In April 2026, Johnson & Johnson (JNJ) is shedding its skin. By divesting the lower-margin Kenvue consumer segment and moving toward a strategic separation of its Orthopaedics business, J&J has transformed into a pure-play Innovative Medicine and MedTech powerhouse. Despite trailing the S&P 500’s recent 2.51% daily gain, JNJ has surged 60% since early 2025, trading at $241.30. Investors are currently locked in a tug-of-war: Bulls highlight a pipeline of the decade with assets like Darzalex and Carvykti poised to offset legacy losses, while bears warn that 67,000 unresolved talc lawsuits and Medicare price negotiations represent a structural ceiling.

As the April 14, 2026, earnings report approaches, J&J is positioning itself as the "only healthcare company delivering over $100 billion in annual revenue." With 51 drug approvals in the rearview mirror and a $14.6 billion R&D engine, JNJ is no longer a slow-moving conglomerate. This guide analyzes the JNJ stock price prediction for 2026 using data from Zacks Research, Trefis, Simply Wall St, and TIKR.

You will also discover how to gain exposure to Johnson & Johnson (JNJ) stock futures through BingX TradFi.

Top 5 Things for JNJ Investors to Know in 2026

- The $101B Revenue Target: J&J has issued 2026 sales guidance of $100 billion–$101 billion, signaling that its high-growth oncology and immunology portfolios have successfully absorbed the Stelara cliff.

- The Talc Litigation Shadow: Over 67,000 plaintiffs continue to sue J&J over asbestos-related cancer claims. Analysts estimate a potential settlement range of $10 billion–$15 billion, which keeps the stock’s valuation multiple suppressed compared to pure-play peers.

- Dividend King Status: With 63 consecutive years of dividend increases and a current yield of around 2.15% as of April 2026, JNJ remains a premier defensive asset for passive income seekers during market volatility.

- MedTech PFA Launch: The European rollout of the VARIPULSE Pro (Pulsed Field Ablation) system marks J&J's aggressive expansion into the high-growth cardiac arrhythmia market.

- IRA Price Negotiations: For the first time, Medicare is negotiating prices on top-sellers like Stelara and Xarelto, creating a new margin headwind that the company must offset through volume-led growth in newer therapies.

What Is Johnson & Johnson (JNJ)?

Johnson & Johnson is the world’s largest healthcare company, headquartered in New Brunswick, New Jersey. Following the 2023 spinoff of Kenvue (Consumer Health), the company operates two primary segments: Innovative Medicine (Pharmaceuticals) and MedTech (Medical Devices).

J&J serves as a cornerstone of the global healthcare infrastructure, with 28 platforms or products each generating at least $1 billion in annual revenue. Under CEO Joaquin Duato, the company has pivoted toward high-science therapeutic areas like Oncology, Immunology, and Neuroscience.

JNJ enters Q1 2026 with a consensus EPS of $2.68. While the stock’s 20.6x forward P/E ratio sits at a premium to the pharmaceutical industry average of 14.2, its 35% Return on Equity (ROE) and $21 billion in projected free cash flow justify its status as a premium flight-to-quality asset.

J&J’s 2026 Strategy: The Catapult Transformation

- Oncology Dominance: J&J is targeting $50 billion in Oncology revenue by 2030, led by Darzalex (Multiple Myeloma) and the explosive 96% growth of cell-therapy Carvykti.

- Precision MedTech: The acquisition of Abiomed and the launch of the TECNIS PureSee surgical vision franchise signal a move toward high-margin robotics and cardiovascular interventions.

- The Kenvue-less Growth Profile: By shedding slower-moving bandages and baby powder, J&J has increased its net income margin to roughly 28.5%, allowing it to re-invest in bolt-on acquisitions like the $3.05 billion Halda Therapeutics deal.

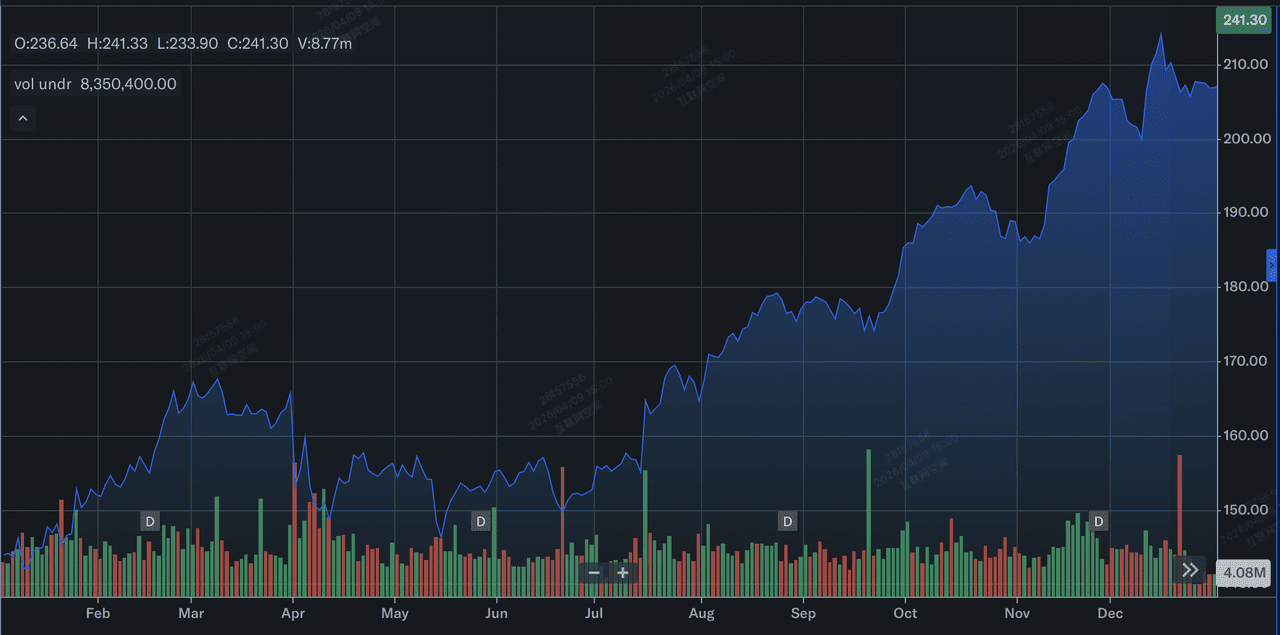

Johnson & Johnson Stock Performance in 2025: An Overview

J&J stock performance in 2025 | Source: Yahoo Finance

In 2025, Johnson & Johnson (JNJ) delivered a catapult performance, characterized by significant stock price appreciation and robust operational growth. The stock surged approximately 44% over the year, rising from roughly $144 in early January to close near $207 by December 31, significantly outperforming its historical averages. This rally was underpinned by a 6% increase in full-year reported sales to $94.2 billion and a dramatic 90.5% jump in diluted earnings per share (EPS) to $11.03, largely due to the absence of one-time charges related to the 2024 Kenvue spinoff.

Operationally, growth was driven by 28 billion-dollar platforms, with oncology blockbusters like Darzalex and Carvykti, which surpassed $1 billion in annual sales for the first time, leading the Innovative Medicine segment. Despite the looming Stelara cliff and ongoing talc litigation, J&J’s strategic pivot into high-margin MedTech and pharmaceuticals allowed it to enter 2026 with a market capitalization exceeding $580 billion and a record sales outlook.

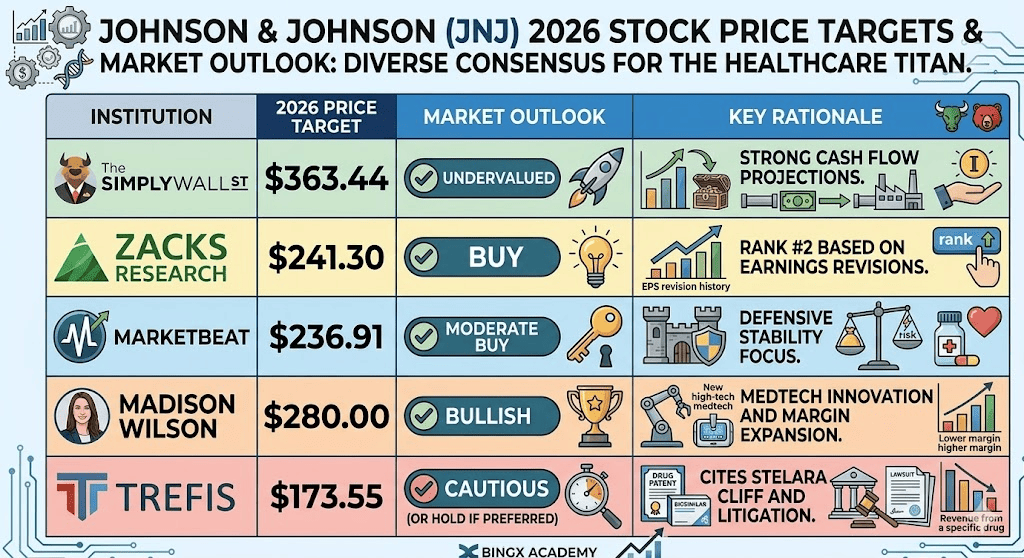

JNJ Stock 2026 Investment Outlook: $363 Fair Value vs. $173 Bear Trap

JNJ stock forecast scenarios for 2026 by various analysts

The 2026 outlook is a battle between best-in-class operational execution and massive legal/regulatory liabilities.

The Bull Case: JNJ’s $300 Blue-Chip Breakout

The bullish narrative is anchored in a massive valuation re-rating as J&J transitions from a conglomerate to a high-velocity Oncology-first entity. If the April 14 earnings report delivers an EPS beat above the $2.68 consensus, it will validate the 2025 catapult strategy. The primary engine is the Discounted Cash Flow (DCF) intrinsic value of $363.44, which assumes the market shifts from pricing JNJ as a legacy pharma player to a growth-oriented MedTech leader. With Tremfya scaling toward $10 billion in peak sales and Carvykti maintaining nearly 100% year-over-year growth, J&J could realize the Dimon-like premium historically reserved for tech-integrated financials.

Practically, the $300 target requires a definitive ring-fencing of the talc litigation. If J&J successfully utilizes the tort system to cap liabilities at the lower end of the $10 billion–$15 billion estimate, the litigation discount currently suppressing the P/E multiple will evaporate. This would allow J&J’s Forward P/E to expand toward 25x, aligning it with pure-play peers. Investors should watch for a sustained 28.5% net income margin; if the $21 billion in projected free cash flow is deployed for aggressive bolt-on acquisitions like the Halda Therapeutics RIPTAC platform, the stock enters a multi-year alpha phase.

The Base Case: J&J Stock’s $245 Fair Value Consolidation Between $235 and $255

The base case positions J&J as the ultimate Fortress of Healthcare, where steady execution offsets structural headwinds. In this scenario, JNJ tracks the S&P 500 Healthcare Index by trading near its mean analyst target of $241.08. Revenue growth remains stable at 6.7%, fueled by the MedTech segment's 5.4% operational growth and the European launch of VARIPULSE Pro. This outlook assumes J&J successfully muddles through the Stelara patent cliff, using its 28 billion-dollar platforms to absorb the revenue erosion without sacrificing its 2.15% dividend yield or its 63-year payout streak.

From a technical perspective, expect high-floor consolidation between $235 and $255. While the $500 million MedTech tariff impact and Medicare price negotiations act as friction, J&J’s 35.03% Return on Equity (ROE) provides a massive safety buffer. For long-term holders, this is the 'Boring is Beautiful' narrative: the JNJ stock provides a low-beta (0.34) hedge against broader market volatility. The focus here is on dividend compounding and the separation of the Orthopaedics business, which simplifies the balance sheet and ensures J&J remains a cornerstone flight-to-quality asset.

The Bear Case: Johnson & Johnson Stock at $173 Amid Litigation Peak

The bear case is a perfect storm of legal setbacks and regulatory margin compression. The primary trigger would be an adverse Daubert ruling on appeal, which would validate plaintiffs' scientific claims and potentially force J&J to increase its litigation reserves far beyond the current $15 billion baseline. This would create a black hole of uncertainty, driving institutional outflows as hedge funds de-risk. If the Inflation Reduction Act (IRA) negotiations result in price cuts exceeding 20% on top-sellers like Stelara, the projected 6.9% earnings growth could turn negative, leading to a sharp compression of the 20.6x Forward P/E.

In this risk-off environment, J&J’s stock would likely test its 52-week floor of $141.50 before settling near the bear-case fair value of $173.55. A failure to hit the $100 billion revenue milestone in 2026, caused by faster-than-expected biosimilar entry or a slowdown in MedTech adoption, would signal that the post-Kenvue growth story was priced for perfection. Investors would pivot from viewing J&J as an innovation leader to seeing it as a legacy giant trapped in a cycle of litigation and patent expiration, resulting in a 28% downside and a multi-year period of underperformance.

Johnson & Johnson (JNJ) Stock Price Forecasts for 2026

|

Institution |

2026 Price Target |

Market Outlook |

|

Simply Wall St (DCF) |

$363.44 |

Undervalued: Strong cash flow projections. |

|

Zacks Research |

$241.30 |

Buy: Rank #2 based on earnings revisions. |

|

MarketBeat |

$236.91 |

Moderate Buy: Defensive stability focus. |

|

Madison Wilson |

$280.00 |

Bullish: MedTech innovation and margin expansion. |

|

Trefis (Bear Case) |

$173.55 |

Cautious: Cites Stelara cliff and litigation. |

How to Trade Johnson & Johnson (JNJ) Stock on BingX

Manage JNJ’s earnings volatility and litigation headlines using BingX TradFi and BingX AI tools to track sentiment shifts.

JNJ/USDT perps on the BingX futures market

Long or Short JNJ Stock Futures on BingX

- Navigate to BingX TradFi and select Stock Futures.

- Select the JNJ/USDT perpetual contract.

- Set your leverage (e.g., 2x–5x) and select Open Long if you anticipate a revenue beat above $101B, or Open Short to hedge against legal news.

- Set Take-Profit (TP) and Stop-Loss (SL) levels to manage the 20.6x P/E valuation risk.

Top 5 Risks to Watch for JNJ Investors in 2026

Successful navigation of the 2026 healthcare market requires balancing J&J’s catapult growth against the structural legal and regulatory hurdles that could impact its valuation multiple.

- Talc Litigation Liquidity Drain: With over 67,000 active lawsuits, any court ruling that forces J&J to increase its $10–$15 billion settlement reserve would directly threaten the free cash flow currently earmarked for R&D and dividend growth.

- The Stelara Volume Gap: While new Oncology assets are scaling, J&J must prove that volume-led growth in Carvykti and Tremfya can move fast enough to offset the double-digit revenue erosion from biosimilar competition and patent expirations.

- IRA Margin Compression: 2026 marks the implementation of Medicare’s negotiated lower prices for Stelara and Xarelto, creating a mandatory margin headwind that requires J&J to find internal operational efficiencies through Project Catalyst.

- MedTech Supply Chain Friction: A projected $500 million impact from medical device tariffs and global trade shifts could dampen the profitability of high-growth surgical robotics and vision franchises just as they reach critical mass.

- M&A Integration Execution: To sustain its $101B revenue target, J&J must successfully integrate massive acquisitions like the $14.6 billion Intra-Cellular Therapies deal without experiencing the conglomerate drag that led to the Kenvue spinoff.

Final Thoughts: Should You Invest in J&J (JNJ) Stock in 2026?

Johnson & Johnson in 2026 represents a calculated transition from a legacy healthcare conglomerate to a high-margin, innovation-driven engine. While the stock’s 20.6x forward P/E reflects a premium valuation, this is supported by a robust $21 billion free cash flow projection and the strategic achievement of the $101 billion revenue milestone. For investors, the April 14, 2026, earnings call serves as the definitive proof of concept; it will reveal if the volume-led growth in Oncology and the European VARIPULSE Pro launch are successfully outrunning the "Stelara cliff" and inflationary MedTech headwinds.

Practically, JNJ remains a premier flight-to-quality asset for those prioritizing defensive stability and growing passive income during geopolitical or economic volatility. However, the $15 billion talc litigation overhang and the implementation of Medicare price negotiations suggest that entry timing and position sizing are critical to managing idiosyncratic risk. Investors should monitor the $235–$240 support levels for potential entry points while maintaining a long-term horizon to allow the post-Kenvue portfolio transformation to fully mature.

Risk Reminder: Trading and investing in equities like JNJ involve a significant risk of capital loss. The company’s performance is highly sensitive to unpredictable legal rulings, FDA clinical trial outcomes, and shifting federal drug pricing regulations. Historical performance is not indicative of future results; always conduct independent due diligence or consult a financial advisor before allocating capital.

Related Reading

- Vicinity Centres (VCX) Price Prediction 2026: Premium Pivot or Consumer Pullback at A$2.60?

- JPMorgan Chase (JPM) Price Prediction 2026: Fortress Defense or AI-Driven Alpha at $330?

- Goldman Sachs (GS) Price Prediction 2026: Strategic Renaissance or Value Trap at $860?

- GE Aerospace (GE) Price Prediction 2026: Can the $190B Backlog Defy Valuation Fears?