can Blackwell and Vera Rubin Take NVDA Back to $300?