The global capital markets in mid-2026 are closely monitoring the enterprise technology ecosystem as the lines between traditional hardware manufacturing and advanced computing architectures permanently dissolve. Quantinuum (ticker symbol: QNT) serves as a primary vehicle for global growth investors aiming to capture a massive secular shift toward high-performance computing engines and full-stack software development setups. By anchoring its core portfolio operations in high-margin enterprise software licenses and advanced processing designs rather than legacy infrastructure, the newly public technology vendor presents a unique tactical allocation for the current macroeconomic climate.

As alternative asset platforms scale their product frameworks to compete directly with classic equity brokerages, institutional desks are re-evaluating enterprise software multiples to protect net investor yields. Wall Street analysts indicate that the traditional tracking parameters for advanced tech equities are undergoing a thorough re-rating throughout the second half of 2026. For international traders monitoring secular shifts in decentralized infrastructure, quantum processing platforms, and network defense rails, tracking the performance metrics of the company has become a core strategic imperative.

Read more: What Is Naoris Protocol (NAORIS)? The Internet Trust Fabric for a Post-Quantum Crypto World

Key Highlights: Top 5 Things for Tech Investors to Know in 2026

- The Dominant Trapped-Ion Hardware Footprint: Operating as an industry standard for safety-certified processing power, the flagship Helios hardware system has achieved immense global interest. This processor forms an essential core layer for enterprise clients transitioning toward next-generation computing speeds.

- The High-Margin Software Transition: Moving past its historical legacy as a pure research project, the enterprise structure relies heavily on intellectual property, recurring enterprise software configurations, and developer suites that feature exceptionally high gross margins.

- Rising Critical Infrastructure Protections: Capitalizing on tightening global security requirements, the Quantum Origin service shields multinational corporate clients and government agencies from complex network exploits and coordinated ransomware threats.

- A Massive Backlog of Unlocked Research Contracts: Supported by an expansion in active commercial development licenses, the company has compiled long-term future royalty backlog metrics. This accumulation provides steady, highly visible revenue generation paths for future fiscal years.

- High-Growth Capital Allocation Acceleration: Breaking away from initial small-scale funding structures, recent financial performance marks significant initial public offering milestones. This consistent funding delivery shows that the long-term strategic transition into a pure-play enterprise software and processing house is successfully translating into sustainable cash flows.

What Is Quantinuum (QNT)?

Quantinuum is the world's largest integrated quantum computing company, specializing in secure intelligent configurations, end-to-end cybersecurity solutions, and the rapidly growing advanced computing edge market. Formed in 2021 through the merger of Honeywell Quantum Solutions and Cambridge Quantum, the enterprise initially disrupted global technology sectors by engineering premier trapped-ion quantum computers that completely dominated early benchmarks.

After shifting its consumer reach to external enterprise partners and subsequently expanding baseline device support, the organization successfully transformed into a modern full-stack vendor backed by a powerful portfolio of foundational technology patents.

Today, the asset ecosystem operates as a highly liquid financial gateway across two distinct focus disciplines:

- The Advanced Hardware Segment: The branch scales high-performance quantum processors using the Quantum Charge-Coupled Device (QCCD) architecture, powering advanced digital systems, robotics networks, and commercial instrumentation platforms.

- The Cybersecurity and Software Segment: This pillar implements enterprise endpoint protection tools like Quantum Origin alongside automated developer engines like the Guppy language, Nexus platform, and InQuanto chemistry software library.

With its prominent position as a transformed pioneer in digital infrastructure, the company has built a massive market presence. In 2026, it operates as a deeply integrated technology play where automated quantum infrastructure networks and public cybersecurity frameworks function side by side.

Read More: Top 7 Ethereum DeFi Projects to Watch in 2026

Quantinuum's Core Details and Key Stock Metrics

- Primary Exchange Position: NASDAQ / High-Growth Technology Segment

- Inception Date: Formed via Merger in 2021 (Pioneering secure enterprise communications)

- Corporate Leadership Team: Led actively by CEO Dr. Rajeeb Hazra

- Global Headquarters Location: Broomfield, Colorado, United States

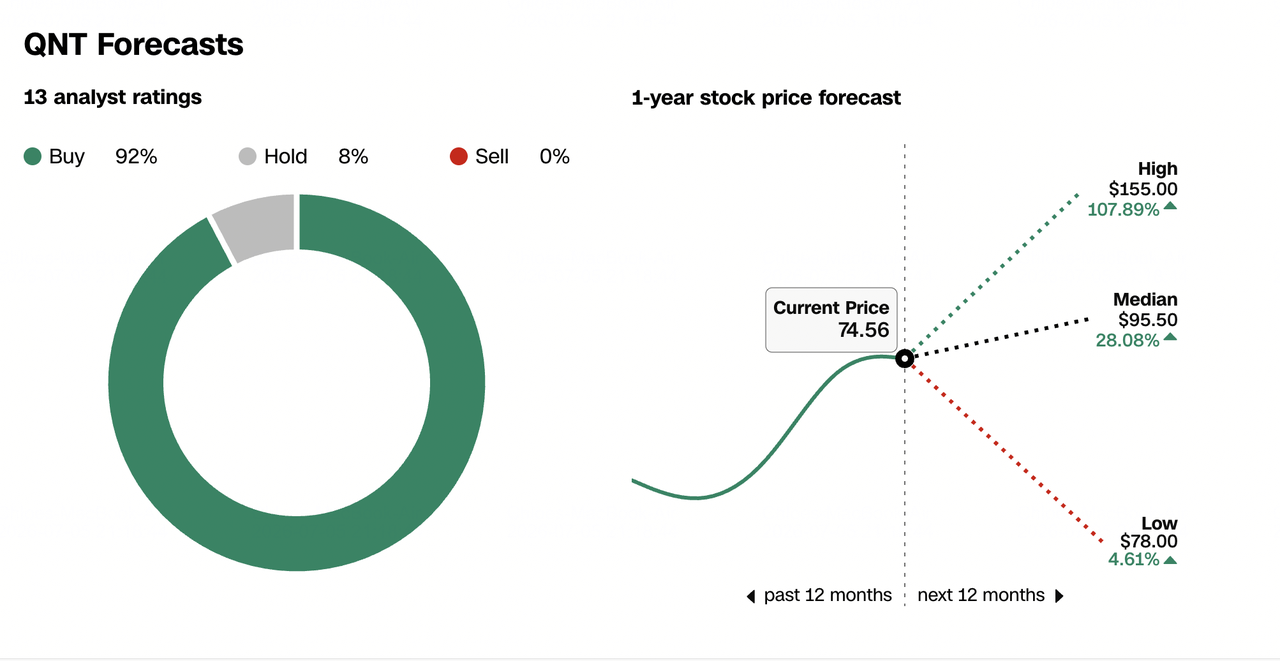

- Current Market Price: As of the July 2026 market close, the stock finished trading at a market valuation reflecting an asset price of $74.56.

Key Financial and Operating Metrics Table

The fundamental data tracking the company's enterprise software expansion highlights its operational footprint heading into the second half of the 2026 fiscal year:

|

Financial and Operating Metric Category |

2026 Stated Value Status |

Primary Revenue Driver |

Primary Growth Tailwinds |

Structural Risks and Roadblocks |

|

Current Stock Price |

$74.56 |

Quantum Processing Access and Advanced Software Subscriptions |

Accelerating enterprise software adoption; rising public infrastructure digital sovereignty. |

Highly sensitive to delayed commercial deployment lines; premium valuation multiple compression risk. |

|

Estimated Corporate Market Capitalization |

Approx. $19.47 Billion |

QNX Microkernel Licenses and Cylance Security Subscriptions |

Explosive growth in software-defined connected vehicles; expanding defense endpoint contracts. |

High exposure to global automotive manufacturing supply delays; intensive endpoint competition. |

|

Stated Day's Trading Range |

$71.52 to $80.61 |

Triple-Inverse Daily Index Swap Agreements |

Short-term hardware cyclical corrections; rapid downside technological re-ratings. |

Severe compounding volatility decay; structural drag during long-term tech bull runs. |

Following its recent IPO, the company maintains a strong institutional liquidity profile with a trailing 52-week trading range of $50.10 to $82.30. As a growth-phase enterprise, it currently operates at a near-term loss while driving full-year projected corporate revenue through enterprise platform upgrades. Operationally, the firm is focused on full-stack trapped-ion hardware and developer suites, anchoring its core architecture design on proprietary Quantum Charge-Coupled Device (QCCD) processor modules.

2026 Tech Sector Investment Comparison

The table below contrasts the financial parameters, underlying attributes, and structural tailwinds defining Quantinuum alongside comparable enterprise computing and security plays in the 2026 market cycle.

|

Asset Class / Strategy |

Implied Focus Sector |

Primary Revenue Driver |

Primary Growth Tailwinds |

Structural Risks & Roadblocks |

|

Quantinuum (QNT) |

Intelligent Embedded Hardware & Cybersecurity |

Quantum Processing Access & Advanced Software Subscriptions |

Accelerating enterprise software adoption; rising public infrastructure digital sovereignty. |

Highly sensitive to delayed commercial deployment lines; premium valuation multiple compression risk. |

|

BlackBerry Ltd (BB) |

Embedded IoT Operating Systems & Cybersecurity |

QNX Microkernel Licenses & Cylance Security Subscriptions |

Explosive growth in software-defined connected vehicles; expanding defense endpoint contracts. |

High exposure to global automotive manufacturing supply delays; intensive endpoint competition. |

|

Direxion Daily Semi Bear 3X (SOXS) |

Leveraged Inverse Technology Derivatives |

Triple-Inverse Daily Index Swap Agreements |

Short-term hardware cyclical corrections; rapid downside technological re-ratings. |

Severe compounding volatility decay; structural drag during long-term tech bull runs. |

Recent Corporate Developments and Strategy of QNT

Rather than relying purely on legacy enterprise desktop clients, the company's mid-2026 layout focuses on institutional edge computing and high-performance automated interfaces.

1. Integration with Advanced AI and Classical Frameworks

Expanding past traditional laboratory applications, the company deployed specialized versions of its developer platform into high-performance classical computing infrastructure. By combining its certified, high-accuracy code architecture with emerging processing models, the firm is successfully capturing critical market share in automated industrial computing sectors.

2. Sovereign Security and Cryptographic Updates

As geopolitical friction drives demand for tight regional data control, the company secured high-level validation for its secure cryptographic generation models. This compliance hurdle solidifies the company's position as a trusted vendor for western defense networks and federal agencies, helping reverse multi-quarters of slow growth in the cybersecurity segment.

Read more: Top 10 Quantum Computing Stocks to Watch in 2026: Companies Driving Next-Gen Computation

The Investment Thesis for QNT in 2026: 5 Pillars of Market Valuation

Source: CNN

1. The Embedded Processing Monopoly Moat

With its core software running alongside top-tier research systems worldwide, the enterprise maintains an exceptionally resilient competitive defensive barrier. Because changing a system's foundational code infrastructure is highly complex, major industrial partners rely on this software to maintain digital dashboards, automated aids, and network structures.

2. Strong Operating Leverage in Software Licensing

The company's transition into commercial deployment has driven an expansion in potential profit margins. Once initial development costs are cleared, new revenue from development licenses and software platform access drops directly to the bottom line, accelerating profitability as the business expands.

3. Rising Global Demand for Secure Communications

As corporate data networks face a rising threat from sophisticated ransomware and state-sponsored cyberattacks, the company's long-standing security reputation acts as a key sales driver. This track record positions it to capture steady enterprise security budgets and expand long-term recurring subscriptions.

4. Capital-Efficient Growth on Fixed Expenditures

Operating with a lean, streamlined cost structure following a comprehensive corporate transformation, the business model requires minimal marginal expenditures to distribute new software copies. This setup allows rising sales volumes to rapidly expand cash flow generation without needing heavy asset modifications.

5. Expansion into Alternative Material Industries

By adapting its core chemistry models to handle industrial automation, chemical research, and molecular testing grids, the company is opening large new revenue channels. This diversification insulates the business from cyclical slowdowns in any single computing niche.

Read more: IonQ (IONQ) Stock Forecast 2026: $100 Quantum Supremacy Flywheel or Speculative Burn Trap?

Quantinuum's Valuation and Performance Forecasts for 2026: Bull vs. Bear Outlook

Institutional research desks maintain an active dialog regarding the company's trajectory, balancing its high-margin processing dominance against its elevated market multiple.

|

Institution / Analyst Desk |

2026 Target Valuation Range |

Market Outlook / Stance |

|

Rosenblatt Tech Equity |

$155.00 |

Highly Bullish: Driven by a rapid conversion of the advanced computing roadmap and strong physical AI system integrations. |

|

Craig-Hallum Financials |

$100.00 |

Bullish: Supported by solid market position as an industry leader and expanding enterprise software deployments. |

|

Evercore ISI Research |

$98.00 |

Outperform: Expects steady operational leverage as logical qubit metrics hold high on rising recurring revenues. |

|

JPMorgan Capital Markets |

$97.00 |

Overweight: Encouraged by high gate fidelity figures and strong placement in commercial hardware environments. |

|

UBS Global Research Desk |

$93.00 |

Buy: Projects steady growth on clear processing roadmaps and expanding developer suite adoption. |

|

Jefferies Research Division |

$90.00 |

Buy: Cautious on high trailing price-to-sales multiples, but sees a differentiated technology lead. |

|

Morgan Stanley Equity |

$78.00 |

Equal-Weight: Concerned that any slowdown in global enterprise tech budgets will directly delay high-margin deployment payouts. |

The Bull Case: Connected Processing Spikes Power Scalable Cash Flows

Bulls argue that as commercial computing networks scale globally, the embedded software value per client will rise significantly. Combined with steady recurring government security contracts, this growing installation volume would generate substantial free cash flows, lifting the stock's valuation well above its baseline software targets as it shifts into a highly profitable growth phase.

The Bear Case: Deployment Delays Compress Premium Multiples

Bears emphasize that the stock's recent valuation metrics place it well past broader software sector averages. If global hardware manufacturing faces supply chain disruptions or slowing deployment schedules, commercial realizations will stall, exposing the stock's premium valuation to significant multi-multiple compression.

Competitive Risks and Sector Pressures

While the company benefits from strong embedded market presence and expanding margins, its management team must carefully navigate several structural headwinds:

- Commercial Assembly and Deployment Dependencies: Operating as an advanced hardware provider means revenue remains tied to aggregate global tech budgets. If macro headwinds or component shortages delay platform builds, the realization of the commercial backlog will slow down.

- Intense Enterprise Cyber Competition: The enterprise cybersecurity landscape features aggressive, well-capitalized cloud native security vendors. If competitors underprice core services, the company faces potential margin compression or customer churn in its secure communications division.

- Elevated Short-Term Valuation Multiples: Following its substantial post-IPO interest, equity carries a steep premium multiple compared to historical averages. This premium exposure increases the stock's vulnerability to sudden market-wide corrections if upcoming quarterly reports show any deviation from guidance.

Read more: Amazon (AMZN) Stock Price Prediction 2026: Can AWS AI Re-acceleration Offset a $200B CapEx Gamble?

How to Trade Quantinuum (QNT) on BingX

For global market participants looking to take advantage of the volatility surrounding software updates and advanced computing product cycles, trading derivative contracts offers a highly flexible, capital-efficient alternative to traditional share ownership. This vehicle allows active traders to manage risk or target short-term price movements around major corporate milestones, much like how tech investors track updates across traditional finance (TradFi), semiconductor leaders like NVIDIA, or core digital assets like Bitcoin.

- Go to the BingX TradFi section and select Stock Futures.

- Search for the QNTUS/USDT perpetual contract.

- Check the trading session before placing your order. Liquidity is typically lower during extended sessions, which can result in wider spreads and higher volatility.

- Select your Margin Mode (Isolated or Cross) and set your leverage.

- Choose Open Long if you expect momentum. Choose Open Short if you anticipate margin pressures or valuation pullbacks.

- Set Take-Profit (TP) and Stop-Loss (SL) levels immediately to manage risk against QNTUS's price swings driven by earnings, news, or global semiconductor production milestones.

Conclusion: Navigating the Software Turnaround Frontier

The enterprise tech sector in 2026 is moving through a major evolution. The investment products positioned for sustainable utility are those that successfully bridge legacy computing limits with modern intelligent edge software tools. The strategic positioning of this company as an integrated hardware and software engine, complete with deep government security alignments and professional developer tools, demonstrates a clear tactical role.

While investors must monitor premium valuation multiples and global tech spending trends, the structural convenience of its software licensing model and positive platform generation capabilities continue to support its market presence. For short-term derivatives traders and long-term tech allocators alike, tracking the vehicle provides a direct way to participate in the future of alternative enterprise technology as high-margin platforms and modern trading terminals establish a new global standard.

Risk Reminder: Derivative and leveraged investment contracts carry high market risk. Rapid shifts in central bank interest rates, sudden adjustments to futures clearing regulations, and unexpected margin requirement updates can cause sharp capital movements. Always deploy strict risk-management and stop-loss protocols to shield capital against sudden shifts in market sentiment.

Related Reading

- Top High-Bandwidth Memory (HBM) Stocks to Buy in the 2026 Memory Supercycle

- Top AI Compute and GPU Stocks to Buy in 2026: The Shift to Inference and Custom Silicon

- Top AI Data Center Stocks to Buy in 2026: Cloud, Servers, and AI Compute Infrastructure

- Top AI Cloud Infrastructure Stocks to Buy in 2026 Amid Hyperscaler Capex and the Neocloud Boom

- Top AI Semiconductor Stocks to Buy in 2026: AI Chips and Supply Chain Complete Guide